Buoyed in part by early optimism about the Trump administration’s potentially positive impact on the economy and the oil and gas industry, the WTI spot oil price reached a five-month high of nearly $76/bbl in January. But the optimism and oil prices have steadily eroded due to the impact of tariffs, trade wars and stubborn oilfield service inflation. In today’s RBN blog, we’ll look at the impact of the January price spike on Q1 2025 earnings and analyze the potential impact of a much lower price scenario in Q2 2025.

Build your energy market expertise at the 20th School of Energy: Foundations.

Learn from RBN experts, participate in hands-on Excel modeling, connect with industry peers, and gain a stronger understanding of today's interconnected energy markets.

September 9-10 | Houston, TX

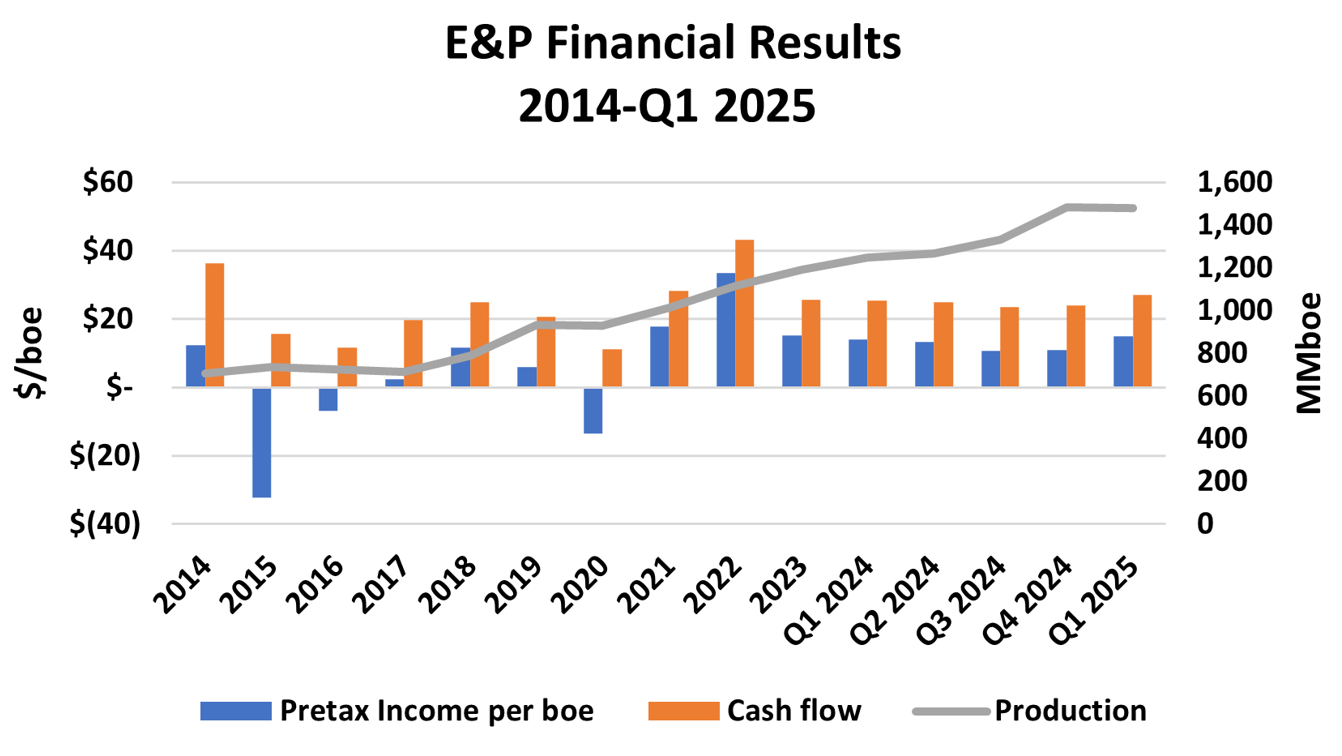

The strong January spot price drove the Q1 2025 average to $71.83/bbl, up 2% from a three-year low of $70.32/bbl in Q4 2024. However, a nearly 70% increase in natural gas prices during the quarter drove a 9% increase in the average oil and gas price to $38.91/boe, the highest since Q1 2023. As a result, the earnings for the 40 E&Ps we cover totaled $22.1 billion in Q1 2025, up 37% to $14.96/boe (blue bar to far right and left axis in Figure 1 below), up from $10.89/boe in Q4 2024. Cash flow grew to $40.1 billion, increasing 13% to $27.15/boe (orange bar and left axis) over the same time period.

Figure 1. E&P Financial Results and Production, 2014-Q1 2025. Source: Oil & Gas Financial Analytics, LLC

The quarter-over-quarter increase in performance appears less impressive when viewed from a broader historical perspective. Average commodity prices for the quarter most closely parallel the results in Q3 2021, when the WTI spot price was just under $71/bbl and the average Henry Hub spot price was within $0.20 of the Q1 2025 price at $4.35/MMBtu. While the average realization in Q3 2021 was just $1.83/boe higher, the pre-tax operating income was $20.42/boe, 36% higher than the recently completed quarter. A major factor is a $2/boe increase in production costs over the last three years, driven by significant post-pandemic oilfield equipment and services inflation. Depreciation, depletion and amortization (DD&A) costs were also more than $1/boe higher, reflecting the higher costs of finding and acquiring reserves. Persistently higher costs are likely to exacerbate the impact of lower commodity prices in Q2 2025 and beyond.

The comparison of costs for Q1 2025 over the previous quarter is more positive. Lifting costs grew 2% to $11.77/boe as production costs increased 2% to $9.86/boe and production taxes rose 7% to $1.90/boe. DD&A expenses declined 3% to $10.92/boe, while impairment charges fell 40% to $0.96/boe. Exploration outlays were down 9% to $0.30/boe.

About the song

“Calm Before the Storm” was written by Patrick Stump, Joe Trohman, Jared Logan and Pete Wentz. It first appeared as the second song on Fall Out Boy’s second EP, Fall Out Boy’s Evening Out With Your Girlfriend, released in March 2003. It also appears as the 10th song on Fall Out Boy’s debut studio album, Take This to Your Grave, released in May 2005. Personnel on the record were: Patrick Stump (lead vocals, rhythm guitar), Pete Wentz (bass, backing vocals), Joe Trohman (lead guitar, backing vocals) and Andy Hurley (drums, percussion).

Take This to Your Grave was recorded between December 2002 and March 2003 at Smart Studios in Madison, WI; Gravity Studios in Chicago; and Rosebud Studios in Skokie, IL. Produced by Sean O’Keefe, the album was released in May 2003 and went to #10 on the Billboard Top Catalog Albums chart and # 140 on the Billboard 200 Albums chart. It has been certified Gold by the Recording Industry Association of America. Two singles were released from the LP.

Fall Out Boy is an American pop/punk band formed in Wilmette, IL, a suburb of Chicago, in 2001. Fueled by the pop songwriting skills of lyricist Pete Wentz and composer Patrick Stump, the group has had a string of hit singles and albums in the pop/punk genre. They have released eight studio albums, two live albums, two compilation albums, nine EPs and 39 singles. They have been nominated for two Grammy Awards and have won five MTV Video Music Awards. They continue to record and tour and will be featured at select festival dates this summer.