The original Cactus Pipeline was a pioneer in moving large volumes of crude oil from the Permian and the Eagle Ford to the Corpus Christi area, which quickly became a leader in U.S. crude exports. Cactus II, an even longer and larger pipeline that came online in H2 2019, only added to Corpus Christi’s export prominence. But the competition with Permian-to-Houston pipelines is fiercer than ever and negotiated rates on pipelines to the Texas Gulf Coast are under pressure. In today’s RBN blog, we look at the Cactus I and Cactus II pipelines and their significance.

Analyst Insights are unique perspectives provided by RBN analysts about energy markets developments. The Insights may cover a wide range of information, such as industry trends, fundamentals, competitive landscape, or other market rumblings. These Insights are designed to be bite-size but punchy analysis so that readers can stay abreast of the most important market changes.

The EIA reported total U.S. propane/propylene inventories had a build of 2.63 MMbbl for the week ended August 15, which was more than industry expectations for an increase of 2.2 MMbbl and the average build for the week of 1.5 MMbbl. Total U.S.

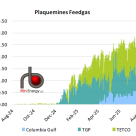

Venture Global’s Plaquemines terminal averaged more than 3 Bcf/d of feedgas last week for the first time, as the company makes more progress.

| Report | Title | Published |

|---|---|---|

| NATGAS Billboard | NATGAS Billboard - August 21, 2025 | 5 hours 9 min ago |

| Chart Toppers | Chart Toppers - August 21, 2025 | 8 hours 24 min ago |

| TradeView Daily Data | TradeView Daily Data - August 20, 2025 | 21 hours 46 min ago |

| Crude Oil Billboard | Crude Oil Billboard Weekly - August 20, 2025 | 23 hours 8 min ago |

| NATGAS Appalachia | NATGAS Appalachia Weekly – August 20, 2025 | 23 hours 15 min ago |

A crude oil leak last Tuesday at the Enterprise Crude Houston (ECHO) terminal disrupted regional flows and caused crude differentials to move higher over the course of the week. While the spill was swiftly addressed by terminal owner Enterprise Products Partners, it still affected inbound and outbound operations for a few days. In today’s RBN blog, we discuss the role of the ECHO terminal and show how even an isolated incident can quickly have an impact on the market.

A few months ago, Enbridge unveiled its plans to expand its massive Mainline and smaller Express/Platte crude oil pipeline systems into the U.S. Midwest/Great Plains. We blogged about those plans, and followed up with a look at how the incremental volumes of Western Canadian crude on the Mainline and Express/Platte might move south from PADD 2 to where they’re wanted most: the Gulf Coast. In today’s RBN blog, we discuss efforts to piece together a more direct pipeline route from Alberta to Cushing and on to the Texas/Louisiana coast.

The build-out of the Permian’s midstream infrastructure over the past 10 years has created extraordinary opportunities for startup companies, most of them backed by private equity. Each of us could cite several examples of midstreamers that, with a combination of guile and grit, developed gathering systems, gas processing plants, pipelines and other infrastructure to serve the fast-growing needs of producers and shippers. In many cases, the assets they constructed were later sold — often at a hefty profit — to much larger firms. As we discuss in today’s RBN blog, even in the midst of sector consolidation, the entrepreneurial spirit of smaller Permian midstreamers continues.

Odds are there’s never been a busier, more frantic time for natural-gas-related infrastructure development in Texas and Louisiana than right now. Construction is underway or imminent at no fewer than seven Gulf Coast LNG export terminals with a combined capacity of 16 Bcf/d. Big-tech firms and midstreamers are touting the potential for several Bcf/d more in gas-fired power demand for data centers in the two states.

The U.S. refining industry has undergone a number of changes in recent years and more turbulence looks likely as global economic and trade patterns shift and energy transition moves forward. For some refineries, this has led to closures due to weak profits, rising regulatory costs and declining demand for products, particularly gasoline. But other refineries have prospered — and even invested in expansions — while the U.S. industry as a whole has evolved into the most competitive system in the world. Overall, the prospects have been very regionally (and even facility) specific. As detailed in the most recent Future of Fuels report from our Refined Fuels Analytics (RFA) practice, this regional differentiation will continue and shift over the coming years. In today’s RBN blog, we’ll discuss what we expect for the U.S. refining industry — where closures will likely take place, where the industry might actually add capacity, and the reasons for those actions.

Data centers are a buzzy topic in the energy industry, and while there is still a lot of fuzziness about what will actually get built and how much natural-gas-fired power will be needed to support these projects, there’s no doubt that major technology companies are well along in planning a number of massive data centers across the country. In today’s RBN blog, we’ll offer a snapshot of the plans announced by tech giants Microsoft, Amazon, Alphabet (Google) and Meta (Facebook).

The oil and gas industry is always working to develop the most efficient methods for unlocking more hydrocarbons. To cut costs and maximize output from their acreage, some companies are rolling out more creative well designs, such as U-turn (aka “horseshoe”) and J-hook wells, which use dramatic, 180-degree underground turns to access more oil and gas from each location. In today’s RBN blog, we’ll discuss the benefits of these approaches and the technical hurdles associated with drilling these deep bends underground.

Any number of things can impact the price of specific types of crude oil at various locations — supply interruptions, takeaway constraints and refinery outages, to name just a few. Every so often, the stars align and just about all those factors narrow the differential between, say, Western Canadian Select (WCS) and West Texas Intermediate (WTI) at the U.S. Gulf Coast to near-record levels. Well, that’s happening now, for the first time in five years. In today’s RBN blog, we discuss the shockingly small WCS/WTI differential and what’s driving it.

The European Union (EU) appears poised to substantially increase its imports of U.S. LNG after reaching a trade deal with the Trump administration that includes a pledge to purchase $750 billion worth of U.S. energy over three years. The trade agreement and the EU’s plans to phase out deliveries of Russian LNG and piped-in natural gas by 2027 may end up being a big positive for U.S. producers. But that doesn’t mean it’s all clear sailing, thanks to competition with Qatar and uncertainty around EU regulations. In today’s RBN blog, we look at how U.S. exporters could still get squeezed on price and volume between today and 2030.

Not long ago, several large-scale carbon-capture projects had plenty of momentum, fueled by a push toward decarbonization and expanded federal tax credits. But while progress on many projects has slowed as they faced a host of problems, Tallgrass’s plan to convert its Trailblazer pipeline from natural gas service to carbon dioxide (CO2) has had a comparatively smooth ride, thanks in large part to an engagement strategy that has allowed it to navigate the trickiest potential complication — local opposition. In today’s RBN blog, we review Trailblazer’s conversion, examine why Tallgrass’s strategy has succeeded where similar projects have failed, and look at what happens next.

The San Juan Basin in northwestern New Mexico and southwestern Colorado has seen more than its share of booms and busts in the last 100-plus years. During the Shale Era, natural gas production in the 7,500-square-mile basin has been slowly declining, undercut by competition from more prolific, better-situated wells in the Permian and Eagle Ford. But a small band of “San Juan believers” think the region is poised for yet another rebound, this time due to what they view as massive, untapped potential in the basin’s Mancos Shale. In today’s RBN blog, we discuss recent developments in the San Juan — and the basin’s extensive pipeline infrastructure.

Western Canadian crude oil production is rising fast. To keep pace, Enbridge is planning expansions to its pipelines into the Midwest and Great Plains. But PADD 2 refineries are maxed out on heavy crude, so virtually all those incremental barrels will need to keep flowing south to refineries and export terminals along the Gulf Coast. Can the pipelines from PADD 2 to PADD 3 handle the higher volumes? In today’s RBN blog, we discuss the knock-on effects of rising Western Canadian production and Enbridge’s pipeline expansions.

MPLX’s July 31 announcement that it has reached an agreement to acquire Northwind Midstream for $2.375 billion puts a spotlight on two undeniable trends. First, the acquisition is the latest in what by now is a long series of multibillion-dollar deals by midstream giants to expand their Permian-to-Gulf, “wellhead-to-water” networks that gather, process, transport and export crude oil, natural gas and/or NGLs. Second, Northwind has been a pioneer in gathering and processing unusually sour associated gas in the prolific Northern Delaware Basin, an area of particular interest to a growing number of E&Ps. In today’s RBN blog, we discuss the deal and what it brings to MPLX.

U.S. E&Ps’ strategic shift from growth at any cost to a laser focus on cash flows to fund shareholder returns revitalized their investor base. But that strategy has been challenged as crude oil prices have eroded since their mid-2022 peak, with producers struggling to balance the need to maintain output and the pressure to sustain dividends. In today’s RBN blog, we’ll see how things are going with the oil and gas companies that bear no responsibility for the costs and complications associated with the finding, development and production of hydrocarbons — the entities that own mineral and royalty interests.

Crude oil producers in the prolific Permian Basin have plenty of options to move their barrels, especially since pipeline capacity currently exceeds production, but not every route out of the basin is equal. One of the hottest destinations for Permian crude is Houston, which boasts an attractive mix of refining and export demand. In today’s RBN blog, we look at the pipelines that transport Permian crude to Houston, discuss why it’s such a vital spot, and preview our latest Drill Down Report.