Over the past month, E&P executives have addressed shareholder and analyst concerns amid the murkiest market conditions since the onset of the pandemic in Q1 2020. One industry leader pointed out that on an inflation-adjusted basis, there have only been two quarters since 2004 when front-month oil prices have been as low as they are today (excluding 2020). In today’s RBN blog, we review what we heard from E&P brass — a measured response that melded confidence in the industry’s new fiscally conservative, shareholder-focused business model; modest spending reductions; and preparations for more substantial responses to future erosion in commodity pricing.

Join us at our historic 20th School of Energy!

School of Energy: Foundations is a two day, in person conference designed to help energy professionals better understand the forces shaping crude oil, natural gas, NGLs, refined products, and petrochemicals.

Attendees will learn from RBN experts, work with Excel based analytical models, participate in Q&As, and network with industry peers.

Build the foundation to better navigate volatile energy markets.

Producer commitment to their current investment strategy was showcased in a quote from Coterra Energy CEO Thomas Jorden, who said his company “is an ark, not a party boat.” The emphasis is on financial stability through maximizing free cash flow and prioritizing shareholder returns. Travis Stice, Jorden’s counterpart at Diamondback Energy, pointed out that the U.S. shale industry has evolved to this mature stage of development from the initial proof of concept, when E&Ps frequently outspent cash flow. Capital spending by the 38 companies we follow declined 3% from full-year 2023 to 2024 as oil prices fell and remained at the reduced level in their original 2025 guidance as E&P managements ignored exhortations from the new Trump administration to dramatically increase production.

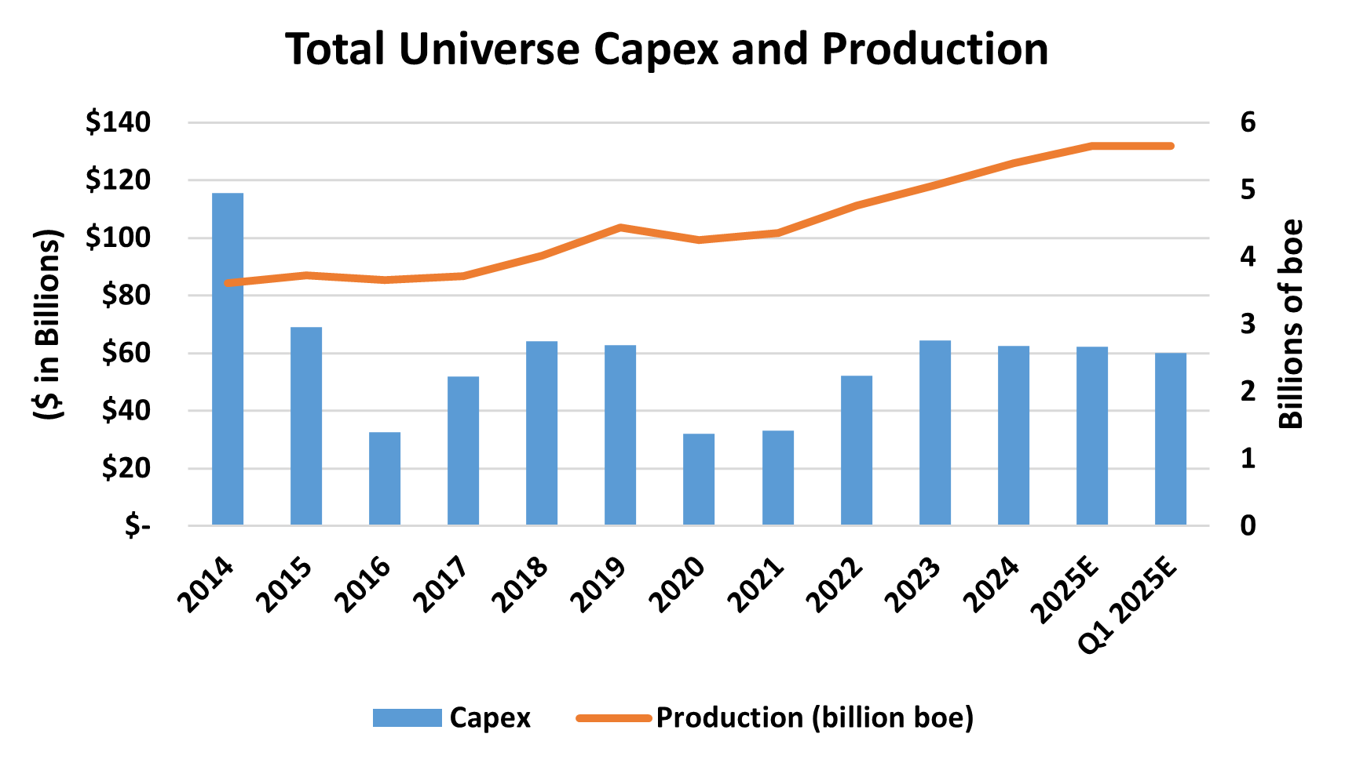

The average monthly price for WTI hit a 2025 peak in January at $74.68/bbl, then fell through the $70/bbl mark in March and averaged $60.76/bbl through the first three weeks of May. Concerns about future oil pricing have arisen based on slowing economies, OPEC production increases, and the potential impact of tariffs. As a result, producers cut 2025 capital spending estimates during their Q1 2025 earnings releases by 4%, or approximately $2 billion, to $60.1 billion (blue bar at far right and left axis in Figure 1 below). The Oil-Weighted E&Ps shaved off $1.1 billion, or 4%, from original capital outlay estimates to $23.3 billion. The Diversified E&Ps are guiding to a $1 billion, or 4%, reduction in capex to $25.9 billion. The Gas-Weighted E&Ps, which are seeing stronger pricing for most of their output, trimmed spending by a modest $125 million, a little under 1% of their capex budgets, to $10.9 billion.

Figure 1. E&P Capital Spending and Production, 2014-Q1 2025E. Source: Oil & Gas Financial Analytics, LLC

About the song

“Here Comes the Rain Again” was written by Annie Lennox and Dave Stewart. It appears as the first song on side one of the Eurythmics’ third studio album, Touch. Released as a single in January 1984, it went to #4 on the Billboard Hot 100 Singles chart. Personnel on the record were: Annie Lennox (vocals, keyboards), Dave Stewart (guitar, keyboards), the British Philharmonic Orchestra, and Michael Kamen (string arranger and conductor).

Touch was recorded in 1983 at The Church studio in London and produced by Dave Stewart. Released in November 1983, it went to #7 on the Billboard 200 Albums chart and has been certified Platinum by the Recording Industry Association of America. Three singles were released from the LP.

Eurythmics was a British pop duo formed in London in 1980 by Annie Lennox and Dave Stewart. Both had previously been in the British punk band, The Catch, and the British pop band, The Tourists. They achieved international success with the Eurythmics’ single, “Sweet Dreams (Are Made of This),” which went to #1 on the Billboard Hot 100 Singles chart and was certified Gold by the RIAA in 1983. They released eight studio albums, a soundtrack album, a live album, two compilation albums, an EP, and 33 singles. They sold more than 75 million records worldwide. They have won a Brit Award, a Grammy Award, an MTV Video Music Award, and were inducted into the Songwriters Hall of Fame in 2020 and the Rock and Roll Hall of Fame in 2022. The group unofficially broke up in 1990 but has had a few reunions since then. Lennox has a successful solo career, and Dave Stewart is a highly regarded record producer. In March, Lennox played her first live performance in over six years at the Royal Albert Hall in London. Stewart will be embarking on a European summer tour with Eurythmics, featuring Vanessa Amorosi on vocals, beginning in July.