Serious concerns about higher costs and lower demand have left the E&P sector in a delicate position since the implementation of new U.S. tariffs, as evidenced by the Dallas Federal Reserve Bank’s recent survey of producers, who appear especially vulnerable after massive acquisition spending in 2024 to deepen and high-grade their portfolios. In today’s RBN blog, we’ll explore the impact of the 2024 acquisitions and commodity pricing on E&P debt and discuss the expected response to protect balance sheets.

Join us at our historic 20th School of Energy!

School of Energy: Foundations is a two day, in person conference designed to help energy professionals better understand the forces shaping crude oil, natural gas, NGLs, refined products, and petrochemicals.

Attendees will learn from RBN experts, work with Excel based analytical models, participate in Q&As, and network with industry peers.

Build the foundation to better navigate volatile energy markets.

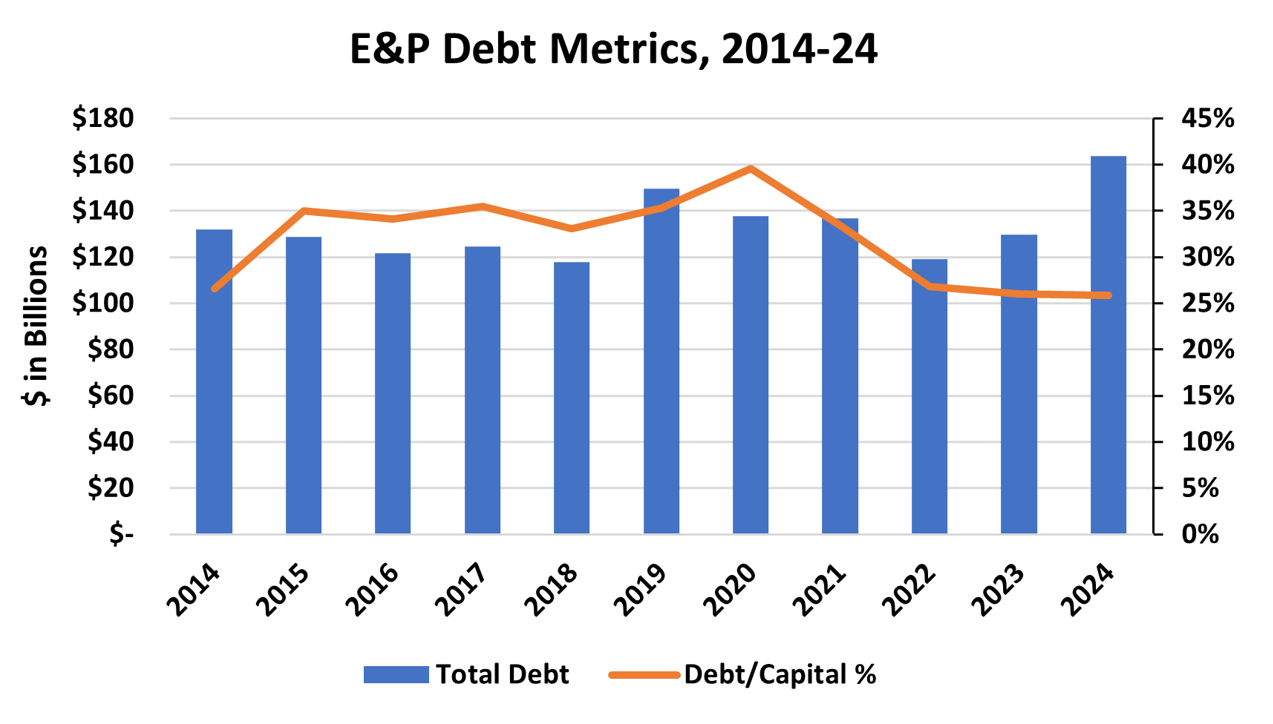

As shown in Figure 1 below, the debt-to-capital ratio (orange line and right axis) for the 39 major E&P companies we cover peaked at a concerning 40% in 2020 as commodity prices cratered. A strong price recovery and strict fiscal discipline led to a steep decline in leverage in 2021-22 as E&Ps fixated on keeping capital outlays far below cash flows and using the free cash to pay down debt, provide dividends and buy back shares. Despite declining oil prices, cost control was a major factor in sustaining that level in 2023.

Figure 1. E&P Debt Metrics, 2014-24. Source: Oil & Gas Financial Analytics LLC

The acquisition spree within the E&P sector drove total debt (blue bars and left axis) sharply higher in 2024: Total debt rose to $164 billion from $130 billion in 2023. The debt-to-capital ratio was unchanged because most of the transactions were funded with the issuance of equity, which also sharply boosted the total capital of the 39 companies we monitor.

Figure 2 below plots debt per barrel of oil equivalent (boe) of reserves (blue line) versus the PV10 value of oil and gas reserves (orange line), which is the primary collateral for most E&P lending. (The PV10 value represents the present value of estimated future oil and gas revenues — based on the first-of-the-month, 12-month average price — less estimated direct expenses and discounted at an annual rate of 10%.) WTI oil prices in the PV10 calculation fell 3.6% in 2024 to $75.48/bbl, while Henry Hub natural gas prices fell 16.7% to $2.35/MMBtu. As a result, the PV10/boe declined from $7.00/boe in 2023 to $6.54/boe in 2024 (right end of orange line).

About the song

“Solid as a Rock” was written by Bob Hilliard and David Mann. It was released as a 10-inch 78 RPM single on Decca Records by Ella Fitzgerald in 1950. The B-side of the single was Sugarfoot Rag by Hank Garland. It was recorded in New York City in March 1950. The song appears as the third song on Ella Fitzgerald: The Complete Decca Singles Vol. 4 1950-1955. It is also included on the compilation albums, Something to Live for and Swing for Private. From February to December 1950, Fitzgerald recorded 24 songs for Decca Records. Sy Oliver and his Orchestra backed Fitzgerald on eight of those songs. “Solid as a Rock” was featured in a Google Doodle on Fitzgerald, the Savoy Ballroom, and swing music in 2021. Personnel on the record were: Ella Fitzgerald (vocals), and Sy Oliver & his Orchestra, featuring Sy Oliver on trumpet and Billy Kyle on piano (orchestral accompaniment).

Ella Fitzgerald: The Complete Decca Singles Vol 4 1950-1955 is a 94-song compilation of Fitzgerald singles on the Decca Records label that was released as an MP3 by Verve Records in 2017.

Ella Fitzgerald was an American singer, songwriter, and composer. Known as the “First Lady of Song,” she was noted for her tone, phrasing, and her “horn-like” abilities in her scat singing techniques. She started her professional career singing with the Chick Webb Orchestra, with many appearances at the Savoy Ballroom in Harlem. She released 51 studio albums, 26 live albums, seven compilation albums, and 166 singles. She won 13 Grammy Awards, has a Grammy Lifetime Achievement Award, a Kennedy Center Honor, a National Medal of Arts, a Presidential Medal of Freedom, and a George and Ira Gershwin Award. Fitzgerald died at her home in Beverly Hills in June 1996 at the age of 79.