Valero is the latest in a long line of US midstream companies to file their Master Limited Partnerships (MLPs) for an IPO – expected early in the New Year. These popular tax efficient entities were created over 25 years ago to encourage energy infrastructure investment. In the last four years the number of MLPs has shot up 50 percent. Today we describe how Valero’s MLP is structured.

Daily Energy Blog

Tuesday, 12/10/2013

Monday, 12/09/2013

Midstream infrastructure companies are investing heavily in facilities to gather, store and transport condensate and natural gasoline range materials in the Utica. The expectation is that production of these light hydrocarbons from the wellhead and gas processing/fractionation plants will increase significantly in 2014. Today we take a deep dive into two company’s plans for condensate and natural gasoline takeaway.

Sunday, 12/08/2013

Throughout the three year-long disruption of the US crude oil distribution system caused by rising domestic and Canadian production trying to find a path through the Midwest, the Seaway pipeline reversal project has been a market bellwether of progress to unwind the congestion. In 2Q 2014 the final phase will come online - opening up an additional 450 Mb/d capacity between Cushing and Houston. As the Seaway project has been built out, the crude surplus in the Midwest appears to have moved to the Gulf Coast. Today we detail the impact of Seaway Phase 3 on Gulf Coast crude supplies.

Thursday, 12/05/2013

Could the US end up exporting 700 MMb/d of crude to Canada by the end of the decade? Despite static domestic refinery demand and a growing production surplus, Canadian imports of crude increased this year. How could that be? The reason for this apparent anomaly is that East Coast Canadian producers are getting better prices exporting their crude anywhere but the US rather than competing at home against cheaper imports from South Texas and North Dakota. Today we explain some unintended consequences of the US crude export regulations.

Wednesday, 12/04/2013

Expanding Western Canadian Oil Sands production is currently butting up against pipeline constraints to move the crude to markets in the US and beyond. The result is painful price discounts for producers and an increased inventory of crude in storage at the Edmonton and Hardisty hubs in Alberta. New storage capacity is being added in both hubs to handle the growing volume. Today we detail TransCanada and MEG Energy expansion plans in Edmonton.

Tuesday, 12/03/2013

Output of naphtha range material such as plant condensates and natural gasoline in the Ohio section of the Utica shale is increasing rapidly as new processing and fractionation capacity in the region comes online. Output of field condensate from the wellhead is also expected to take off in 2014. These light hydrocarbons will be delivered to market by a combination of pipeline, rail and barge infrastructure. Today we look at pipeline infrastructure plans to deliver condensates and natural gasoline to Canada as diluent.

Monday, 12/02/2013

So far in 2013 around 645 Mb/d of new crude oil pipeline capacity has opened up to ship supplies to the Texas Gulf Coast. Early this month (December) line fill starts on the largest new capacity addition to date – the 700 Mb/d Keystone Gulf Coast Pipeline. The new pipeline runs from Cushing to Port Arthur and will carry mostly Canadian heavy crude. Today we wonder if all that crude will find a home.

The first episode in this series described 4 MMb/d of current and planned expansions to crude transportation capacity into the Texas Gulf Coast region (see Handling The Texas Gulf Coast Crude Flood). Our analysis showed that the new incoming light crude capacity will exceed Texas Gulf Coast demand by somewhere north of 0.5 MMb/d by the end of 2015. In episode two we described how some of these excess crude supplies would move east on the reversed Ho-Ho pipeline (see Gulf Coast Crude West to East Flows). In episode three we looked at how shippers could divert supplies away from Texas Gulf Coast congestion (see Texas Gulf Coast Bypass Options). This time we consider the impact of the Keystone Gulf Coast pipeline.

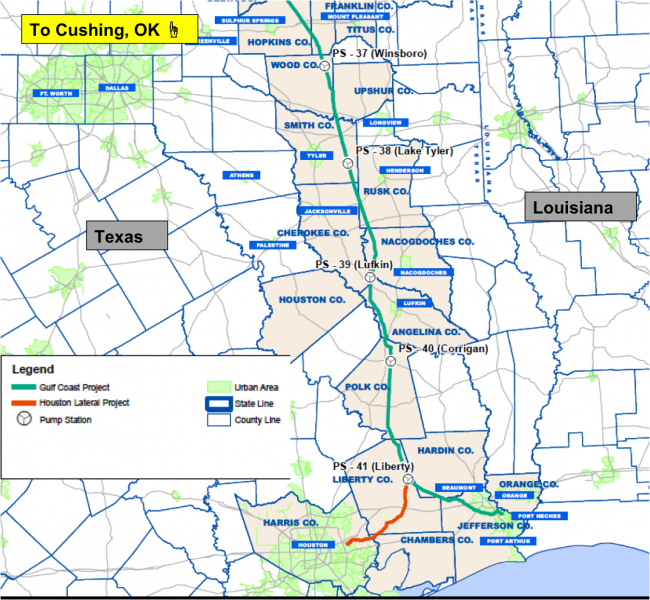

One of the more confusing features of the Keystone Gulf Coast Pipeline is what to call it – the name seems to change in real time. That is probably due to a desire to disassociate the southern Gulf Coast section of the pipeline from delays in permitting the Canada to US Keystone XL pipeline. Owner and operator TransCanada most recently set up a subsidiary to operate the pipeline called Marketlink LLC and it should now apparently more properly be called the Cushing Marketlink Pipeline so we will go with CMP as an abbreviation.

The 36-inch-diameter CMP runs 485 miles from Cushing, OK, to Nederland, TX (see green line on the map below). The line will have an initial capacity of 700 Mb/d with the option to expand to 830 Mb/d. It is almost ready to commence operations but before that can happen it has to be filled with oil – a process known as “line fill”. We described how line fill works and provided a formula to approximate the volume of oil required back in May 2012 (see A Time for Gas A Time For Crude – Part 2). According to that formula CMP requires 3.5 MMBbl of line fill. Marketlink LLC has said the first pipeline deliveries will be made before the end of 2013. The company is also constructing a 48-mile Houston Lateral pipeline (orange line on the map) that will run from the Liberty pumping station to East Houston and should be online by the end of 2014 with 130 Mb/d capacity.

Source: TransCanada Website and RBN Energy (Click to Enlarge)

The initial destination of the CMP is the Sunoco Logistics (part of Energy Transfer Partners) Nederland terminal. We have covered the Nederland terminal in two previous blog posts (see Nederland Crude Wonderland and Nederland Crude Volume Surges). The terminal is located on the Sabine-Neches waterway between Beaumont and Port Arthur, TX and has 22 MMBbl of storage capacity (see map below). The location is in the heart of Beaumont/Port Arthur refining country – home to four large refineries owned by ExxonMobil (Beaumont, 365 Mb/d), Valero (Port Arthur, 310 Mb/d), Total (Port Arthur, 174 Mb/d) and Shell/Saudi Aramco (Motiva 600 Mb/d). The Sabine Neches Waterway connects to the Gulf of Mexico, providing waterborne access to the entire Gulf Coast region. Nederland is about 100 miles East of Houston and 350 miles West of New Orleans.

Tuesday, 11/26/2013

Western Canadian producers regularly have to swallow large price discounts for heavy crude versus the US benchmark West Texas Intermediate (WTI). During the first week of November price discounts for heavy Western Canadian Select crude versus WTI came close to $42/Bbl – the deepest since 2007. Since then they have narrowed but are still over $30/Bbl. Today we examine the relationship between storage volumes in Alberta and crude price discounts.

Saturday, 11/23/2013

When over 4 MMb/d of new crude transportation capacity opens up to the Texas Gulf Coast by the end of 2015 shippers are likely to face congestion getting their supplies to refiners in the region. Given the U.S. Department of Commerce ban on exports, some of that crude needs to find a home elsewhere. Pipeline options to get crude supplies to Eastern Gulf refineries are limited to the Ho-Ho reversal project. Today we examine shipper alternatives.

Wednesday, 11/20/2013

Increasing production of naphtha range material such as condensates and natural gasoline in the southeastern Ohio section of the Utica shale will soon exceed the capacity of local refineries to process such light hydrocarbons. Midstream logistics companies like MPLX are developing infrastructure to transport condensate, natural gasoline and the more limited supplies of crude produced in the Utica to refineries further afield. There is also demand for condensate and natural gasoline to be used as diluent to reduce the viscosity of Western Canadian heavy crude bitumen. Today we describe MPLX and its sponsor Marathon Petroleum Corporation’s (MPC) recently announced long term takeaway transportation plans.

Tuesday, 11/19/2013

Finding a home for growing condensate range material being produced in the Ohio Utica shale play involves local refinery deliveries as well as new transport routes to markets outside the region as far away as Canada. Midstream companies are busy developing infrastructure plans to gather both wellhead condensate and output from natural gas processing plants in the region. Today we detail MPLX and its sponsor Marathon Petroleum Corporation’s (MPC) recently announced Utica shale plans.

Monday, 11/18/2013

Crude oil and diluent pipelines running through the two largest Canadian marketing and transportation hubs at Hardisty and Edmonton in Alberta have current capacity of 3.9 MMb/d. That will double to 8 MMb/d by 2018 if currently planned projects are completed. Getting the resultant expanding flows of crude and diluent in and out of Alberta via these hubs poses the same challenge that Gulf Coast operators are facing from the flood of crude descending on them from the US and Canada. Today we begin a new series detailing midstream Canadian terminal operations at Hardisty and Edmonton.

Sunday, 11/17/2013

We estimate that over 4 MMb/d of new crude transportation capacity will have opened up to the Texas Gulf Coast by the end of 2015 – to a region with just under 3.7 MMb/d of nameplate refining capacity. With crude exports restricted by Federal law, some of that crude is going to need to find a home – most likely at Eastern Gulf refineries in Louisiana and Mississippi. Today we look at how some of the incoming flood of crude could be redistributed across the Gulf Coast region.

Thursday, 11/14/2013

Owning a refinery in the middle of the fastest growing shale crude basin sounds like a good idea. Calumet Specialty Products LP thinks so – they purchased the 14.5 Mb/d San Antonio refinery in December 2012 located at the heart of the Eagle Ford. Since then Calumet has set about expanding production and organizing more efficient crude transportation. But owning such a small refinery near the largest refining region in the world has its risks. Today we describe how location and crude supply advantages help keep this refinery competitive.

Tuesday, 11/12/2013

The potential for the Tuscaloosa Marine Shale (TMS) tight-oil play to become the next big thing in U.S. oil production is attracting exploration and production companies willing to put some money at risk in the hope of big payoffs. The TMS seems to have a lot going for it. The play in central Louisiana and southwestern Mississippi is said to have seven billion barrels of oil in place deep below ground but only a stone’s throw from the pipeline networks, terminals and refineries of the Gulf Coast. But succeeding in TMS requires overcoming the play’s challenging characteristics through nuanced drilling techniques and completion formulas. Today in the second part of our series on TMS we examine what the E&P pioneers have accomplished so far in drilling and production, what they’re learning from their experience, and what it would take to turn TMS’s potential into reality.