This is Part IV of a multi-part series on the Golden Age of Natural Gas Processors. The first three parts covered the following topics:

- Part I – Crude-to-gas ratio; historical trends; Influence on natural gas processing; frac spreads

- Part II - Impact of increasing NGL production on prices, and how NGL markets are responding to the price changes.

- Part III - Uplift in value provided by natural gas processing at today’s prices – how the math works

Today we look at how much money natural gas plants make, who gets the money and what that means for both producers and processors.

[Update: The crude-to-gas ratio was back above 50X on a cash basis on Friday. Henry Hub ICE cash dropped to $2.074, April Futures closed at $2.275 and prompt crude futures continued to cycle up and down, this time closing at $106.87. That brings the crude-to-gas ratio on a cash basis to 51.5X and on a futures basis to 47X].

Table 1 below is similar to the numbers we’ve reviewed previously in this series, except that it (a) updates the prices to Friday 3/23, and (b) adds a column for Transportation and Fractionation (10 cnts/gal). That is a representative cost for moving raw mix (y-grade) liquids from our plant to a fractionator and then paying the cost of fractionating the mixed stream into purity products. Total product value per month generated by our 10,000 b/d of NGL production is $14.2 MM.

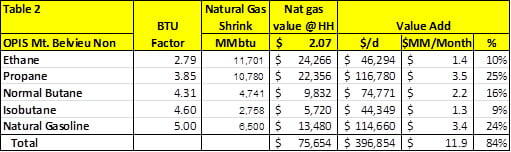

Table 2 is similar to the shrinkage table reviewed last Thursday in Part III. It shows that the daily BTU value of the gas extracted to make the liquids (based on Friday’s ICE cash price at HH) is $76k, for a total value add of $397k/day or $11.9MM per month.

So who gets all this money? The answer depends on the type of contracts that are in place between the producer who owns the gas and the processor who owns the plant. There are three basic types of contract structures used by the processing industry: fixed-fee contracts, keep-whole contracts, and percent-of-proceeds (POP) contracts.

Fixed fee – Just what it says. The gas processing plant charges the producer a fixed fee for processing the gas. Usually the deal is on a Mcf or MMbtu basis. In this case all of the uplift on liquids prices (or lack thereof in historical times) goes to the producer. The processor has no commodity risk whatsoever, and has no exposure to NGL prices. This was a good thing a few years ago when the frac spread was upside down (gas high relative to NGL prices). Now commodity risk looks like free money.

In keep-whole deals, the processor returns dry (processed) gas to the producer equal to the total volume delivered at the plant inlet. In this case the processor bears all of the processing margin risk, and gets all of the uplift from the frac spread. When frac spreads were low, processors were hurt by these deals and many were converted to fixed fee contracts. Of course, with today’s astronomical frac spreads, there is a lot of remorse over those conversions. Processors with significant volumes on keep-whole deals are printing money.

Percent of proceeds deals share the risk and reward between processor and producer. Basically the processor gets a percentage of NGLs and natural gas from the producer as a processing fee. The percentage sharing arrangement between NGLs and gas determines the exposure of the producer and the processor to the frac spread at the plant.

Of course, each processor has a different mix of these contracting methods. But to get a general sense of the numbers we can look at a quarterly report detailing the volume, $ margin and unit margin by contract type prepared by DCP midstream, the largest NGL producer in the U.S. A summary of this report is shown in Table 3 below.

In Q4 2011, fee business made up 46% of DCP’s processing volume, but only 14% of the company’s gross margin. The fee-based business realized a margin of 15 cnts/MMbtu. In this case, the producer is getting all of the uplift except for the 15 cnt/MMbtu fee. Keepwhole was only 7% volumetrically, but generated 25% of gross margin. DCP is retaining 100% of the uplift on this small volume, which produced a huge profit margin of $1.68/MMbtu. The percent of proceeds deals made up 48% of the volume and 63% of gross margin, for a margin of $.65/MMbtu. See the full DCP report at:

https://www.dcpmidstream.com/Investors%20and%20News/Pages/Margin.aspx

Let’s use DCPs numbers to estimate the frac spread split between producers and processors for our example plant described in Tables 1 and 2 above. We’ll also need an inlet volume number for our plant, so let’s assume 250,000 Mcf/d, a reasonable estimate for a 10,000 B/d plant. If we split the plant using DCP’s percentage volumes for each method, and then multiply DCPs margin by the resulting volume, this gives us an estimate of the total margin for this plant if it were to exactly match DCPs volume mix and margin for Q4 2011. The answer as shown in Table 3 is $3.7 MM/month, or about 30% of the total uplift of $11.9 MM/month (Table 2).

Of course this is a very rough estimate of who is getting the money. Most likely DCP is in a better negotiating position than most gas processors, and so has improved its deals over the past couple of years to keep a higher percentage of the uplift. Nevertheless, it does provide a reasonable indication of how much of the uplift is going to the producer and how much to the processor. Industry “talking numbers” confirm that most processors are keeping 10%-30% of today’s uplift, depending on a wide range of factors.

This split looks like a good thing for both producers and processors. But there are a few more factors we need to look at to fully understand the market implications of a 50X crude-to-gas ratio. For example, how much money are plants making after expenses? What have hedging programs done to that profitability this year? What does it cost to build one of these plants and then to move the NGL products to market. We’ll look at these issues as this series continues later this week.