Valero is the latest in a long line of US midstream companies to file their Master Limited Partnerships (MLPs) for an IPO – expected early in the New Year. These popular tax efficient entities were created over 25 years ago to encourage energy infrastructure investment. In the last four years the number of MLPs has shot up 50 percent. Today we describe how Valero’s MLP is structured.

First up a quick disclaimer. RBN Energy does not advocate investment in MLPs. We are not an investment advisor. The purpose of this article is not investment advice or endorsement.

We covered MLPs previously in two RBN blog posts last year (see Masters of the Midstream and MLPs Exit the Toll Road). If you are completely new to the topic you’ll probably benefit from reading at least the first of those blogs before you dive into this one. Otherwise make do with the Cliff Notes version in the next few paragraphs.

MLPs are a particular type of US corporate structure established by Federal tax reform legislation in 1986 to encourage investment in energy infrastructure. MLP businesses have to be partnerships engaged in “qualifying” natural resource activities, which back in the early days were limited to activities such as gathering, transporting and processing oil, natural gas and natural gas liquids (NGLs). They are typically businesses where income is derived from the volume of traffic using an asset such as a pipeline rather than owning the commodity that flows through. The toll road analogy is used to describe such fee-based business. Not all MLPs are fee based and some produce or refine hydrocarbons – exposing them to commodity price risk – that was the topic of last year’s second MLP blog (see MLPs Exit the Toll Road).

MLP partnerships are publically traded. A partnership differs from a regular “C” corporation because it is considered the aggregate of its partners rather than a separate entity. Instead of individual stockholders owning stock, the partners in an MLP own distinct pieces of the partnership called units. Because a partnership is not an entity, it pays no corporate taxes on its profits. Tax liabilities are instead “passed through” to individual unit holders who pay tax on their share of MLP profits. Unit holders typically receive cash distributions from their MLP every quarter based on earnings but are also allocated a share of depreciation on MLP assets that offsets the tax liability on cash distributions.

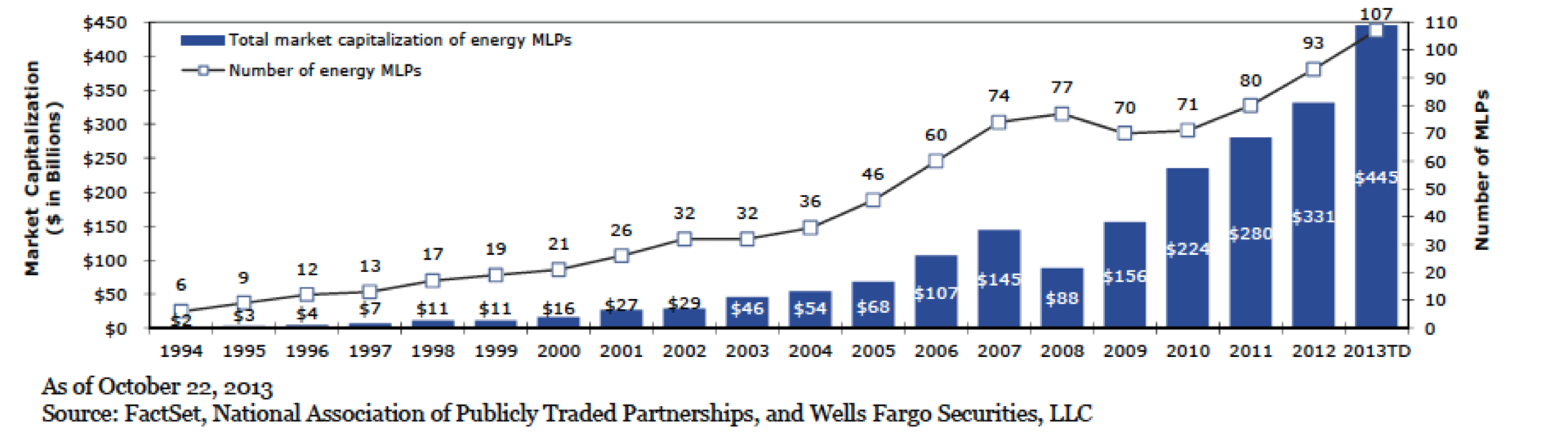

Because they are intended to produce regular and reliable income distributions for unit holders and because their tax structure results in lower total taxes than regular corporations, MLPs have become popular and important vehicles for energy midstream infrastructure companies. In the past four years the happy coincidence of a boom in US energy industry infrastructure needs and practically zero interest rates on alternative “safe” investments like bonds has combined to make MLPs extremely attractive to investors. They are also very appealing to midstream companies looking for ways to finance expensive infrastructure using funds with a low overall cost. The chart below, from an MLP primer presentation by Wells Fargo shows the growth in market capitalization and the numbers of MLPs since 1994. You can see that in the past four years, market capitalization increased from $224 Billion in 2010 to $445 Billion in the year to October 2013. Over the same period the number of publically traded MLPs increased by fifty percent from 71 to 107. As of this week, another 7 MLPs have filed for an Initial Public Offering (IPO) with the US Securities and Exchange Commission (SEC).

Source: Wells Fargo “Primer” on MLPs’

Another convenience of the MLP structure for midstream energy companies is that all unit holders are not equal. Most MLPs have two classes of ownership – General Partners (GPs) and Limited Partners (LPs). GPs control and manage the partnership’s operations in return for a (typically) 2 percent stake. LPs are the unit holders or investors who own the other 98 percent and are not involved in operations. GPs can also own incentive distribution rights (IDRs) that entitle them to receive a higher percentage of incremental cash distributions from the partnership when the distribution to LP unit holders reaches certain tiers – usually percentage levels. GPs retain firm control over an MLP – reducing the risk when a midstream energy company spins off assets into these structures. GPs can also realize significant upside return on a 2 percent investment through IDRs if the MLP assets perform well.

About the song

James Brown’s “Sex Machine” Album and hit song were released in 1970

Comments

What is the expected VLP annual percentage yield?

As I understand it, the MLP's distribution of 'units' are basically tax free, minus the tax headache of filing K-1 tax forms.

The Valero MLP offering is coming this year and should be priced this week. Also IPO proceeds for the most part are staying at the MLP not going to VLO.