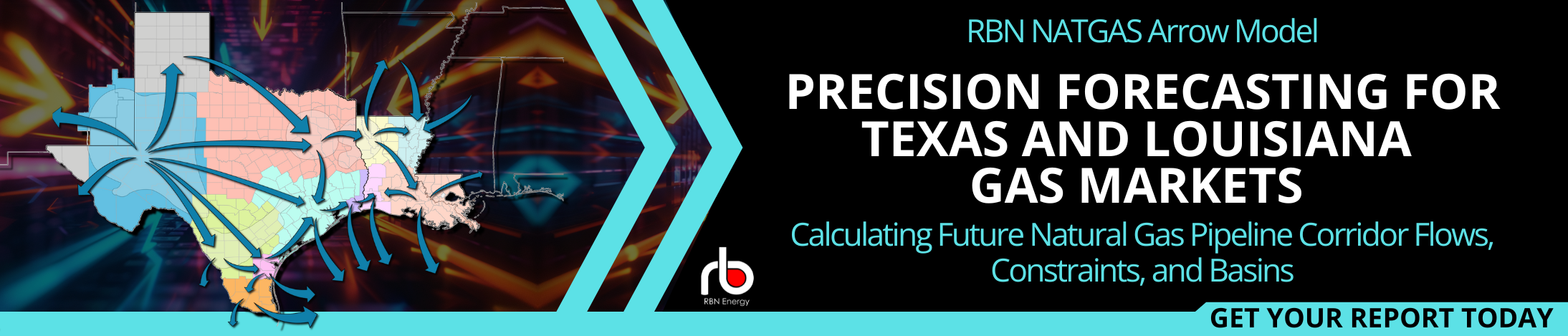

Odds are there’s never been a busier, more frantic time for natural-gas-related infrastructure development in Texas and Louisiana than right now. Construction is underway or imminent at no fewer than seven Gulf Coast LNG export terminals with a combined capacity of 16 Bcf/d. Big-tech firms and midstreamers are touting the potential for several Bcf/d more in gas-fired power demand for data centers in the two states. And developers are advancing a slew of inter- and intrastate pipeline projects aimed at bringing Permian, Haynesville and other gas to where it will be needed. It’s admittedly hard to keep track of it all, but in today’s RBN blog, we take a snapshot of where things stand today and highlight the highlights.

Texas and Louisiana already are crisscrossed by tens of thousands of miles of gas pipelines large, medium and small. But those extraordinary networks aren’t enough for what will be needed over the next five years. The Shale Revolution, the world’s push toward lower-carbon sources of energy and Russia’s war on Ukraine, among other things, have combined to make fast-rising U.S. LNG exports a global necessity. As we track in RBN’s weekly LNG Voyager report, feedgas flows to Gulf Coast LNG export terminals have recently topped 15 Bcf/d, and those volumes will roughly double over the next six to seven years as expansions at existing facilities and new terminals are brought online.

And that’s not all. As we’ve discussed in a number of blogs, most recently in I Know Places, the Lone Star and Bayou states also have become hotbeds for the development of large-scale data centers. Each of these will require at least several hundred megawatts of around-the-clock power, with new gas-fired power plants being the most logical (and quickest) way to meet that need. For example, Meta Platforms (parent of Facebook and Instagram) is planning a $10 billion complex in Richland Parish, LA, that will be powered in large part by three new Entergy Louisiana gas-fired power plants totaling more than 2,200 MW. (That’s up to 330 MMcf/d of gas demand.) Several proposed data-center projects in Texas could be much bigger, with much higher demand for power (and gas).

The incremental gas demand from new LNG export capacity and new data centers in Texas and Louisiana will be met primarily from rising gas production in the Permian and an expected resurgence in the Haynesville, with likely assists from other shale plays (especially the Eagle Ford). But there’s a catch: Existing pipelines from these plays to new and emerging gas-demand centers are or will be essentially maxed out. New pipeline capacity will be needed, and will be coming in spades.

About the song

“Helter Skelter” was written by Paul McCartney and credited to Lennon-McCartney. It appears as the sixth song on side three of The Beatles’ ninth studio album, The Beatles, commonly referred to as “the White Album.” McCartney intended to write a song as heavy and loud as possible. He was inspired by The Who’s 1967 single, “I Can See for Miles.” He succeeded in producing a song that preceded heavy metal. The song has been covered by artists such as Motley Crue, Siouxsie & the Banshees, Aerosmith, and Oasis. Charles Manson felt the song held a message of impending apocalypse, when in fact it was written about a British fairgrounds attraction ride. Personnel on the record were: Paul McCartney (lead vocals, lead guitar), John Lennon (six-string bass), George Harrison (guitar, guitar slides), Ringo Starr (drums; “I’ve got blisters on my fingers” shout at the end).

The Beatles (White Album) was recorded at Abbey Road and Trident studios in London between May and October 1968. The double LP was produced by George Martin and released in November 1968. It went to #1 on the Billboard 200 Albums chart and has been certified 24X Platinum by the Recording Industry Association of America. No singles were released from the LP.

The Beatles were an English rock band formed in Liverpool in 1960. The core lineup of John Lennon, Paul McCartney, George Harrison and Ringo Starr would go on to change the direction of modern music and pop culture. They released 17 studio albums, five live albums, 52 compilation albums, 36 EPs and 63 singles and have sold more than 600 million records worldwide. They have won an Academy Award, seven Grammy Awards, 15 Ivor Novello Awards and a Lifetime Achievement Grammy Award and are members of the Rock and Roll Hall of Fame as a group and individually. In 1965, Queen Elizabeth II appointed each member an MBE. Paul McCartney and Ringo Starr have been knighted. The Beatles were featured in four motion pictures and 10 documentaries. John Lennon was assassinated in 1980 and George Harrison died in 2001. Paul McCartney and Ringo Starr continue to record and tour as solo artists. Paul McCartney will be on his Got Back Tour in the U.S. and Canada this fall and Ringo Starr will be on his Ringo Starr and His All Starr Band Tour in the U.S. in September.