Natural gas liquids production in the Utica and “wet” Marcellus has taken off like a rocket, and all that ethane, propane, butane and natural gasoline needs to be either moved out of the region or consumed there. That presents a real operational challenge to midstream companies, mostly because the Upper Ohio River Valley offers very little of the NGL storage capacity that Mont Belvieu—the center of the NGL universe—has in spades. Storage is the mechanism that helps balance out supply and demand on any given day. How can the nation’s fastest-growing NGL production play function without the luxury of significant NGL storage? Today, we continue our look at infrastructure development in the region.

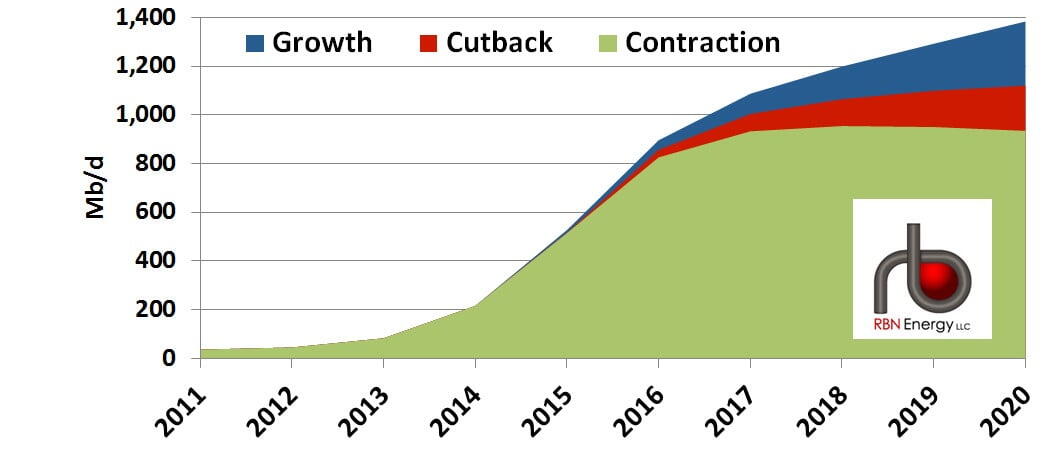

In just a few days (April 6), the Pittsburgh Pirates and the Cincinnati Reds will open their 2015 seasons at the Reds’ Great American Ball Park, each hoping this year will be better than 2014. (The Pirates showed some promise and garnered a National League wild card spot, but lost their playoff game to the San Francisco Giants; the Reds finished the season with a 76-86 record for fourth place in the NL Central Division.) One thing the region between the two cities can count on, though, is a strong energy-driven economy, with continued growth in natural gas and NGL production. Under each of RBN Energy’s three crude oil price scenarios—Growth, Cutback and Curtailment (see I’ll Take You There—Continued NGL Infrastructure Growth Expected in Permian and Eagle Ford Basins for an explanation)— Utica/wet Marcellus NGL production could double if all the ethane available were recovered, and then continue growing in subsequent years depending on your level of optimism about crude prices . Figure#1 shows RBN’s forecast for Northeast NGL production potential, which includes all ethane whether recovered or rejected.

Figure #1 – Northeast NGL Production Potential; Source: RBN Energy

The strong NGL production growth the region experienced in 2014—and expects again this year —is the result of two things: 1) natural gas producers’ new focus on wet-gas plays that provide them the uplift of NGL sales and revenue, and 2) a fast-paced NGL infrastructure build-out by midstream companies like MarkWest Energy Partners, Utica East Ohio Midstream, Blue Racer Midstream and Williams. As we said in Episode 1 of this series, just five years ago there was only 600 MMcf/d of natural gas processing capacity in the entire northeast region, and most of that capacity was scattered widely, with each facility operating pretty much on a stand-alone basis. Since then, however, gas production in the overall Utica/Marcellus region has increased from 2 Bcf/d to nearly 20 Bcf/d, and the fastest growth has been coming from the wet Marcellus in southwestern Pennsylvania and northern West Virginia and in the Utica in eastern Ohio. In Episode 2 we described the Utica/wet Marcellus region in more detail, and in Episode 3 we discussed the eight major pipelines that move natural gas through and out of the region (and unveiled our Pipeline GIS asset mapping function). Then, last time in Episode 4, we described the gas processing assets of MarkWest--by far the biggest midstream player in the Utica/wet Marcellus, with 4.1 Bcf/d of existing gas processing capacity and plans to add another 2.4 Bcf/d by the end of 2016. We mentioned at the time that many of MarkWest’s seven gas processing complexes in the region either have on-site de-ethanizers and/or C3+ fractionators or will have them soon.

Today, we describe those assets, which allow MarkWest to separate out ethane and the other NGLs. First, a quick refresher course on terminology. As we said in our Talkin’ ‘Bout My F-F-Fractionation series, de-ethanizers separate ethane, or C2, the lightest of the five NGLs and the volume-dominant NGL in almost all wellhead gas streams. C3+ units, in turn, separate the other four NGLs--propane (C3), normal butane (NC4), isobutane (IC4) and natural gasoline (C5+)--but not ethane. C2+ facilities, which are most common in Mont Belvieu, remove everything from C2 (ethane) through C5+ and, since they fractionate or separate all NGLs, they are simply called fractionators. We noted in our fractionation series that before the shale revolution, production of natural gas in what is now the Utica/Marcellus was limited to conventional wells that produced (and still produce) only modest amounts of gas with only small quantities of NGLs. That meant the facilities to separate NGLs only needed to be modest in size. Furthermore, with no demand for ethane in that part of the country (all ethane demand is for petrochemicals – steam crackers, and today there are no steam crackers in the Marcellus/Utica vicinity), there was no need for ethane removal, so the facilities that got built were C3+ units that left whatever ethane (C2) there was in the residue gas stream to be sold as natural gas. Now, with production in the wet shale plays in the region taking off—and with Utica/wet Marcellus gas laden with significant percentages of potentially marketable ethane—a key focus is on building de-ethanizers and C3+ facilities that will help optimize NGL sales and revenue.

Now, let’s run through what MarkWest’s got and what it’s planning on the de-ethanizer and C3+ front. Figure #2 shows existing facilities (in color-coded, multi-sized circles*); later in this series we’ll provide a map that also shows what MarkWest and others are planning. (In our next episode, we’ll get to MarkWest’s NGL pipelines and describe how all the separate and distinct pieces of its Utica/wet Marcellus infrastructure are designed to operate as an integrated whole—and to mitigate the operational risks associated with extracting and consuming NGLs in a region that has next-to-no NGL storage capacity.)

[*Pipeline GIS functionality note: Showing gas processing plants, de-ethanizers and C3+ fractionators on the same map can be confusing, since many of these facilities are at the same physical locations. We solved that problem in Pipeline GIS by superimposing different sized circle icons for each type of facility, where gas plants (in blue), sit atop C3+ fractionators (in orange), which in turn sit atop de-ethanizers (in green). That way when there is only one type of facility at a given location it is easy to spot what kind of facility it is. And it is equally easy to identify where multiple facilities are at the same site.

** In Pipeline GIS you can click different layers off and on, so in addition to the gas processing plants, fractionators and de-ethanizers shown in the static map below, when you click through to Pipeline GIS you can see which natural gas pipelines connect to which plants, as we described in Episode 4.]

About the song

“Join Together” was written by Pete Townshend. The song was originally intended to be a part of The Who’s Lifehouse project, an unfinished science fiction rock opera that Pete Townshend was writing as a follow-up to Tommy. Recorded at Olympic Studios in London in May 1972, “Join Together” was released as a single in June 1972. Produced by The Who with Glyn Johns, it went to #17 on the Billboard Hot 100 Singles chart. The song has been included in several Who compilation albums, beginning with the Hooligans double hits album released in September 1981. Personnel on the record were: Roger Daltry (lead vocals, harmonica), Pete Townshend (guitar, synthesizer, Jew's harp, backing vocals), John Entwistle (bass, backing vocals), and Keith Moon (drums).

Hooligans is a double compilation record of hits from The Who running from 1964 to 1978. Released in September 1981, the LP went to #52 on the Billboard 200 Albums chart and has been certified Gold by the Recording Industry Association of America.

The Who are an English rock band formed in London in 1964. Its core lineup was Roger Daltry on lead vocals, Pete Townshend on guitar, John Entwistle on bass, and Keith Moon on drums. They are considered by many to be one of the most influential rock bands of the 20th century. They have released 12 studio albums, 16 live albums, four soundtrack albums, 27 compilation albums, four EPs and 58 singles and have sold over 100 million records worldwide. The Who are members of the Rock and Roll Hall of Fame and UK Music Hall of Fame, and are the recipients of a Lifetime Achievement Award from the Grammy Foundation. Roger Daltry and Pete Townshend received Kennedy Center Honors as members of The Who in 2008. Daltry and Townshend have both released solo albums over the years, and both continue to record and tour as The Who. The Who are currently on the road with The Who Hits Back! tour in the UK.