Big changes are coming to the new epicenter of the global LNG market: Texas and Louisiana. On top of the existing 12.5 Bcf/d of LNG export capacity in the two states, another 11+ Bcf/d of additional capacity is planned by 2028. The good news is that the two major supply basins that will feed this LNG demand — the Permian and the Haynesville — will be growing, but unfortunately not quite as fast as LNG exports beyond 2024. And there’s another complication, namely that the two basins are hundreds of miles from the coastal LNG terminals, meaning that we’ll need to see lots of incremental pipeline capacity developed to move gas to the water.

If we break it down further, looking at Texas and Louisiana separately, we see quite different fundamental dynamics. On the Louisiana side, LNG exports are set to rise faster than production in the state, while in Texas, the pace of production growth generally matches the combo of LNG and Mexico exports for a few years, but eventually lags behind as new LNG terminals come online, requiring the state to pull more gas in from Oklahoma or send less to Louisiana. These developments will drive highly dynamic market conditions, with flow shifts that will impact price differentials, the need for new pipeline infrastructure, and the gas sourcing strategies for LNG exporters.

As we explore in today’s RBN blog, understanding all of these changes requires a natural gas flow/capacity model specifically targeted to make sense out of the evolving market dynamics in Texas and Louisiana. We’ve got one, and we call it Arrow.

More on the Arrow Model in a minute. First, we want to drive home the point that the magnitude of the changes coming is enormous. There will be a slew of new LNG export terminals — even if the months-long pause on new gas-export licenses announced by the Biden administration on January 26 drags on. We will see rising gas production in both the Permian and the Haynesville. And there will be more pipeline projects than you can shake a stick at. There are a number of wrinkles that have made the outlook particularly dynamic over the past few months. Consider the following market-impacting examples:

- We’re seeing a resurgence in Eagle Ford gas production, concentrated in the southern and western portions of the play rather than the oilier windows closer to the Houston Ship Channel.

- New LNG flows out of the southernmost tip of Texas will begin when Rio Grande LNG comes online. And Rio Grande might not be the last LNG terminal in that neighborhood either: Just this month, EQT signed a preliminary feedgas-supply contract with Texas LNG, also located near the Texas-Mexico border.

- More LNG export flows to the Texas side of the Sabine River are on the way, with Golden Pass LNG (QatarEnergy, ExxonMobil) ramping up over the course of 2025 (inconvenient for us modelers, months later than the late-2024 startup the market had initially been expecting). And then there’s the Port Arthur LNG (Sempra) export facility coming on in H2 2027.

- Cheniere is expanding its existing Corpus Christi facility with seven midscale modular trains to add to the three large trains currently in operation. The new trains are expected to produce LNG starting in Q4 2024.

- Even more demand is coming in southeastern Louisiana. Plaquemines LNG (Venture Global) took FID (final investment decision) in Q1 2023, and that part of the world is also the nexus of what looks to be significant ammonia investments that will require their own incremental gas supplies.

To understand the dynamics of how these factors and many others will impact flows, capacities and price differentials in the Texas/Louisiana market, you need to model the historical fundamental relationships in the region and then overlay forecasts of supply/demand and the infrastructure projects needed to move gas from production areas to that demand: LNG exports, Mexico exports and new Gulf Coast industrial projects.

Compounding the challenges of modeling these changing gas fundamentals, Texas and Louisiana have the most dense, interconnected, and complicated network of natural gas pipelines anywhere in North America, and for that matter, the world. So to get a handle on these developments and their effects, we need to dissect the region in terms of gas flows and pipeline capacity utilization. The trick is to aggregate the dozens of pipelines into, within, and out of Texas and Louisiana into meaningful flow corridors that access comparable supply sources and deliver those volumes to similarly situated demand regions. And at the same time, we need to factor in the reality that what constitutes a meaningful flow corridor is changing with those new sources of gas supply and demand growth.

FERC Greenlights Two Natural Gas Pipeline Projects

We’ve been at this Texas/Louisiana flow/capacity fundamentals business for many years, developing the original rendition of our model back in 2016. Since then, we’ve used the model to analyze various topics not only in our consulting engagements, but also right here in the RBN blogosphere, including in Born on the Bayou, where we detailed how gas flows into, within, and out of Louisiana, and in Get Ready, where we assessed how new pipeline capacity from the Permian combined with growing LNG exports would affect Houston Ship Channel basis differentials. When the pandemic upended everyone’s gas production growth outlooks in 2020, we posted our Some Beach blog series, which focused on everyone’s favorite elephant in the room — the Permian — to examine how new Permian takeaway capacity would combine with weaker production growth and rising LNG exports to shift flows both within Texas and across the Texas/Louisiana border.

More recently, in Down by the Water, we used the model to explain how rising LNG exports in both Texas and Louisiana would affect Bayou State gas flows and, in Gotta Get Over, we examined the different types of pipeline projects being planned to de-bottleneck Louisiana in advance of increasing Haynesville production and rising LNG export demand.

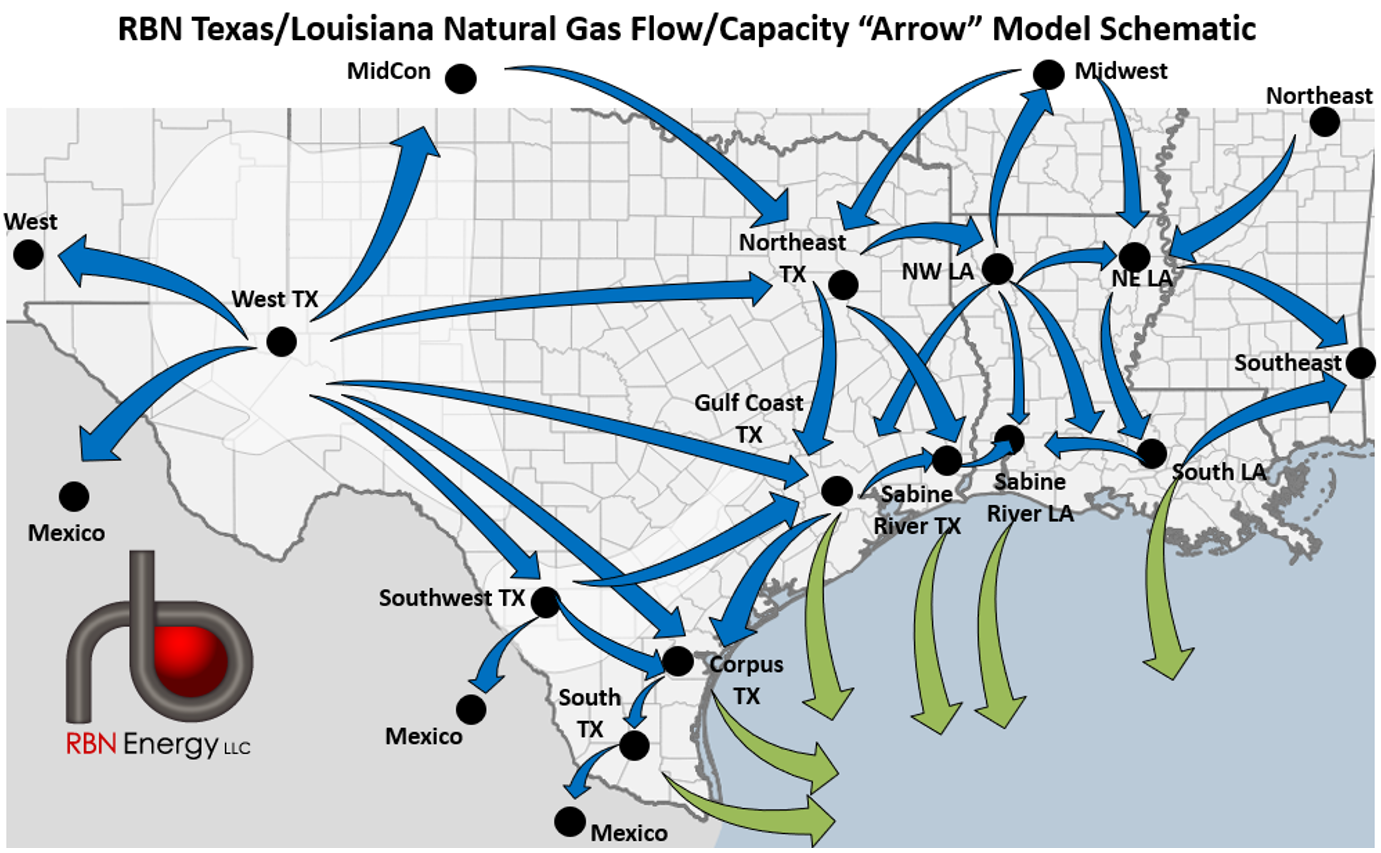

As we said, we call the RBN Texas/Louisiana Natural Gas Flow/Capacity model the “Arrow Model” for short. Figure 1 below provides a schematic of the model — and reveals how it got its name. Lots of arrows. Our approach is to carve the Texas/Louisiana region into pipeline “corridors” that can be used to assess changes in the region’s inflows, outflows and flows within each state via groups of pipes that serve similar markets from comparable supply sources. These pipeline corridors (blue arrows) are aggregations of pipelines connecting 19 market hubs (black dots) that we have specified as relevant to the analysis of the Texas/Louisiana market, some of which are within the two states and others that are outside the region. We also identify the six LNG corridors (green arrows) through which gas exits the region in liquefied form on LNG carriers. The attributes of each arrow include capacity, historical flows, projected flows, constraints, and other factors. The net flows for each arrow move in the direction indicated by the arrow, but they can and do flip around over time when modeled market conditions dictate.

Figure 1. RBN Texas/Louisiana Natural Gas Flow/Capacity “Arrow Model.” Source: RBN

As we will discuss in more detail later, the Arrow Model approach enables us to (1) aggregate gas production, demand and net outflows or inflows for each market hub over time; (2) quantify the degree to which gas is pushed/pulled between and among hubs, again over time; (3) predict gas flows on each corridor (and the need for incremental pipeline capacity); and (4) forecast the basis differentials that underlie and support the aforementioned flows of gas.

The best part is, you don’t need to know how all of our model is wired together mathematically to make sense of the model’s output. It is our job to lay out the assumptions that go into Arrow, extract the output with the right amount of detail where it’s needed, and provide an easily digestible, targeted market outlook. It all boils down to a rigorous examination of flows and capacity utilization across these corridors, then incorporating new pipeline, LNG-export and industrial projects to provide a comprehensive understanding of how flows and price differentials are likely to shift and evolve month by month, season by season and year by year. Importantly, the model’s inputs can be tweaked to account for changing conditions, such as LNG project delays tied to the Biden administration’s recently announced pause on export license approvals.

Now that we have a basic understanding of what the Arrow Model does and how it does it, let’s dig into the fundamentals of what the model reveals about upcoming flow and capacity shifts across Texas and Louisiana, starting with the big picture.

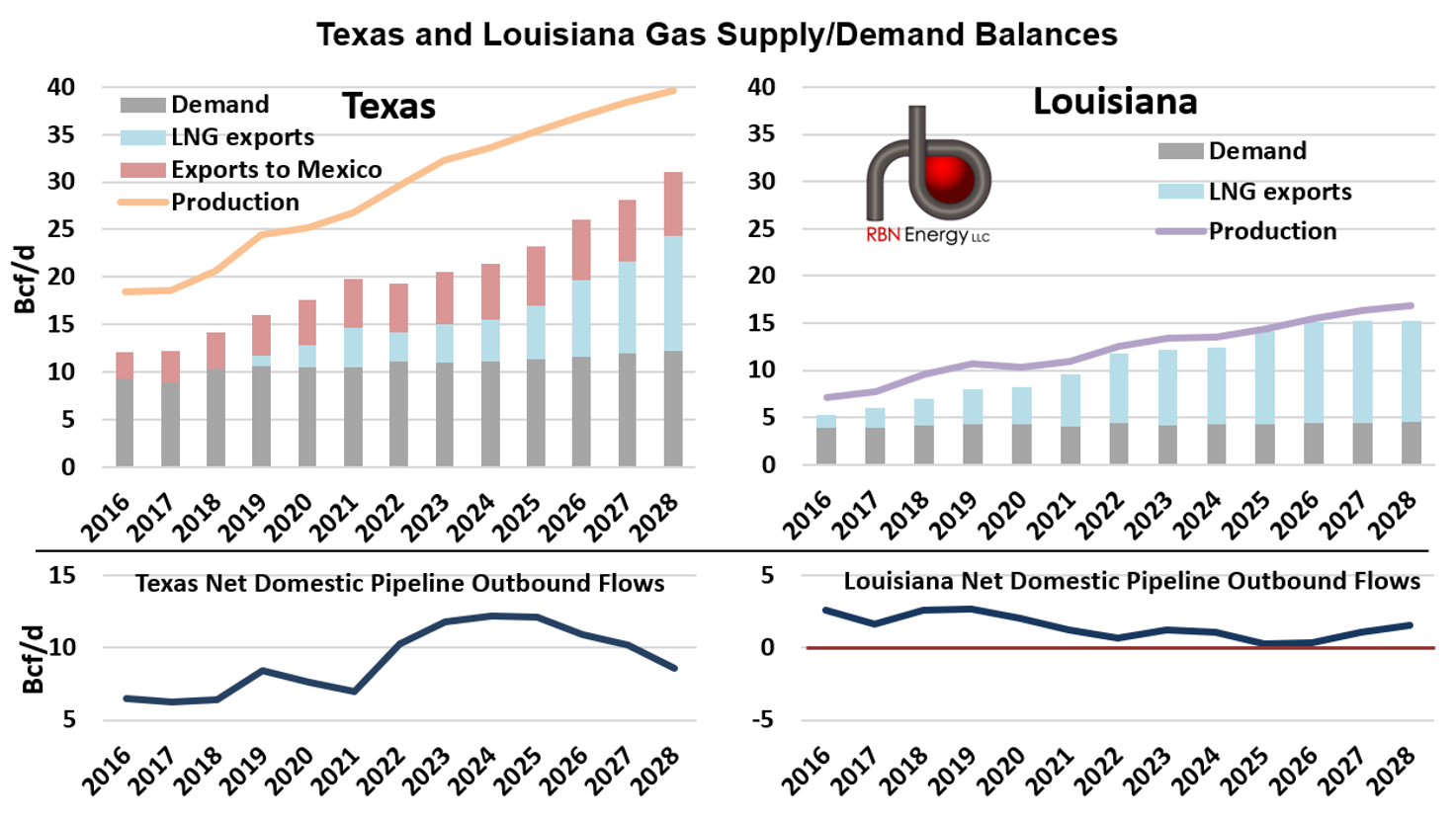

Figure 2 below shows the incremental growth in Permian and Haynesville gas production in our “Mid” forecast scenario compared with Texas/Louisiana LNG exports from 2023 to 2028. LNG exports are ramping up: a total of more than 12 Bcf/d of demand growth over the next five years (green line). That number includes the new LNG terminals coming online, the feedgas/losses that come along with LNG flows, the proposition that some of these export facilities run above capacity, and 2023-24 growth reflecting Freeport downtime last year. At the same time, dry gas production in the Permian (orange bar segments) and the Haynesville (purple bar segments) is growing by about 10 Bcf/d over the same period (5.4 Bcf/d and 4.7 Bcf/d, respectively) — well below the pace of LNG demand growth. The implication is that more gas must move into the region (or less gas must move out) for there to be enough gas to meet Texas/Louisiana LNG demand.

Figure 2. Incremental Permian and Haynesville Gas Production vs. Incremental LNG Exports. Source: RBN

The more you zoom in, the more you learn. For example, the Texas and Louisiana sides of the region are experiencing conflicting fundamental dynamics. In Louisiana, LNG exports (light-blue bar segments in upper-right graph in Figure 3 below) rise slightly faster than production in the state (purple line) for the next few years, and by 2025, net outflows from the state (dark-blue line over the zero mark in lower-right graph) to the surrounding states (Texas, Arkansas, and Mississippi) drop to the zero mark — meaning that, in aggregate, those neighboring states neither receive nor deliver gas to Louisiana. After 2026, though, the state becomes slightly net long gas supply (the dark-blue line climbs back above zero), as no LNG export facilities are expected in 2027-28 and Haynesville production continues growing.

Figure 3. Texas and Louisiana Gas Supply/Demand Balances. Source: RBN

Conversely, in Texas, the pace of production growth (orange line in upper-left graph in Figure 3) roughly matches (and sometimes exceeds) the pace of growth in LNG exports (light-blue bar segments) and pipeline exports to Mexico (pink bar segments) to 2026 — thereby keeping the state’s supply/demand balance (dark-blue line in lower-left graph) steady and sometimes rising. However, in 2027-28, with the startup of the Port Arthur and Rio Grande LNG terminals and steady-as-she-goes Permian production growth, the supply/demand balance trends downward as Texas needs to pull more gas in from Oklahoma, send less to Louisiana or both.

In essence, those big-picture flows are the starting point for our Arrow Model analytics. Over the upcoming installments of this blog series, we’ll examine some key market areas across Texas/Louisiana, explaining which arrows go where, how the arrow flows are changing, and what all those arrows mean for basis differentials. As you can tell, we like this model a lot. We are confident that our aim is true.

We’ll be diving into this model and more in our upcoming NATGAS Master Class on April 10th. This event provides a unique opportunity to gain a comprehensive understanding of these crucial topics and explore their practical applications through insightful presentations, interactive exercises, and discussion. Click here for more information and to register.

About the song

“Alison (My Aim Is True)” was written by Elvis Costello and appears as the fifth song on side one of Elvis Costello’s debut album, My Aim Is True. Costello claimed he wrote the song about a cashier at a grocery store. In what would become a Costello trait, the lyrics present a Raymond Chandleresque/film noir scenario about lost love and sentimental regret. The line, “My aim is true,” would be used as the title for his debut album. Released as a single in May 1977, the song didn’t chart in the U.S. but received plenty of airplay on U.S. album-oriented rock radio. Linda Ronstadt released her version as a single in April 1979 and it went to #30 on the Billboard Hot 100 Singles chart. Personnel on the Costello record were: Elvis Costello (vocals, rhythm guitar), John McFee (lead guitar), John Ciambotti (bass), Sean Hopper (keyboards), and Mickey Shine (drums).

My Aim Is True was recorded in 1976-77 at Pathway Studios in London and produced by Nick Lowe. Pathway was a small, eight-track studio favored by Stiff Records owners Dave Robinson and Jake Riviera. In addition to Costello, The Damned, Squeeze, Madness, and The Police recorded there. Costello was backed up on most of the album by members of the San Francisco band, Clover. While recording the album the band resided at Headley Grange outside of London, a place made infamous as the location for the recording of several Led Zeppelin albums because of its stone walls and unique acoustics. The album was recorded and mixed in a total of 24 hours. Since the time that the record was made, Clover member John McFee joined The Doobie Brothers, Sean Hopper was a member of Huey Lewis and The News, and John Ciambotti became a session bassist and chiropractor in Los Angeles (he died in March 2010). Producer Nick Lowe, a former member of popular British pub rock band Brinsley Schwarz, became a successful solo artist. Released in July 1977, the My Aim Is True LP went to #32 on the Billboard 200 Albums chart and has been certified platinum by the Recording Industry Association of America. Three singles were released from the LP.

Elvis Costello (Declan Patrick MacManus) is an English singer, songwriter, musician, record producer, author, and television host. He started playing professionally in the Liverpool folk rock band Rusty. After moving to London, he formed the pub rock band Flip City. While recording with Flip City at Pathway Studios in London, Costello met Dave Robinson from Stiff Records, who offered him a solo record deal in 1976. He has released 32 studio albums, six live albums, 16 compilation albums, two EPs, and 62 singles. Costello has won two Grammy Awards, two Ivor Novello Awards, an ASCAP Founder Award, and an MTV Video Music Award. He is a member of the Rock and Roll Hall of Fame and the Songwriters Hall of Fame. He continues to record and tour.

Comments

I would love to hear the RBN take on what is going on with the growth of 30s oil in the US. See the recent EIA energy today note. What really is happening and what is driving it? You all are some of the best at puzzles like this. Oh...and he's not heavy, he's my brother.

In reply to DJ special request by g p

Great topic and great song request. We probably ought to revisit the topic but we have talked about it in the past in our Still Crazy blog from back in 2020. Obviously, the world has changed a lot since then (nobody had any idea how COVID was going to shake out) but part of what we said at the time was:

You might be wondering, why would production of superlight crudes and condensates be so stable compared to light and medium grades? There are a couple of reasons. First, the price of these 50.1-degrees-and-up barrels is discounted due to quality considerations — their product yields don’t fit the needs of most Gulf Coast refiners — so producers have backed off drilling in areas that come along with a lot of condensate production like the western Eagle Ford and the Delaware Basin side of the Permian. And second, we think some of the superlight and condensate barrels end up blended off with light- and medium-grade crude, and therefore are misclassified in these statistics.

In reply to Great topic and great song by David Braziel

If you graph it, you see a different phenomenon the last year versus previous several. Yeah, it might be blending, but would that gibe with 914 data? Don't they enter what is produced on the pads? Not how it was mixed by midstreamers? I would look at the Energy Today note from a few days ago...really is kind of curious.