U.S. E&Ps’ strategic shift from growth at any cost to a laser focus on cash flows to fund shareholder returns revitalized their investor base. But that strategy has been challenged as crude oil prices have eroded since their mid-2022 peak, with producers struggling to balance the need to maintain output and the pressure to sustain dividends. In today’s RBN blog, we’ll see how things are going with the oil and gas companies that bear no responsibility for the costs and complications associated with the finding, development and production of hydrocarbons — the entities that own mineral and royalty interests.

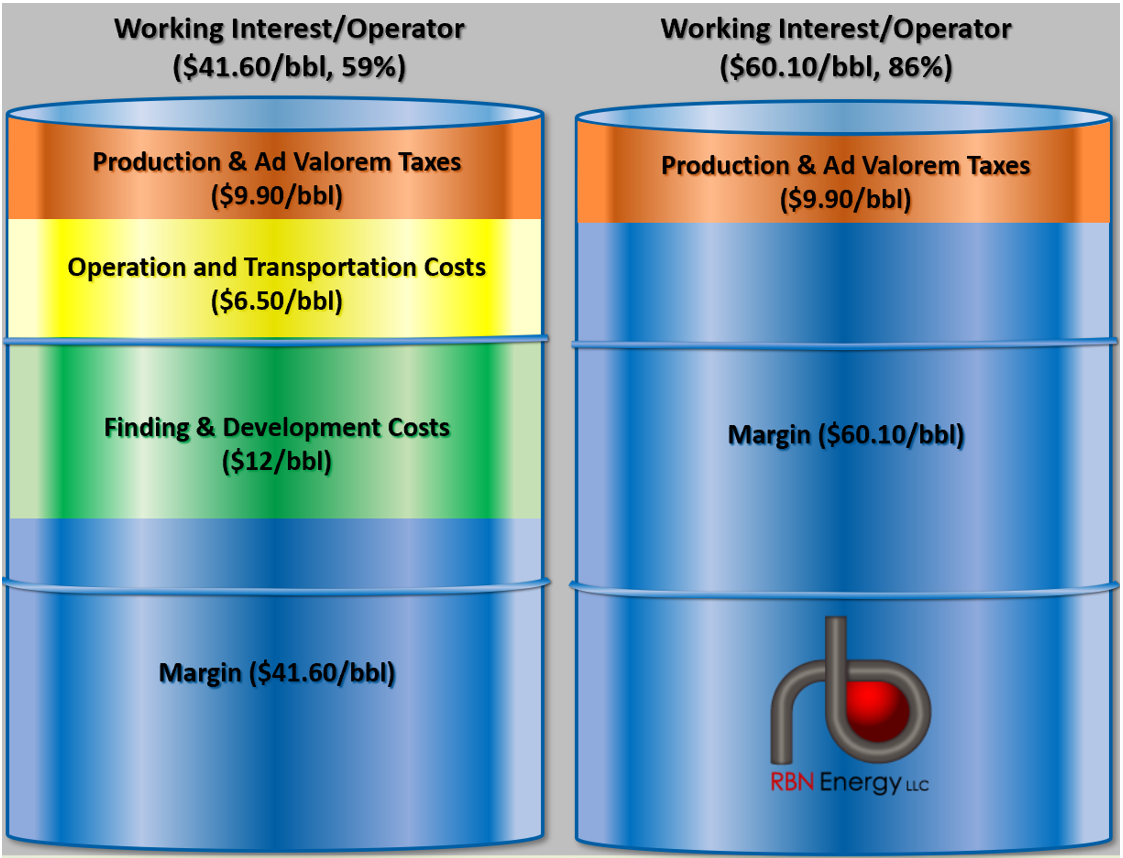

We first discussed this industry segment two years ago in Money for Nothing, which provided an extensive overview of mineral and royalty interests, which receive about 20% of the gross revenues generated by oil and gas wells. Figure 1 below illustrates the higher percentage of revenues received by holders of mineral and royalty interests on a barrel of crude priced at $70/bbl. In this example, the working interest holders (left barrel) are responsible for the $12/bbl of finding and development costs (F&D; green section of barrel), the $6.50/bbl of operating and transportation costs (yellow section), and the $9.90/bbl in taxes (orange section), resulting in a net of $41.60/bbl, or 59% of the gross revenue. The mineral/royalty interests on the right, in turn, are responsible only for the $9.90/bbl in taxes, resulting in net revenue of $60.10/bbl, or 86% of gross revenue.

Figure 1. How Crude Oil Proceeds Differ Between Working Interests and Royalty Owners. Source: Oil & Gas Financial Analytics, LLC

Because they incur little or no production and exploration expenses, it’s no surprise that significantly higher proportions of realized revenues of royalty/mineral trusts (RTs) flow through to the bottom line. As shown in Figure 2 below, Q1 2025 pre-tax operating cash flows (green bar segments in group to far right) and operating income (dark-blue bar segments) for the seven RTs we monitor (Kimbell, Viper, Dorchester, Blackstone, Sitio, Freehold and PrairieSky) were $38.33/boe and $24.62/boe, respectively. That’s 41% and 65%, respectively, higher than the average for our universe of 40 E&P companies (light blue and orange bars). The RTs retained 92% of realized pricing as cash flow and reported 59% of realized pricing as income, compared with 70% and 38%, respectively, for the E&Ps. Only the depreciation, depletion and amortization (DD&A) expenses of RTs ($13.21/boe) exceeded that of E&Ps ($10.92/boe), likely because of the higher acquisition costs by royalty companies.

About the song

“Smart Money” was written by Mark Knopfler and appears as the 12th song on his 10th studio album, One Deep River. The song appears to be Knopfler’s soliloquy to chasing fame in Tinseltown and that ever-elusive brass ring. It features his laid-back vocals and an island groove. Personnel on the record were: Mark Knopfler (lead vocals, electric guitar), Guy Fletcher (synthesizer), Richard Bennett (acoustic guitar), Glenn Worf (bass), Ian Thomas (drums), Greg Leisz (pedal steel guitar), Jim Cox (Hammond organ), Danny Cummings (percussion), and Emma and Tamsin Topolski (backing vocals).

One Deep River was recorded in 2023 at Knopfler’s British Grove Studio in London. Produced by Knopfler and Guy Fletcher, the album was released in April 2024 and went to #157 on the Billboard 200 Albums chart. The album cover depicts the Tyne Bridge over the River Tyne, which passes through Knopfler’s hometown of Newcastle upon Tyne. Three singles were released from the LP.

Mark Knopfler is a British singer, songwriter, guitarist and record producer. He was a founding member of the rock band Dire Straits, from its formation in 1977 to its dissolution in 1995. With Dire Straits, he released six studio albums, five live albums, two compilation albums, three EPs, and 31 singles. Dire Straits have sold more than 100 million albums worldwide. As a solo artist, he has released 10 studio albums, nine soundtrack albums, two compilation albums, three EPs and 26 singles. He has won four Grammy Awards, three Brit Awards and an Ivor Novello Lifetime Achievement Award. In 1999, he was awarded an OBE. Dire Straits were inducted into the Rock and Roll Hall of Fame in 2018. Knopfler continues to record and has discussed doing a final world tour in late 2025 through 2026, but no dates or locations have been announced.