The price discount for Western Canada’s benchmark heavy crude oil has seen yet another widening in the past few months. Increased pipeline access to the U.S. was believed to be the key to solving this problem in the long term, but more recent fundamental developments surrounding pipeline egress, refinery demand and increasing heavy oil supplies demonstrate that larger discounts can — and do — still happen. This problem could persist for several more months until a better balance is achieved in downstream markets. In today’s RBN blog, we discuss the latest drivers of the wider price discounts for Western Canada’s heavy oil.

The twists and turns in the pricing saga of Western Canada’s heavy crude oil marker, Western Canadian Select (WCS), are seemingly endless. Used as the benchmark for heavy crude pricing, its value at the price hub of Hardisty, AB, is determined as a discount to the price of light crude oil benchmark WTI at Cushing, OK. The magnitude of that discount is a very important determinant in the price netback realized by heavy oil producers, which account for about 80% of all the crude produced in Western Canada. With that kind of weighting, the price of WCS and its discount is a very big deal.

The Crude Oil Billboard keeps readers at the forefront of the U.S. crude oil market by offering access to data and information moments after its release. Say goodbye to PDF reports that come out after the market has already moved on.

The fact that heavy, higher-sulfur oil is priced at a discount to light sweet crude is not surprising, especially for WCS and other related heavy oil streams produced in Western Canada. Heavy oil requires more processing at refineries to be turned into useful end-use products such as gasoline and diesel, meaning higher costs; it has to be transported very long distances to reach refineries in Eastern Canada, the Midwest, and the Gulf Coast, meaning higher costs; and there can be choke points in the transportation network of pipelines where too much crude oil supply is competing for too little pipeline space. In that situation, the discounting can become more extreme at certain locations as producers engage in barrel-on-barrel competition by offering a wider and wider discount (i.e., lower absolute price) to ensure their supply gets into the pipeline to downstream refiners ahead of a competitor’s supply. When this combination of upstream supply, downstream refinery demand and pipeline networks is well synchronized, the price discount for WCS should more or less reflect the combined cost of transportation and refinery processing, with the bulk of that coming from the cost of pipeline transportation.

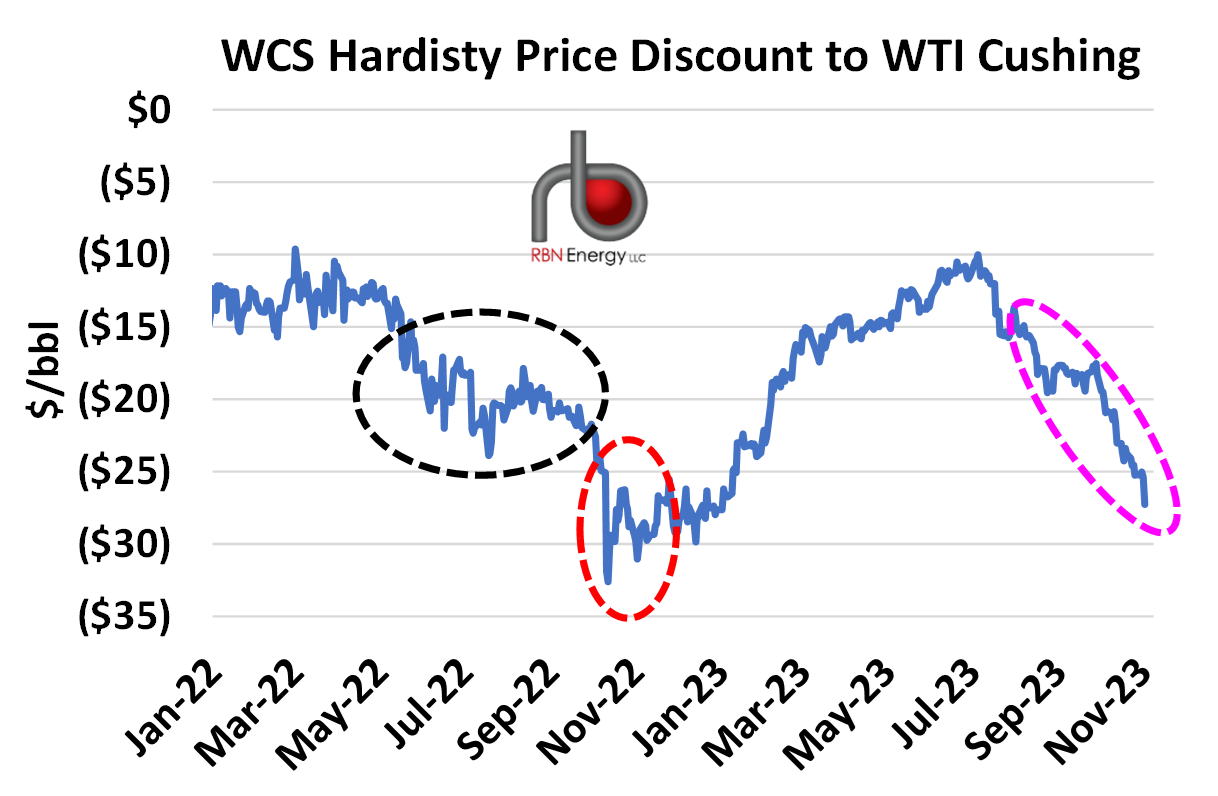

As you might expect, the motivation for today’s blog — and song title — is that in the past couple of months the discounting of WCS seems to harken back to past same ol’ situation(s) of greater price discounting, recently reaching levels as low as US$27/bbl under WTI (pink dashed oval in Figure 1) at the end of October and well below the more market-optimal discount that lies in the $10-$15/bbl range. The rough math means that Western Canada’s heavy oil producers are getting $12/bbl less for their heavy crude oil than they were just a few months ago, and at a time when benchmark light crude oil prices like WTI have remained elevated in a global market shaped by producer-driven supply constraints and geopolitical upheavals.

Figure 1. WCS Discount to WTI. Source: Bloomberg

About the song

“Same Ol’ Situation (S.O.S.)” was written by Nikki Six, Mick Mars, Vince Neil and Tommy Lee. It appears as the seventh song on Mötley Crüe’s fifth studio album, Dr. Feelgood. Released as the album’s fifth single in July 1990, it went to #34 on the Billboard Mainstream Rock and #78 on the Hot 100 Singles charts. Personnel on the record were: Vince Neal (vocals, rhythm guitar), Mick Mars (lead guitar), Nikki Sixx (bass), and Tommy Lee (drums).

Dr. Feelgood was recorded in 1988-89 at Little Mountain Sound Studios in Vancouver with Bob Rock producing. It was the first album that Mötley Crüe recorded after their quest for sobriety, their first and only album to go to #1 in the charts, and the band’s last album with Vince Neil as their singer until their 1997 album, Generation Swine. Producer Bob Rock found working with the band so disruptive that to minimize conflict and allow the album to be recorded, he had each band member record their parts separately. Released in August 1989, the album went to #1 on the Billboard 200 Albums chart and has been certified 6x platinum by the Recording Industry Association of America. Five singles were released from the LP.

Mötley Crüe is an American heavy metal band formed in Hollywood in 1981. The lineup of Vince Neil, Nikki Sixx, Mick Mars and Tommy Lee is the most popular version of the group. Nine members have passed through the band over the years, with Nikki Sixx being the only constant member. The band has sold more than 100 million records worldwide. They have released nine studio albums, three live albums, eight compilation albums, three EPs, and 30 singles. They have won one American Music Award and have a star on the Hollywood Walk of Fame. In October 2022, Mick Mars announced his retirement from touring with the band, with guitarist John 5 replacing him. The band continues to record and tour and are currently on their world tour in Japan and Australia.