Recent rumors coming out of Washington DC suggest that changes to US regulations that severely limit exports of US crudes are alternatively imminent or being discussed with a view to repeal. Many US producers have argued that the export ban should simply be removed in order to allow the free flow of crude oil across borders. Today we ponder the impact of an end to the crude export ban.

Crude oil exports from the United States are heavily restricted by Department of Commerce regulations introduced in the 1970’s that are administered by the Bureau of Industry and Security (BIS). These regulations prevent the export of US crude oil except to Canada or in specific circumstances from Alaska and California (see I Fought the Law). In Episode 1 of this series we discussed the consequences of a partial end to the ban on crude exports that might occur as a result of a change to the BIS definition of lease condensate – a very light hydrocarbon that is nevertheless defined as crude that cannot be exported. Production of lease condensate is booming in shale plays like the Eagle Ford in South Texas. Our analysis imagined that if the condensate export ban were lifted tomorrow, much of this material would be exported to Asia as a petrochemical feedstock. This time around we widen the debate to wonder what would happen if there were a complete removal of the ban on crude exports – including lease condensate.

The crude export regulations were written at a time when a shortage of oil threatened US security and prompted legislators to prevent domestic producers sending supplies overseas. Between the mid-80’s and 2009, US crude oil production was in long term decline meaning that dwindling domestic supplies were eagerly snapped up by US refiners and the export ban was never more than an occasional issue (such as when Alaska North Slope – ANS- production exceeded West Coast refinery requirements in the 90’s). Since 2010, however, the US has undergone a dramatic crude renaissance, principally as a result of the shale oil revolution. Current production is over 8.4 MMb/d – its highest level since October 1986 – up 50 percent since the start of 2011 (see Like A Bat Out of Hell). And while production is soaring, proved reserves are increasing even faster – laying the groundwork for continued output.

But although US crude production is surging, the country still imports upwards of 7 MMb/d to meet refining demand, so you might think that calls to end the export ban are premature. The trouble is there’s a mismatch between the quality of crude the US is now producing in abundance from shale, which contain a preponderance of light components, and refineries that are for the most part configured to process heavy crudes or light crudes that contain more middle or heavy distillate components than typical shale crudes (see The Charge of the Light Brigade). In effect, much of the new crude production is not best suited for processing in existing refineries without the latter undergoing potentially expensive and time consuming reconfiguration. The result is that crude supplies from prolific production in basins such as the Eagle Ford in South Texas and the Permian in West Texas are washing up at Gulf Coast refineries that are struggling to process so much light crude. And crude inventories at the Gulf Coast have recently reached record levels of close to 400 MMBbl even as refineries in that region run at over 90 percent of capacity.

In our view, the disposition and price impact of light crude surpluses are some of the most important issues in the crude oil and petroleum product markets today, and will continue to be for the next few years – regardless of what happens to BIS regulations. For that reason, RBN has joined with Turner, Mason and Company to provide a conference focused specifically on this topic. “Surviving the Flood of Light Crude Oil” is scheduled for August 19-20 in Houston, and is designed around many of the principles used at RBN’s School of Energy, including laptop computer access to all presentation materials and spreadsheets in real time, structured content from RBN and Turner Mason experts, and no executive project sales-pitches. Register now while space is still available. For more information on the conference, you can download the brochure here.

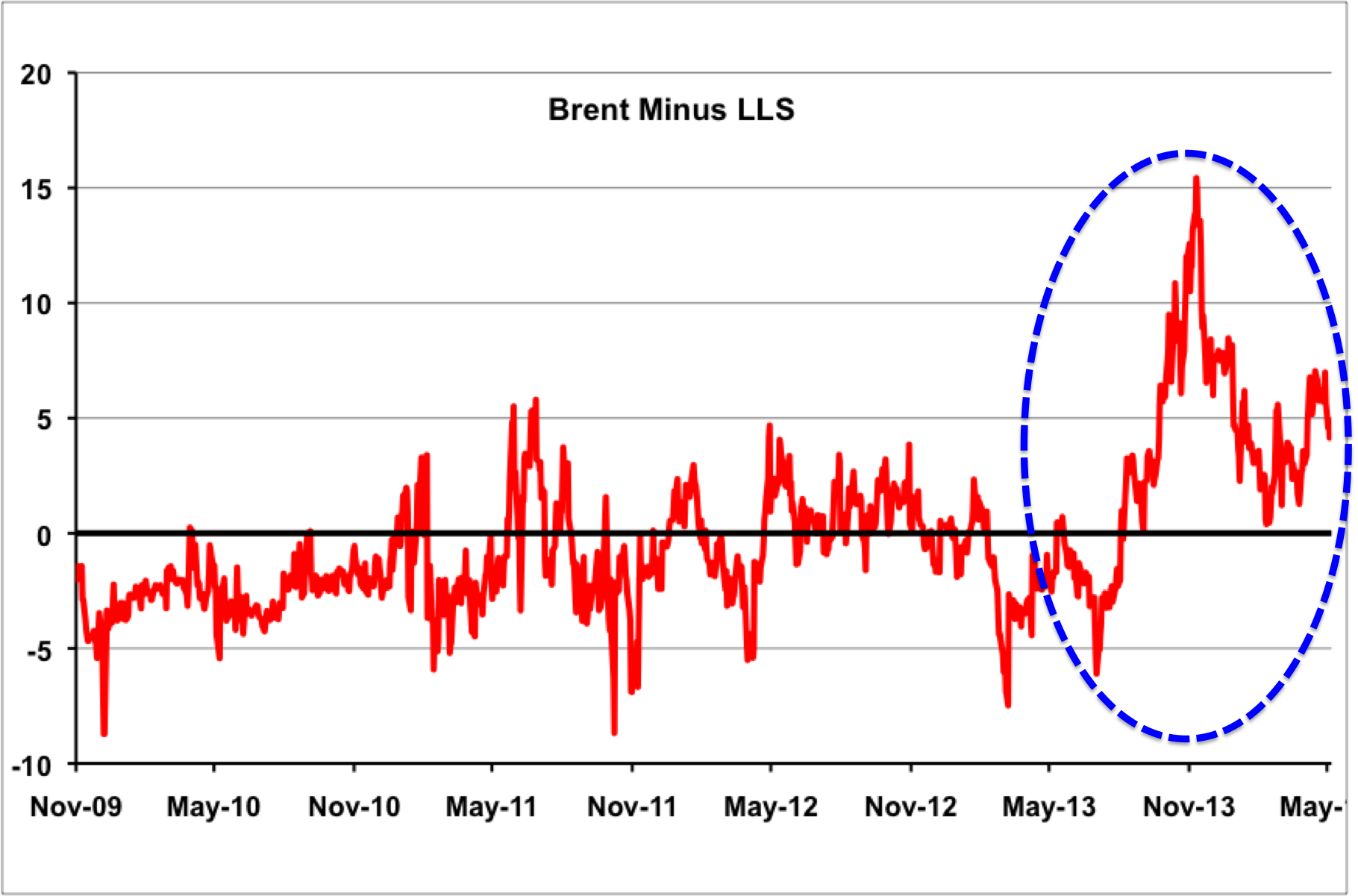

And of course the export ban poses a further challenge to the US crude quality mismatch because producers are required to sell their crude to US refiners rather than perhaps seeking more suitable buyers overseas that want to process light crude. As with any market where too much product is chasing after too few buyers, US crude producers are therefore getting less money for their barrels right now than they might if exports were permitted. The data in Figure #1 sheds light on this pricing issue. The red line is the premium of international benchmark light sweet crude Brent over the Gulf Coast equivalent crude benchmark, Light Louisiana Sweet (LLS). These two crudes have similar characteristics, so would expect to be valued fairly closely in international markets. And that is roughly how they traded until last summer. Between November 2009 and August 2013 Brent averaged about $1/Bbl under LLS – a little less than the cost of freight between the North Sea and the Gulf Coast.

Figure #1