The summer movie season opened with the latest — and reportedly last — entry in the Tom Cruise-propelled “Mission: Impossible” franchise called “The Final Reckoning.” That title reminded us that, to E&P executives, the commodity price crash at the onset of the pandemic in 2020 must have seemed like the final blow in a series of financial crises that brought many of their companies to the verge of bankruptcy. But in a dramatic, “Mission: Impossible”-style recovery, producers restored their battered balance sheets and won back investors by radically shifting cash allocations. In today’s RBN blog, we’ll review the rise of the new E&P hero — dividends — and analyze how producers apportioned cash flows in Q1 2025.

A hair-raising 90% erosion in U.S. E&P share prices between 2014 and 2020, as measured by the S&P E&P index, resulted largely from individual investors fleeing the oil and gas sector. Money had surged to the sector on the promise of substantial long-term growth with the Shale Revolution and the surge in crude oil prices to over $100/bbl in 2014. But a long, subsequent decline in realizations and massive overinvestment led to growing debt, massive losses and shrinking market caps. With E&Ps paying paltry dividends — just over 1%, on average, in 2019 compared with 4.6% for the integrated majors and 5.45% for midstream companies — oil and gas producers were the worst performing S&P group in five of seven years between 2014 and 2020.

Canadian crude output is rising, requiring new export routes. As traditional pathways face constraints, the U.S. Rockies—especially the Guernsey, WY hub—are emerging as key corridors for moving Canadian heavy crude to downstream markets, including the Gulf Coast.

No wonder E&Ps pivoted from their failed growth-at-all-costs strategy to target individuals and institutions who prioritized return on investment. Producers prioritized boosting cash flows over capital investment to wield a powerful tool to grow share prices: substantially higher dividends. With a big assist from the post-pandemic surge in oil prices, the average E&P dividend across the entire sector more than tripled to 3.28% in 2022 and 3.98% in 2023, with several major producers adding special dividends that brought total yields to near or even above 10%. These yields, which exceeded payouts by integrated majors like ExxonMobil and Chevron, resulted in the E&P sector becoming the top-performing S&P group in both years.

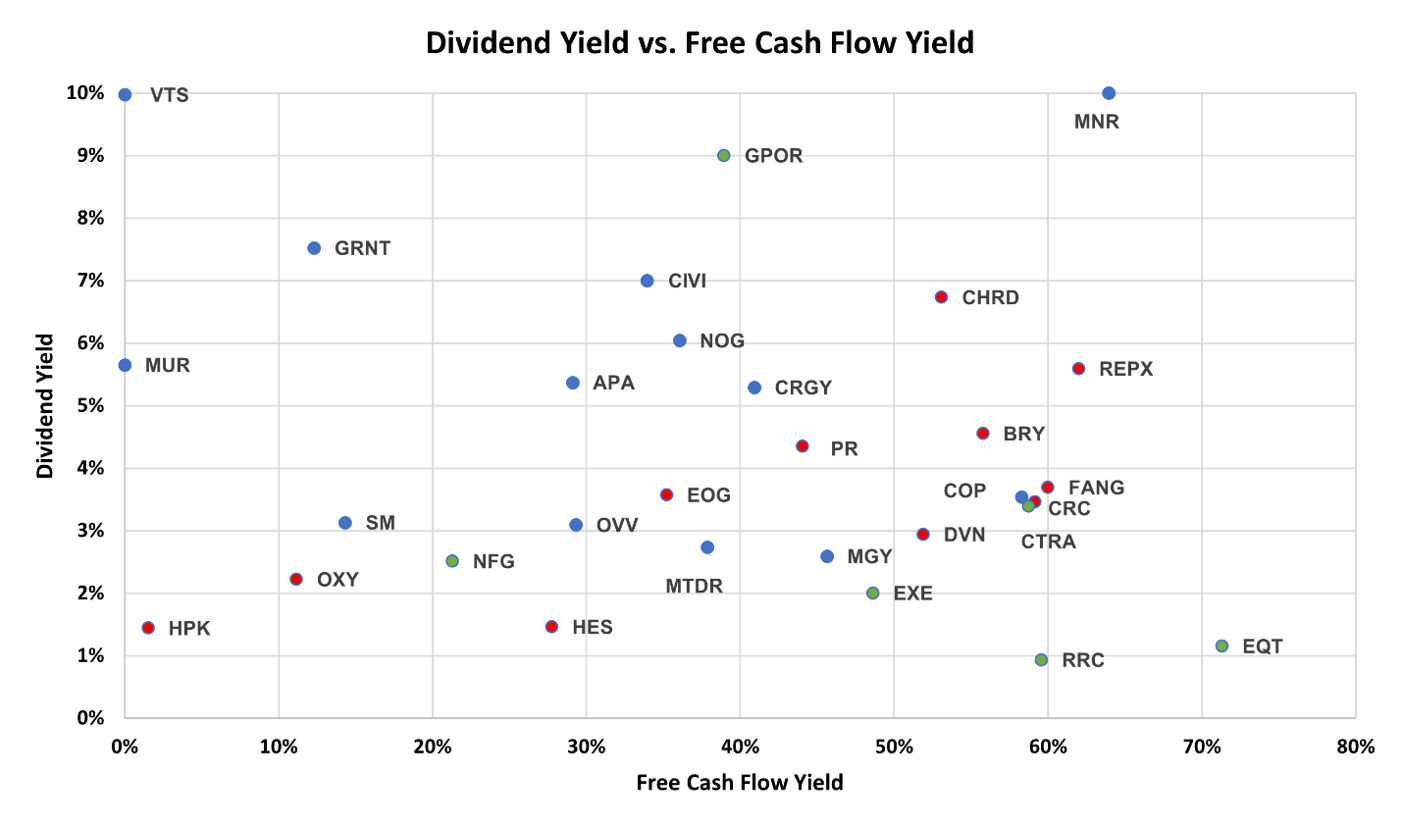

Although oil prices have slipped from their 2022-23 highs, the 39 large E&P companies we follow have managed to largely sustain their higher-than-historical dividend payouts that restored investor support. Figure 1 below shows the Q1 2025 yields (y axis) for the 28 of these companies that pay dividends (colored dots with stock symbols) compared with each company’s free cash flow yield (x axis). (For a list of stock symbols and company names, click here. Red dots are for companies in the Oil-Weighted group, blue dots are for the Diversified group, and green dots are for the Gas-Weighted group.) The free cash flow yield is the percentage of cash flow retained by an E&P after funding its capital investment program. The median free cash flow is 40% and the median dividend yield is 3.65%, still an elevated return on a historical basis. The median free cash flow return in the most recent quarter was up slightly from an average 37% in 2023.

Figure 1. E&Ps’ Free Cash Flow Yield vs. Dividend Yield, Q1 2025. Source: Oil & Gas Financial Analytics, LLC

About the song

“Mission: Impossible Theme” was written by Lalo Schifrin and appears as the first song on side one of Music From Mission: Impossible, the soundtrack album by Lalo Schifrin. With the working title of “Burning Fuse,” probably referring to the opening segment of the 1960s television show, Schifrin composed the song to a beat that spells out the letters, “M.I.” in Morse Code. The song was recorded in Hollywood in October 1967 and produced by Tom Mack. Released as a single in November 1967, it went to #7 on the Billboard Easy Listening and #41 on the Billboard Hot 100 Singles chart. It has been certified Gold by the Recording Industry Association of America (RIAA). It was inducted into the Grammy Hall of Fame in 2017 and remains a popular song for marching bands to play at sporting events. Personnel on the record were: Lalo Schifrin (piano, harpsichord, arranger, conductor), Mike Melvoin, Paul Beaver (keyboards), Bob Bain, Tommy Tedesco (guitar), Ray Brrfown (acoustic bass), Carol Kaye (electric bass), Eral Palmer, Shelly Manne (drums, percussion), Adolfo Valdes (bongos, conga), Ken Watson, Emil Richards (percussion), Bill Plummer (sitar). Dorothy Remsen (harp), along with five trumpet players, five trombone players, four French horn players, five reed players, fifteen violinists, four violists, and five cellists.

The album Music From Mission: Impossible features music composed and conducted by Lalo Schifrin for the TV series Mission: Impossible. Recorded in Hollywood in October 1967 and produced by Tom Mack, the album was released in November 1967. It went to #41 on the Billboard 200 Albums chart. One single was released from the LP.

Lalo Schifrin, who turned 93 on June 21, is an Argentine-American pianist, composer, arranger and conductor. He has a large catalog of film and television score credits dating to the 1950s. In addition to Mission: Impossible, he wrote the score to Cool Hand Luke, Bullitt, Enter the Dragon and The Amityville Horror. He has released 52 studio albums, 43 soundtrack albums and a live album. Schifrin has won five Grammy Awards, an Honorary Academy Award from the Academy of Motion Picture Arts and Sciences, and a star on the Hollywood Walk of Fame. In 2024, in collaboration with Rod Schejtman, Schifrin composed a 35-minute symphony for full orchestra that is a tribute to their homeland, Argentina.