Over the past four years, we’ve documented the strategic transformation of upstream oil and gas producers from growth at all costs to the fiscally conservative concentration on accumulating free cash flow to accelerate shareholder returns. Much like their upstream counterparts, midstream corporations and master limited partnerships (MLPs) have shifted to fiscal conservatism, focusing less on growth and capital investment and more on shareholder returns, acquisitions and debt reduction. In today’s RBN blog, we examine the cash flow allocation of a representative baker’s dozen of midstream companies as they compete for investor support.

The RBN Crude Oil Analytic Suite gives you access to four weekly reports covering crude oil markets, including: Crude Billboard, Crude Permian, Crude TradeView, and Crude Voyager.

Taking advantage of the more stable, fee-based revenues from energy infrastructure such as pipelines, gas processing plants, storage facilities and fractionators, midstream entities historically have focused on generating substantial returns to shareholders. In the early 1980s, midstream MLPs were created as tax-efficient entities that aimed to distribute most of their cash flow to their general and limited partners. The primary benefit of MLPs was single taxation, which meant that taxes were not paid on the entity level but instead were passed through to the limited partners’ personal tax returns. A portion of those distributions qualified as return of capital, which meant the taxes on that portion could be deferred until the units were sold. In contrast, a corporation’s income is subject to double taxation, once at the corporate level and then again on dividends at the shareholder level.

However, in the early years of the Shale Era midstream companies transitioned their strategies toward growth as they developed U.S. gathering systems, “replumbed” long-haul pipelines and made other investments to accommodate the needs of new unconventional oil and gas plays. They largely funded this investment by issuing new units, but the oil price crash in 2014-15 crimped access to capital markets. MLPs were particularly impacted because up to half of their cash flows were syphoned off to general partners as incentive distribution rights (IDRs), which award a general partner a greater share of the MLP’s profits as certain goals are met. Although the general partnership normally holds only a 2% limited partnership interest, IDRs can range to up to 50% of the total distributions, sharply reducing cash available for investment and limited partner distributions. In addition, because regulations severely limit retirement accounts and pension funds from purchasing their limited partnership units, the universe of potential investors is sharply reduced. As a result, many companies slashed or froze distributions. Then the Tax Reform Act of 2017 cut the corporate tax rate, reducing the impact of double taxation. As a result, several major midstream entities restructured as traditional C-corps and many remaining MLPs restricted or eliminated IDRs.

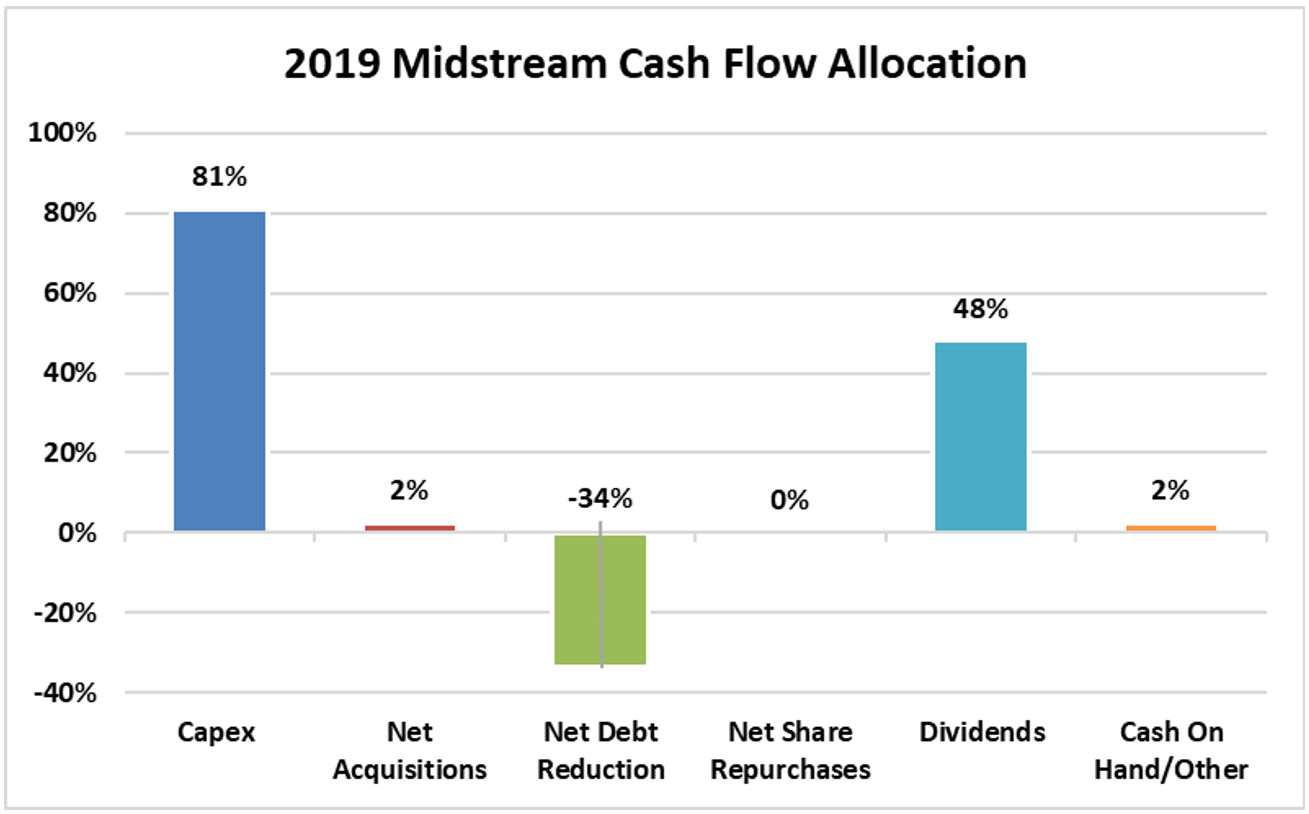

Figure 1. 2019 Midstream Company Cash Flow Allocation. Source: Oil & Gas Financial Analytics, LLC

About the song

“Let It Grow” is written by Eric Clapton and appears as the third song on side two of Clapton’s second solo album, 461 Ocean Boulevard. The song’s lyrics are a reflective treatise on love and redemption. After a three-year hiatus from the music industry, and overcoming heroin addiction, there is a good chance that Clapton wrote this song while living in Tulsa around 1973, enjoying the local music scene under the auspices of good friend Leon Russell, who had a home and studio in Tulsa at the time. Three-fifths of the band Clapton put together for 461 Ocean Boulevard came from Tulsa: longtime Russell and Clapton bassist Carl Radle, and organist Dick Sims and drummer Jamie Oldaker, both of whom came from the popular Tulsa band, Tulsa County. Personnel on the record were: Eric Clapton (lead vocals, guitar, slide guitar), George Terry (guitar, backing vocals), Dick Sims (organ), Albhy Galuten (piano), Carl Radle (bass), Jamie Oldaker (drums), and Yvonne Elliman (backing vocals).

461 Ocean Boulevard was recorded in the spring of 1974 at Criteria in Miami, with Tom Dowd producing. The album’s title refers to the address Clapton and his band were living at in Golden Beach, FL, while they were recording the album. Clapton used his black Stratocaster —a Gibson ES 335 nicknamed “Blackie” — for slide work, and various Martin acoustic guitars in making the LP. Released in July 1974, the album went to #1 on the Billboard 200 Albums chart and has been certified platinum by the Recording Industry Association of America. Two singles were released from the LP.

Eric Clapton is a British rock and blues guitarist, singer, and songwriter. He was a member of The Yardbirds, John Mayall’s Bluesbreakers, Cream, Blind Faith, Delaney & Bonnie’s band, Derek and the Dominoes, and has an extensive solo career that began in 1974. As a solo artist, Clapton has released 21 studio albums, 15 live albums, 21 compilation albums, seven soundtrack albums, and 81 singles. He has an OBE and CBE from Great Britain and a Grammy Lifetime Achievement Award, and is a Commander of the Ordre des Arts et des Lettres of France. He was inducted into the Rock and Roll Hall of Fame three times: as a member of The Yardbirds and of Cream, and as a solo artist. He continues to record, tour, and put on the annual Crossroads Guitar Festival. His next tour dates are scheduled for May 2024 with performances in the UK and Ireland.