Western Canadian crude oil production is rising fast. To keep pace, Enbridge is planning expansions to its pipelines into the Midwest and Great Plains. But PADD 2 refineries are maxed out on heavy crude, so virtually all those incremental barrels will need to keep flowing south to refineries and export terminals along the Gulf Coast. Can the pipelines from PADD 2 to PADD 3 handle the higher volumes? In today’s RBN blog, we discuss the knock-on effects of rising Western Canadian production and Enbridge’s pipeline expansions.

Join us at our historic 20th School of Energy!

School of Energy: Foundations is a two day, in person conference designed to help energy professionals better understand the forces shaping crude oil, natural gas, NGLs, refined products, and petrochemicals.

Attendees will learn from RBN experts, work with Excel based analytical models, participate in Q&As, and network with industry peers.

Build the foundation to better navigate volatile energy markets.

A few months ago, in Here, There and Everywhere, we examined Enbridge’s plan to spend up to C$2 billion (US$1.5 billion) by 2028 to improve the efficiency and reliability of its 3.28-MMb/d Mainline pipeline system from Alberta to the Midwest that the midstreamer has said will increase its 96% utilization rate by 1% or 2%. Enbridge also is investing another C$1.5 billion (US$1.1 billion) by 2027 on a multiphase optimization project that will boost the system’s capacity by 150 Mb/d — and maybe more, if demand warrants. In addition, the company is looking to add up to 30 Mb/d of capacity to its 310-Mb/d Express-Platte pipeline system, which runs from Hardisty, AB, to Wood River, IL, just west of the Patoka, IL, crude oil hub. Enbridge has hinted that further expansions to Express-Platte are possible.

More recently, in You’ve Got a Friend in Me, we discussed our latest forecast for Western Canadian crude oil production and stacked that up against available and planned pipeline capacity out of the region. The bottom line? Even with the May 2024 startup of the 590-Mb/d Trans Mountain Expansion Project (TMX) to Canada’s British Columbia coast, 180 Mb/d in planned expansions to Enbridge’s pipelines (150 Mb/d on the Mainline and 30 Mb/d on Express-Platte) by 2027, and higher utilization of the Mainline (maybe another 50 Mb/d), Western Canadian producers and shippers may well face a takeaway capacity crunch by late 2028 — only three years from now. In other words, keep those capacity-adding projects comin’!

In today’s blog, we assume that our production forecast is on point and that Enbridge will find shipper support for another 150 Mb/d in Mainline expansions, resulting in a total of 380 Mb/d of incremental flows down the Mainline and Express-Platte systems by the late 2020s (150 from initial Mainline expansion + 30 from Express-Platte expansion + 50 from Mainline efficiencies + 150 from future Mainline expansion). That all raises a new and important question: Where will that extra 380 Mb/d end up?

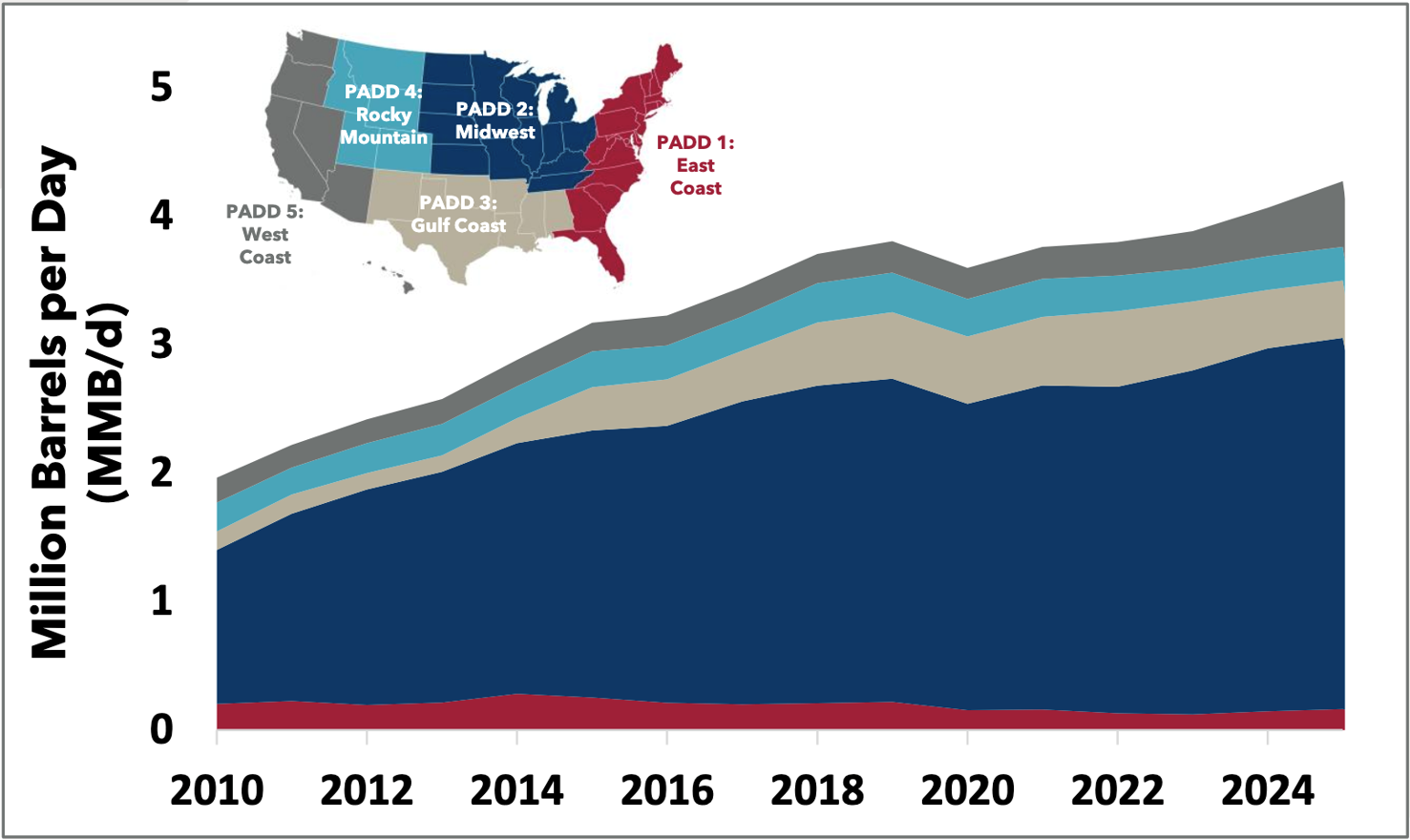

Let’s begin with a little background. Canadian crude oil exports to the U.S. have more than doubled over the past 15 years, from about 2 MMb/d in 2010 to 4.2 MMb/d in 2024. PADD 2 (Midwest/Great Plains) is by far the largest destination, accounting for two-thirds (or about 2.8 MMb/d; dark-blue layer in Figure 1 below) of last year’s total. Of the 2.8 MMb/d that ended up in PADD 2, ~2.3 MMb/d was heavy crude and the rest (~500 Mb/d) was light/medium crude — together, these types accounted for 73% of the more than 3.8 MMb/d of crude PADD 2 refineries received, on average, in 2024, with Western Canadian heavy accounting for 60% of their crude slate and Western Canadian light/medium making up 13%. (The 27% balance was U.S.-sourced light oil.)

Canadian Crude Oil Exports to the U.S. by PADD

Figure 1. Canadian Crude Oil Exports to the U.S. by PADD. Sources: EIA and Canadian Association of Petroleum Producers

About the song

“Take the Long Way Home” was written by Roger Hodgson and appears as the first song on side two of Supertramp’s sixth studio album, Breakfast in America. The song addresses going home, whether that is a physical place or a place within your heart. It was the last song written for Breakfast in America. Released as a single in October 1979, it went to #10 on the Billboard Hot 100 Singles chart. Personnel on the record were: Roger Hodgson (lead vocal, keyboards, harmonica, guitar), Rick Davies (keyboards, backing vocals), John Helliwell (sax, clarinet, backing vocals), Dougie Thomson (bass) and Bob Siebenberg (drums).

Breakfast in America was recorded between May and December 1978 at Village Recorder Studio B in Los Angeles. Produced by Peter Henderson and Supertramp, the album was released in March 1979 and went to #1 on the Billboard 200 Albums chart. It has been certified 4X Platinum by the Recording Industry Association of America. It won two Grammy Awards in 1980 and remains Supertramp’s best-selling album. Four singles were released from the LP. The album cover features American actress Kate Murtagh as a waitress, while the back cover features the band having breakfast at Bert’s Mad House, a diner in Los Angeles. Four singles were released from the LP.

Supertramp was a British rock band formed in London in 1970 by songwriters Roger Hodgson and Rick Davies, along with saxist and clarinetist John Helliwell, bassist Dougie Thomson and drummer Bob Siebenberg. Hodgson left the band to pursue a solo career in 1983, and the band continued until 1988, reforming in various configurations until 2012. Nineteen members passed through the band during its run. They released 11 studio albums, six live albums, four compilation albums and 25 singles and have sold more than 60 million records worldwide.