This is Part V of a series on the Golden Age of Natural Gas Processors. The first four parts reviewed the crude-to-gas ratio at 50X, the impact of increasing NGL production on prices, the uplift value provided by gas processing, and who gets all the money. Today we examine the incredible magnitude of gas processor’s margins – if the processor has access to the right gas streams.

[Update: On Friday the crude-to-gas ratio remained on either side of 50X from a cash-vs-futures perspective. Henry Hub ICE cash dropped a penny to $2.00, April Futures closed at $2.126 down 2.3 cnts and prompt crude futures closed at $102.02/bbl, up 24 cnts. That brings the crude-to-gas ratio on a cash basis to 51X and on a futures basis to 48X].

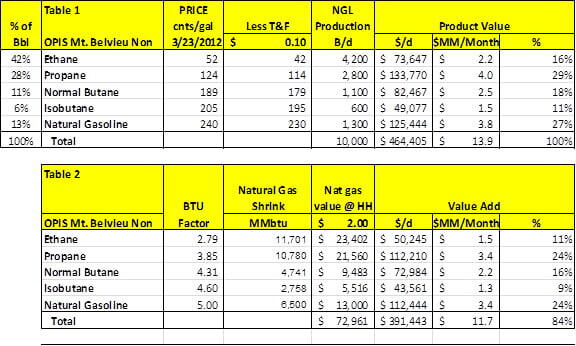

Tables 1 & 2 at the bottom of this page update the data in the previous postings of this series. They show how at today’s prices for natural gas and natural gas liquids, a representative processing plant producing 10,000 BPD of liquids in a typical yield pattern will generate $13.9 MM/month in product value, and $11.7 MM/month of value uplift.

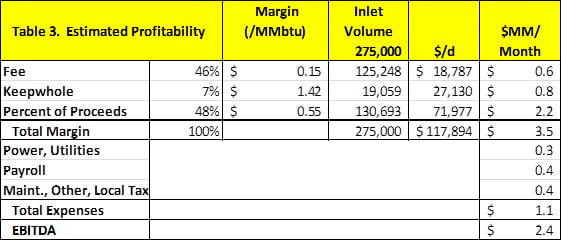

Table 3 (immediately below) translates that into bottom line profitability for our representative gas plant using a typical mix of processing contract structures [fixed-fee, keep-whole, and POP (percent-of-proceeds)] based on DCP Midstream’s contract mix and fee structure. Note that this calculation assumes the uplift margin from Table 2 for keep-whole and POP, rather than the DCP margins assumed in Part IV and adjusts for the BTU content of the inlet volume gas. This time the top line number comes out at $3.5 MM/Mo. This week we also include typical operating costs for a plant of this size of $1.1 MM/Mo., which leaves an EBITDA of $2.4 MM/Mo. That sounds like a pretty good return, right?

Yea, pretty good in most businesses. But in the natural gas processing industry in 2012, this is relatively meager. The reason is the BTU content of the gas. This gas is relatively lean. We’ll get back to the economics in a minute, but first a brief detour to cover the difference between lean and rich gas – as measured by the BTU of the gas and it’s GPM.

GPM stands for gallons per MCF, which means gallons of NGLs produced per thousand cubic feet (MCF) of gas processed. The richer your gas, the more gallons you get. A typical lean stream has a BTU content of 1,050 or less. That is basically pipeline quality gas. GPM on that gas is 1-2. We can easily calculate the GPM on our sample gas plant. NGL production is 10,000 b/d. Times 42 = 420,000 gallons/day. Divided by our inlet volume of 250,000 on an MCF basis yields a GPM of 1.68. At our representative mix of NGL products that’s a BTU content of about 1,100. So for every 1,000 cubic feet of natural gas, our plant can extract 1.68 gallons of NGLs.

Table 4 shows the typical ranges of BTU and GPM numbers. Our plant is in the lean range based on GPM, and just over the rich line in the BTU category. Clearly it makes a lot of economic sense to process this gas stream. But processing is only marginally necessary from a gas quality perspective. There were times in some parts of the country when gas this lean was not processed.

So what happens when richer gas is processed? Let’s do the math. What if our sample plant generated twice as many NGL barrels on the same volume of gas. That would be 20,000 b/d times 42 = 840,000 gallons/d. Divided by 250,000 yields a GPM of 3.36. That’s high but by no means unusual in today’s wet plays. Ponder that. Twice as much product from the same quantity of gas. It’s twice as much shrinkage (BTUs removed from the gas) but that volume is valued at the price of natural gas – from $400k to $800k per month – chump change compared to the revenue side. So we just added $3.0 MM to the gross margin line, and almost $3.0 MM to the EBITDA. Costs are relatively the same (assuming of course, our plant has the capacity to produce and transport this volume of liquids). But profits are up 225%.

As long as we are pondering, why stop there. What if we get four times the NGL volume from the gas. That would be 40,000 b/d times 42 = 1,680,000 gallons/d. Divided by 250,000 yields a GPM of 6.7. Very rich gas, but certainly within the range of some Eagle Ford and Granite Wash gas streams. That is four times the volume of liquids from the same quantity of natural gas.

Hey, the spreadsheet says profits are up from our base case by almost 500% to about $11 MM per month. Now that’s profit.

Given the magnitude of these numbers, is it any wonder why producers are chasing wet gas plays. Remember we are only showing the 30% of the profitability that goes to the processor in the calculations above. 70% of the uplift is going to the producer.

This is the golden age of natural gas processing. Companies in the right spots with the right contract structures are printing money. Someday it will end, but at this point that day does not look soon. So in the famous words of Rufus from Bill & Ted’s Excellent Adventure, Party on Dudes!

---------------------------------------------------

Tables 1 and 2 below show the base case calculations used above.

---------------------------------------------------

We’ve got something new on RBN starting last Friday. Check out Updata’s daily technical analysis for natural gas and crude markets here.

Comments

I dont understand the relationship of how the BTU factor allows you to calculate a natural gas shrink and therefore expense. How does or does not the caculation of natural gas shrink affect your natural gas processing value calculation from your blog series How Rich is Rich? Thank you for your assistance. Monica