For most of us, matching spending with income is the logical path to financial stability. However, after decades of aggressive investment in search of growth, the “dollars in equals dollars out” method of allocating free cash flow has been an adjustment for many U.S. oil and gas producers. Their post-pandemic concentration on keeping capital spending well below inflows, maintaining healthy leverage ratios and directing excess funds to reward shareholders with dividends and stock buybacks has revitalized the industry and restored investor confidence. But ebbing commodity prices have upped the difficulty of this quarterly zero-sum game. In today’s RBN blog, we will analyze the shifts detected in Q2 2025 cash allocation of the 38 major U.S. E&Ps we cover.

Analyst Insights are unique perspectives provided by RBN analysts about energy markets developments. The Insights may cover a wide range of information, such as industry trends, fundamentals, competitive landscape, or other market rumblings. These Insights are designed to be bite-size but punchy analysis so that readers can stay abreast of the most important market changes.

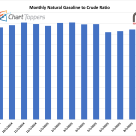

The monthly natural gasoline price for September 2025 stands at 85% of NYMEX crude, reflecting a modest uptick of one percentage point from August’s 84%. However, the ratio remains slightly below year-ago levels, down one point from 86% in September 2024.

If it seems like the push for decarbonization has suddenly picked up the pace lately, Michigan provides proof. Home to the Big 3 automakers and for many the symbolic heart of U.S. manufacturing, its efforts to move away from fossil fuels have long been met with skepticism and resistance. But changing attitudes about climate change and renewable power — and full Democratic control of the state government for the first time in 40 years — have led to a swift about-face in the state’s energy policy. In today’s RBN blog, we examine Michigan’s plans to accelerate its transition away from coal-fired power and the long-term challenges that come with it.

Appalachian natural gas producers got good news earlier this month: Williams announced it was moving forward with the Southeast Supply Enhancement project, a large-scale expansion of southbound capacity out of the Northeast on its Transco Pipeline system. Not only that, but it super-sized the project to 1.4 Bcf/d of capacity — nearly double the 800 MMcf/d it had offered in an open season held this summer. The project is one of several brownfield expansions planned to provide additional supply access in Transco’s premium Zone 5 market area, which runs through Virginia and North Carolina — and the first large-scale takeaway expansion to be announced in the area since the long-delayed Mountain Valley Pipeline (MVP) was cleared for completion following years of regulatory and legal hurdles. In today’s RBN blog, we provide the latest on the Transco Corridor expansions.

U.S. Gulf Coast LPG exports are sky-high, averaging just under 2 MMb/d in October, with nearly two-thirds of those volumes bound for Asia — a straight-shot trip once a Very Large Gas Carrier (VLGC) has passed through the Panama Canal. But an unprecedented dry spell has left the canal’s operators — and LPG shippers — in a real bind. The century-old maritime shortcut, which was expanded just a few years ago to accommodate more and larger vessels, uses massive amounts of fresh water, and to help conserve what’s left in the system’s main reservoir, the Panama Canal Authority (PCA) is ratcheting down how many ships can pass through each day. Worse yet, VLGCs are a low priority compared to other, larger vessels that pay higher tolls. That means that far fewer Asia-bound LPG ships will be using the Panama Canal for who knows how long. Instead, many shippers will need to make far longer, more costly trips through the Suez Canal or around the southern tip of Africa. In today’s RBN blog, we discuss what LPG shippers in particular are up against.

The push to decarbonize frequently focuses on the transportation sector, which is responsible for the largest share of global greenhouse gas (GHG) emissions. That has led to increased blending of ethanol into gasoline and the development of several alternative fuels, most notably renewable diesel (RD) and sustainable aviation fuel (SAF). But as production of those two fuels accelerates, an often-overlooked byproduct of their creation is beginning to attract more attention: renewable naphtha. In today’s RBN blog, we explain the similarities and differences between traditional naphtha and renewable naphtha, look at how renewable naphtha is produced, and show how it can be used to help refiners, petrochemical companies and hydrogen producers meet their sustainability goals and reduce the carbon intensity (CI) of their products.

Wider price discounts for Western Canadian heavy crude oil have been weighing on its oil producers for the past few months. This appears to be the result of a combination of weak refinery demand, rapidly rising oil production and insufficient oil takeaway capacity from Western Canada. A more permanent solution for wider discounts might be to increase pipeline export capacity to ensure that rising oil production has more options to reach markets. In today’s RBN blog, we consider the pending startup of the Trans Mountain Expansion Project (TMX) as a means to do just that.

Much like their upstream counterparts, midstream companies have shifted to fiscal conservatism over the past few years, focusing less on growth and capital investment and more on shareholder returns, acquisitions and debt reduction. But there are significant differences between the strategies of midstream companies set up as traditional corporations, or C-corps, and those established as master limited partnerships, or MLPs. In today’s RBN blog, we continue our short series on midstream company cash flow allocation with an analysis of their reinvestment rates vs. their shareholder payouts.

Crude-oil-focused production growth in the Permian is generating increasing volumes of associated gas that need to be processed and mixed NGLs that need to be piped to Mont Belvieu, fractionated and exported. All that suggests the need for still more infrastructure — processing plants, NGL pipelines, fractionators and export facilities — and Enterprise Products Partners, a top-tier NGL midstreamer, recently laid out a multibillion-dollar plan to help Permian producers keep pace. In today’s RBN blog, we discuss the new set of projects Enterprise has in the works.

Over the past four years, we’ve documented the strategic transformation of upstream oil and gas producers from growth at all costs to the fiscally conservative concentration on accumulating free cash flow to accelerate shareholder returns. Much like their upstream counterparts, midstream corporations and master limited partnerships (MLPs) have shifted to fiscal conservatism, focusing less on growth and capital investment and more on shareholder returns, acquisitions and debt reduction. In today’s RBN blog, we examine the cash flow allocation of a representative baker’s dozen of midstream companies as they compete for investor support.

It’s been a rough few weeks for the offshore wind industry, highlighted by Ørsted’s decision to cancel two high-profile projects in the Northeast: Ocean Wind 1 and Ocean Wind 2. The industry continues to be plagued by a host of problems around inflation, the supply chain and permitting, leading some developers to write-down losses and question whether their projects remain economically viable. But it hasn’t all been bad news, as other projects have been able to move forward and hit major milestones. In today’s RBN blog, we look at the recent cancellations, some key projects that have been approved or are advancing, and what we’ll be watching for over the next several months.

Well, thanks to you all, we reached another important milestone this week: 40,000 subscribers to RBN’s daily blog. We are quite proud of the achievement. That’s a lot of folks taking time out of their busy day to read a couple thousand words about what’s happening with oil, gas, NGLs and renewables — all in the context of a rock & roll song. We couldn’t have done it without you. Today, after posting a total of about 3,000 blogs over nearly 12 years, we pull back the curtain on the RBN blogosphere and discuss how and why it all happens — and how you help shape what we blog about.

Over the past couple of years, a growing number of natural gas producers — from global integrateds like ExxonMobil, Chevron and BP to E&Ps large, medium and small — have contracted with entities like MiQ and Project Canary to scrutinize their upstream operations and score their relative success in minimizing methane emissions. By some estimates, as much as one-third of U.S. gas production is already “certified” or “differentiated,” and with growing interest in “low-emissions” gas among domestic and international buyers the trend seems likely to accelerate. In today’s RBN blog, we continue our look at certified/differentiated gas with a review of the gas producers leading the way.

The price discount for Western Canada’s benchmark heavy crude oil has seen yet another widening in the past few months. Increased pipeline access to the U.S. was believed to be the key to solving this problem in the long term, but more recent fundamental developments surrounding pipeline egress, refinery demand and increasing heavy oil supplies demonstrate that larger discounts can — and do — still happen. This problem could persist for several more months until a better balance is achieved in downstream markets. In today’s RBN blog, we discuss the latest drivers of the wider price discounts for Western Canada’s heavy oil.

Six months ago, the U.S. West Coast natural gas market looked like it was in dire straits. A harsh winter had depleted stocks to the lowest level in over a decade and it seemed like the region would be hard-pressed to refill storage to a reasonable level, given limited and constrained pipeline options to flow incremental gas west. Instead, a combination of mild weather and operational changes eased demand and pipeline constraints, and Pacific Region storage staged a remarkable comeback this summer. In today’s RBN blog, we delve into how the region escaped a worst-case scenario heading into the heating season.

Phillips 66 is probably best known for its fleet of complex refineries, but the Houston-based company also is involved in marketing, chemicals and midstream services. In fact, P66 is one of only a handful of midstreamers offering the full range of “well-to-market” or “well-to-water” NGL services — everything from associated-gas gathering systems and gas processing to NGL pipelines, storage, fractionators and export facilities. And P66’s standing among NGL midstream providers has only been enhanced by the recent doubling of its ownership interest in DCP Midstream. In today’s RBN blog, we continue our series on major NGL networks with a look at P66’s NGL-related assets, most of which run from the Rockies, West Texas and South Texas to the NGL hubs in Mont Belvieu and Old Ocean, TX.

LNG export projects looking to take a positive final investment decision (FID) need to sell a high proportion of their nameplate capacity under long-term contracts to ensure sufficient cash flows to underpin the project and obtain financing. U.S.-based projects (new and expansions) totaling more than 350 million tons per annum (MMtpa, 48.3 Bcf/) — against a current global market of 400 MMtpa (52.9 Bcf/d) — are vying for creditworthy offtakers from multiple markets in their pre-FID deliberations. The sense of urgency among project sponsors has been boosted by the Russia/Ukraine war and a potentially resurgent Chinese economy, both of which should promise a bright future for new projects. Plenty of those have reached FID in the last couple of years, but what is holding others back from taking the same step? In today’s RBN blog, we’ll look at some of the factors impacting those decisions and the long-term implications that flow from them.