The original Cactus Pipeline was a pioneer in moving large volumes of crude oil from the Permian and the Eagle Ford to the Corpus Christi area, which quickly became a leader in U.S. crude exports. Cactus II, an even longer and larger pipeline that came online in H2 2019, only added to Corpus Christi’s export prominence. But the competition with Permian-to-Houston pipelines is fiercer than ever and negotiated rates on pipelines to the Texas Gulf Coast are under pressure. In today’s RBN blog, we look at the Cactus I and Cactus II pipelines and their significance.

Analyst Insights are unique perspectives provided by RBN analysts about energy markets developments. The Insights may cover a wide range of information, such as industry trends, fundamentals, competitive landscape, or other market rumblings. These Insights are designed to be bite-size but punchy analysis so that readers can stay abreast of the most important market changes.

The EIA reported total U.S. propane/propylene inventories had a build of 2.63 MMbbl for the week ended August 15, which was more than industry expectations for an increase of 2.2 MMbbl and the average build for the week of 1.5 MMbbl. Total U.S.

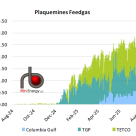

Venture Global’s Plaquemines terminal averaged more than 3 Bcf/d of feedgas last week for the first time, as the company makes more progress.

| Report | Title | Published |

|---|---|---|

| NATGAS Billboard | NATGAS Billboard - August 21, 2025 | 5 hours 9 min ago |

| Chart Toppers | Chart Toppers - August 21, 2025 | 8 hours 24 min ago |

| TradeView Daily Data | TradeView Daily Data - August 20, 2025 | 21 hours 46 min ago |

| Crude Oil Billboard | Crude Oil Billboard Weekly - August 20, 2025 | 23 hours 8 min ago |

| NATGAS Appalachia | NATGAS Appalachia Weekly – August 20, 2025 | 23 hours 15 min ago |

MPLX’s July 31 announcement that it has reached an agreement to acquire Northwind Midstream for $2.375 billion puts a spotlight on two undeniable trends. First, the acquisition is the latest in what by now is a long series of multibillion-dollar deals by midstream giants to expand their Permian-to-Gulf, “wellhead-to-water” networks that gather, process, transport and export crude oil, natural gas and/or NGLs. Second, Northwind has been a pioneer in gathering and processing unusually sour associated gas in the prolific Northern Delaware Basin, an area of particular interest to a growing number of E&Ps. In today’s RBN blog, we discuss the deal and what it brings to MPLX.

U.S. E&Ps’ strategic shift from growth at any cost to a laser focus on cash flows to fund shareholder returns revitalized their investor base. But that strategy has been challenged as crude oil prices have eroded since their mid-2022 peak, with producers struggling to balance the need to maintain output and the pressure to sustain dividends. In today’s RBN blog, we’ll see how things are going with the oil and gas companies that bear no responsibility for the costs and complications associated with the finding, development and production of hydrocarbons — the entities that own mineral and royalty interests.

The uncertainty and angst spurred by the ongoing trade war doesn’t seem to have dampened foreign companies’ interest in acquiring upstream and midstream energy assets in the U.S. The recent rumor — still unconfirmed — that Mitsubishi Corp. is in talks to acquire Aethon Energy Management’s massive holdings in the Haynesville for a reported $8 billion is only the latest indication that overseas interest may be stronger than ever. In today’s RBN blog, we’ll discuss the latest round of foreign investments in U.S. energy and what’s driving those deals. We’ll also look at the Aethon assets on the block.

You might have thought the flurry of acquisitions and buyout deals that midstream companies entered into over the past couple of years would have satisfied their evident desire to refocus, expand and reshape their businesses. But you’d be wrong. In the first half of 2025 — a period of considerable uncertainty in the energy industry — midstream players continued to buy and sell pipelines and other important assets at a frenetic pace. In today’s RBN blog, we discuss some of the more interesting recent transactions and what they tell us about the midstream space.

The summer movie season opened with the latest — and reportedly last — entry in the Tom Cruise-propelled “Mission: Impossible” franchise called “The Final Reckoning.” That title reminded us that, to E&P executives, the commodity price crash at the onset of the pandemic in 2020 must have seemed like the final blow in a series of financial crises that brought many of their companies to the verge of bankruptcy. But in a dramatic, “Mission: Impossible”-style recovery, producers restored their battered balance sheets and won back investors by radically shifting cash allocations. In today’s RBN blog, we’ll review the rise of the new E&P hero — dividends — and analyze how producers apportioned cash flows in Q1 2025.

Energy-market risks abound. Israeli attacks on Iranian oil and gas infrastructure. The looming possibility of a global trade war. Up-and-down prices for WTI and Brent. Still, in the midst of all this doubt and instability, oil and gas producers continue to buy and sell major upstream assets in the U.S. — and gobble up entire companies — in ongoing efforts to grow their businesses, reshape their portfolios and/or reduce their debt. In today’s RBN blog, we continue our look at recent big-dollar deals in the U.S. oil and gas industry.

U.S. fuel supplier Sunoco announced in May that it has inked a US$9.1-billion agreement to buy Canada-based Parkland Corp., a move that would create the Americas’ largest independent fuel distributor. Sunoco would gain control of Parkland’s fleet of fueling stations and its valuable Burnaby refinery near Vancouver, BC. The deal is supported by Parkland’s largest shareholder and is slated to be voted on June 24. In today’s RBN blog, we’ll discuss this deal and what it means for Canada’s only West Coast refiner.

The pace of multibillion-dollar acquisitions in the upstream sector may have eased a bit after a frenetic couple of years, but M&A among E&Ps is still happening. And, just as important, producers just coming off big deals are divesting assets that don’t fit their strategies, or reaching agreements to buy “bolt-on” acreage and production in key basins. There’s a lot of M&A “fun, fun, fun” going on, though many of the deals don’t make big headlines because there are only nine or 10 numbers after the dollar sign, not 11. In today’s RBN blog, we look at a variety of recent upstream M&A and divestment announcements and what they tell us about the production end of U.S. energy markets.

Buoyed in part by early optimism about the Trump administration’s potentially positive impact on the economy and the oil and gas industry, the WTI spot oil price reached a five-month high of nearly $76/bbl in January. But the optimism and oil prices have steadily eroded due to the impact of tariffs, trade wars and stubborn oilfield service inflation. In today’s RBN blog, we’ll look at the impact of the January price spike on Q1 2025 earnings and analyze the potential impact of a much lower price scenario in Q2 2025.

Over the past month, E&P executives have addressed shareholder and analyst concerns amid the murkiest market conditions since the onset of the pandemic in Q1 2020. One industry leader pointed out that on an inflation-adjusted basis, there have only been two quarters since 2004 when front-month oil prices have been as low as they are today (excluding 2020). In today’s RBN blog, we review what we heard from E&P brass — a measured response that melded confidence in the industry’s new fiscally conservative, shareholder-focused business model; modest spending reductions; and preparations for more substantial responses to future erosion in commodity pricing.

Serious concerns about higher costs and lower demand have left the E&P sector in a delicate position since the implementation of new U.S. tariffs, as evidenced by the Dallas Federal Reserve Bank’s recent survey of producers, who appear especially vulnerable after massive acquisition spending in 2024 to deepen and high-grade their portfolios. In today’s RBN blog, we’ll explore the impact of the 2024 acquisitions and commodity pricing on E&P debt and discuss the expected response to protect balance sheets.

The tide is shifting in the energy sector back toward hydrocarbons as renewables face new, big hurdles. The latest tangible sign of this shift is BP’s decision to refocus on traditional oil and gas and deemphasize renewables, which follows ExxonMobil’s and Shell’s restructuring of strategies in the same direction. The likelihood that hydrocarbon demand will continue to grow throughout this decade has reinforced the importance of E&P companies adding to their proved oil and gas reserves. In today’s RBN blog, we analyze crucial trends from the 2024 reserve reporting of the major U.S. oil and gas producers.

The record $120 billion upstream M&A spending spree in 2024 focused on the consolidation of Permian Basin positions by the major U.S. publicly traded oil and gas companies. With crude oil prices stagnant in the $70-$80/bbl range, producers were driven to boost Tier 1 acreage and capture operational synergies to fund the generous shareholder returns demanded by their investor base. When the dust cleared at year-end, the larger E&Ps we track — plus supermajor ExxonMobil — closed or announced deals on acreage that generated about 1.5 MMboe/d of production, almost 25% of their 2023 Permian output. In today’s RBN blog, we’ll analyze what this unprecedented consolidation means for Permian production going forward.

In an industry such as oil and gas that is beset with more uncertainty than usual of late due to geopolitical upsets, bubbling trade wars and a recent plunge in crude oil prices, being a larger company with the resources to survive the turbulent times — and thrive when the sailing is smoother — is more important than ever. For Western Canada’s energy sector, this has meant companies getting bigger through mergers. In today’s RBN blog, we discuss the planned combination of Whitecap Resources and Veren, one of the largest deals to emerge in the region in recent memory, as well as several other recent transactions that have been part of the consolidation wave.

As the clock approached midnight on December 31, E&P managements and shareholders likely clinked champagne flutes to celebrate a remarkable four years of prosperity for an industry that had been nearly shattered by two decades of periodic financial crisis. Soaring post-pandemic commodity prices and gold-plated balance sheets provided generous cash flows, enabling substantial shareholder payouts that restored investor support, but after a period of relative stability the outlook for the E&Ps we follow is uncertain. In today’s RBN blog, we’ll review the cash-allocation strategies used by U.S. oil and gas producers in 2024 and examine the factors that could dramatically impact the sector’s performance in 2025.