U.S. interstates are populated with electronic displays that update drivers in real-time on traffic conditions, road closures, weather alerts and other important events. If there was a sign for executives steering our nation’s oil and gas producers, it would likely read “Poor Visibility, Slow Down Ahead.” After a short-lived price rally in Q1 2025, the industry faced lower commodity realizations and macroeconomic headwinds in Q2 2025, which spooked investors and hardened a cautious investment approach. In today’s RBN blog, we analyze the latest results of the 39 major U.S. E&P companies we cover and look at what’s ahead.

Analyst Insights are unique perspectives provided by RBN analysts about energy markets developments. The Insights may cover a wide range of information, such as industry trends, fundamentals, competitive landscape, or other market rumblings. These Insights are designed to be bite-size but punchy analysis so that readers can stay abreast of the most important market changes.

ExxonMobil announced on Tuesday, August 26, 2025, that it has reached Final Investment Decision (FID) on a large-scale reconfiguration project at its Baytown, Texas Refinery and Petrochemical Complex.

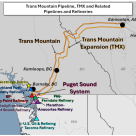

The Trans Mountain Pipeline Expansion (TMX) has been running “spectacularly well since startup” and plans are being considered to boost the pipeline’s capacity, Trans Mountain Chief Financial Officer Todd Stack said during a fireside chat Wednesday at RBN’s School of Energy Canada in Calgary.

U.S. crude oil exports from Gulf Coast ports are soaring — in January they averaged well over 2 MMb/d — and when you’re moving large volumes long distances by water, there’s no vessel as efficient as a Very Large Crude Carrier (VLCC). A number of midstream companies are planning costly offshore terminals that could fully load 2-MMbbl VLCCs, but jobs like that take years, and Moda Midstream is in no mood to wait. Since it acquired Occidental Petroleum’s (Oxy) Ingleside marine terminal near Corpus Christi last September, Moda has been adding new tankage and loading equipment to enable it to load up to 1.25 MMbbl onto a VLCC within 24 hours from arrival to departure, then send the supertanker out to the deep waters of the Gulf for a quick top-off via reverse lightering. Upon completion of further expansion programs, the terminal’s loading capabilities will reach a combined 160 thousand barrels per hour (Mb/hour) among its three berths. Today, we discuss recent and near-term enhancements at Texas’s newest VLCC loading facility.

Imagine a crude oil hub with all this: a central location near the Gulf Coast; pipeline, waterborne and rail access to a wide range of imported and domestic crude; tens of millions of barrels of storage capacity; direct connections by pipe to nearly a dozen major refineries; and the ability to load “neat” or blended barrels of oil onto Aframax-class vessels for export. You’ve conjured up the hub in Louisiana’s St. James Parish, which is fast-becoming an even more significant market player, with even broader access to U.S. and Canadian crude supplies and, very likely, direct outbound links to one or more export terminals capable of fully loading VLCCs. Today, we continue our series on St. James with a look at its storage assets and at the pipes that flow into and out of the hub.

The market is used to crude oil spreads in the Permian Basin being volatile. Fast-paced production growth, the addition of new takeaway pipelines — and the rapid filling of those new pipes — have all impacted in-basin pricing, and we’ve seen differentials from the Permian to its downstream markets — Cushing, OK, and the Gulf Coast — widen and narrow as supply and demand fundamentals have changed. But recently, things have gotten a lot wilder. In September 2018, the Midland discount to WTI at Cushing blew out to almost $18/bbl, then narrowed to less than $6/bbl only three weeks later, thanks largely to the start-up of Plains All American’s much-ballyhooed, 350-Mb/d Sunrise Expansion. As Sunrise started to fill up, price differentials initially widened for a brief period of time. But, as we kicked off 2019, the Midland-Cushing spread quickly shrank further and then flipped, with Midland last Friday (January 25) trading at a $1/bbl premium to Cushing crude. You might wonder, how the heck did that happen? In today’s blog, we discuss how things play out when a supply glut evaporates and traders are suddenly caught in a tight market.

When crude oil prices crashed in the second half of 2014 and 2015, producers survived by becoming leaner and more efficient. That transition included drastic reductions in the rates paid to services companies while wringing ever more oil and gas out of each well and, in the process, permanently altering the economics of drilling and completion. This year, producers are again facing a lower-price environment; since early October (2018), crude prices have dropped more than 30%. In the current, more conservative investment environment, can producers do it again? Can additional value be squeezed out with bigger well pads and longer laterals? Today, we continue a series exploring the benefits and risks of these highly concentrated and highly complicated operations.

Earlier this decade, East Coast refineries found it cost-effective to ramp down their crude imports and turn to the price-advantaged U.S. shale oil they could rail in from the pipeline-constrained Bakken or send up by tanker from the crude-saturated Gulf Coast. Things changed, though. New southbound crude pipelines out of the Bakken came online, the ban on most crude exports was lifted — providing a new outlet for Texas crude production — and the economic rationale for railing or shipping in domestic crude to PADD 1 refineries withered. Now, things have changed again. Most important perhaps, is that the price spread between WTI and Brent has widened, and once more it can make financial sense for these refineries to revert to crude-by-rail out of the Bakken and to shipping in crude on Jones Act tankers from Corpus Christi and other Gulf Coast ports. Today, we discuss these recent trends, what’s driving them, and how long they might last.

Record runs allowed U.S. refiners to continue a multiyear streak of strong margins in 2018 despite higher crude prices during the first three quarters and a weaker fourth quarter after product prices tanked along with crude in October. While rising crude prices threatened refinery margins, a high Brent premium over domestic benchmark West Texas Intermediate (WTI) kept feedstock prices for U.S. refiners lower than their international rivals. The availability of discounted Canadian crude also helped produce stellar returns for Midwest, Rockies and Gulf Coast refiners that are configured to process heavy crude. Product prices only weakened in the fourth quarter when gasoline inventories began to rise. Today, we highlight major trends in the U.S. refining sector during 2018 and look forward to 2019.

Throughout the middle and latter parts of the 2010s, crude oil production growth in major U.S. basins and in Western Canada — not to mention the end to the ban on most U.S. crude exports in December 2015 — has caused noteworthy shifts in crude flow patterns, stressed existing pipeline infrastructure, and highlighted the importance of crude storage and distribution hubs. A common theme through all this has been that more and more crude needs to find its way to the Gulf Coast, with its bounty of refineries and export docks. To that end, lately, there’s been a slew of new pipeline and export-terminal projects announced that are tied to the St. James crude trading hub, which is located in Louisiana, about 60 miles up the Mississippi River from New Orleans. Today, we begin a series on St. James and why it’s becoming an even bigger player in crude markets.

The possibility of reversing the flow on Capline — the U.S.’s largest northbound crude oil pipeline — has been discussed for a number of years now. Finally, it may be on the horizon. The three owners of Louisiana-to-Illinois pipeline announced last week that this month they plan to initiate a binding open season for a reversed Capline system that would enable southbound flows starting in the third quarter of 2020 — only a year and a half from now. And, as we discuss in today’s blog, reversing Capline’s direction could open up new crude-slate possibilities for Louisiana refineries and boost crude exports out of the Bayou State.

LPG exports out of Gulf Coast marine terminals averaged 1 MMb/d in 2018, a gain of 12% from 2017 and 35% from 2016. And, with U.S. NGL production rising steadily, 2019 is looking to be another banner year for LPG shipments to overseas buyers. The increasing volume of propane and normal butane — the NGL purity products generally referenced as LPG — is filling up the existing export capacity of the Gulf Coast’s six LPG terminals and spurring the development of a number of expansion projects. Today, we continue our blog series on propane and butane export facilities along the Gulf, West and East coasts, and what’s driving the build-out of these assets.

In 2018, a handful of midstream companies started racing to develop deepwater export terminals along the Gulf Coast that can fully load Very Large Crude Carriers (VLCCs) with 2 MMbbl of crude oil from the Permian and other plays. While some of those companies are moving toward final investment decisions (FIDs) that would bring their plans to fruition in the early 2020s, terminal operators with existing VLCC-capable assets — both onshore and offshore — turned up the volume in a major way in December. Today, we outline the strides made in recent days by the export programs of the Louisiana Offshore Oil Port (LOOP), Seaway Texas City and Moda Midstream.

The Cushing, OK, storage and trading hub plays critically important roles in both the physical and financial sides of the crude oil market. Located at a central point for receiving crude from a wide range of major production areas — Western Canada, the Bakken, the Rockies, SCOOP/STACK and the Permian among them — the hub also has numerous pipeline connections to Gulf Coast refineries and export docks, and to a large number of inland refineries. And, with Cushing’s 94 MMbbl of storage capacity and status as the delivery point for NYMEX futures contracts for West Texas Intermediate, the hub’s inventory levels and the WTI-at-Cushing price are closely watched market barometers. But like a lot of other U.S. energy infrastructure in the Shale Era, Cushing’s place in the energy world has been in flux. Most importantly, Permian production has been surging, the ban on U.S. oil exports is a fading memory, and the Gulf Coast — not Cushing — is where most U.S. crude production wants to go. Today, we discuss Cushing’s changing role and highlights from RBN’s new Drill Down Report on the U.S.’s most important crude hub.

There’s a reason why more than half a dozen midstream companies and joint ventures are clamoring to build deepwater loading terminals on the Gulf of Mexico: because it’s a major pain to load Very Large Crude Carriers (VLCCs) any other way. These days, the standard operating procedure for loading the vast majority of VLCCs along the Gulf Coast involves a complex, time-consuming and costly process of ship-to-ship transfers called reverse-lightering, in which smaller tankers ferry out and transfer crude to VLCCs in specified lightering areas off the coast. Today, we ponder the current dynamics for U.S. crude exports via VLCC.

For months, the crude oil market had Canada figured out. Production was growing, bit by bit. Pipelines were maxed out. Railcars were hard to come by but were providing some incremental takeaway capacity. Midwest refineries, a big destination for Canadian crude, went in and out of turnaround season, moving prices as they ramped up runs. Overall, the supply and demand math was straightforward also, tilted towards excess production. Canadian crude prices were going to continue to be heavily discounted for the next year or two, until one of the new pipeline systems being planned was approved and completed. Western Canadian Select (WCS) — a heavy crude blend and regional benchmark — was averaging at a discount to West Texas Intermediate (WTI) near $40/bbl in November, dragging down Syncrude prices with it. As the market was settling in for a long, cold winter in Canada, a bombshell dropped: Alberta’s premier announced on December 2 (2018) that regulators would institute a mandatory production cut, taking 325 Mb/d of production offline, and that the government would invest in new crude-by-rail tankcars. That announcement has had a massive impact on prices, with WCS’s differential narrowing to $18.50/bbl most recently. In today’s blog, we look at several catalysts for the recent swing in Canadian prices, and how the recent governmental intervention will impact differentials.

This summer and fall, more than a half dozen companies and midstream joint ventures have announced plans for new deepwater export terminals along the Gulf Coast that — if all built — would have the capacity to load and send out more than 10 MMb/d, which is notable because the U.S. Lower 48 currently produces 11.2 MMb/d. Most of these projects won’t get built, of course — export volumes may well continue rising, and the economics of fully loading VLCCs at deepwater ports are compelling, but even the most optimistic forecasts suggest that only one or two of these new terminals will be needed through the early 2020s. So, there’s a fierce competition on among developers to advance their VLCC-ready export projects to Final Investment Decisions (FIDs) first. Today, we discuss highlights from our new Drill Down Report on deepwater crude export terminals as well as the export growth and tanker-loading economics that are driving the project-development frenzy.

During the summer of 2018, crude oil inventories at the trading hub in Cushing, OK, dropped to extreme lows. With estimated tank bottoms around 14.6 MMbbl, Cushing stockpiles hit 21.8 MMbbl for the week of August 3. Traders’ alarm bells were ringing, and upstream and downstream observers were wondering if low storage levels were going to cause significant operational issues. But just when it seemed tanks were nearing catastrophic lows, inventories reversed course and started to climb. Since August, crude stocks have increased by 13.6 MMbbl, or nearly 60%, and there is now talk of potentially too much crude en route to Cushing, maxing out capacity there. There are many contributing factors to this most recent inventory swing, with increased domestic production and the tail end of refinery turnaround season being two of the bigger fundamental drivers. But the main catalyst has been the shift from a backwardated forward curve to a contango forward curve in the WTI futures market. Today, we continue our Cushing series with a snapshot of recent contango markets and the impact those prices have had on stockpiles at the central Oklahoma hub.