This post continues yesterday’s review of the Golden Age of Natural Gas Processors, an analysis of the 50X crude-to-gas ratio on the economics of natural gas processing and the market for natural gas liquids. To fully understand this post, first see The Golden Age of Natural Gas Processors – NGLs in a 50X Crude-to-Gas Ratio World. Today we look at the impact of increasing NGL production on prices, and how NGL markets are responding to the price changes.

--------------------------------------------------------

One of the most significant effects of the high crude-to-gas ratio has been the steady march of drilling to high btu gas and crude oil plays. It simply makes no sense to drill for dry natural gas with prices in the $2.00/MMbtu range. The result as noted many times in RBN postings (most recently in Turn, Turn, Turn Around), NGL production is up significantly and is now approaching 2.5 MMb/d. Over the past three years, production for the individual NGLs are all up significantly: Natural gasoline +19%. Isobutane +24%. Normal butane +17%. Propane +26%. And of course, ethane +45%, exceeding 1.0 MMb/d in December.

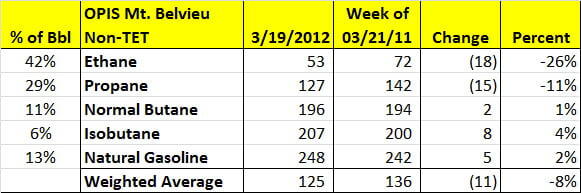

All that additional production has had an impact on price. To understand the market consequences, we must look at the product level details. As is often the case with NGLs, averages can obscure the facts. The table below shows OPIS Mt. Belvieu Non-TET prices for yesterday, and for about one year ago – the week of March 21st. The prices are weighted by a typical gas plant % yield of NGLs. The weighed average price is down by only 8%, or 11 cnts. That doesn’t sound like much given all of the new production. But at the product level there are big differences --- Ethane prices off 26%, Propane off 11%. Heavies (Normal, Iso and Natural) all up slightly. (Prices below in cnts/gal; so for example, propane yesterday was $1.27/gal)

The weakness in NGLs contrasts with crude oil, which was running about $100/bbl this time last year. At $108 currently that’s a 8% increase. Thus the light NGLs are substantially weaker relative to crude, and the heavy NGLs are slightly weaker relative to crude. Before we start feeling sorry for gas processors, let’s not forget that natural gas prices are down from about $4.00 to about $2.14, or -46%. So processing margins (frac spreads, as discussed yesterday) still look extremely attractive.

Clearly these numbers tell us that there are material differences in the way that the individual NGLs are responding to growth in NGL production. Ethane has seen the greatest increase in production and the most pressure on prices. Frankly the ability of the U.S. petrochemical industry to absorb all of the additional ethane has been pretty amazing. At today’s ethane price, it remains the most preferred feedstock for ethylene crackers, and that is keeping the ethane market relatively in balance.

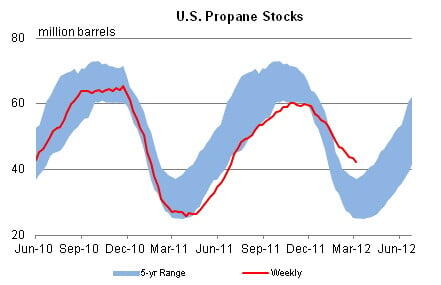

Propane has had a triple whammy. (1) Production is up. (2) It has been bested by ethane as the preferred ethylene feedstock for years. And (3) 2011-12 was the year-of-no-winter, killing the business for propane distributors. Propane prices have been holding up pretty well under the circumstances, but you can’t ignore the lagging inventory drawdown over the past few weeks. See the EIA graph below. There is a lot of propane being shipped to markets in Latin America (see The Long Way Around: Propane from shale gas gets to the Far East), but that probably won’t be enough of an influence on price to offset the inventory build that is starting up this week. Prices will be weaker this summer (unless crude prices go crazy).

The heavy NGLs – normal butane, isobutane and natural gasoline have been holding relatively steady relative to crude oil. In the coming weeks, normal will get softer as stricter summer RVP regulations kick into place, reducing the amount of normal that can be blended into motor gasoline. Iso will increase on a relative basis as refineries crank up utilization for the summer and use more iso in their alkylation units. Natural gasoline is still finding a home as a diluent for oil sands production in Canada, as well as its traditional use in motor gasoline blending.

In summary, we can say that NGL prices are slightly weaker than last year, even more so as compared to crude prices. But these numbers are still extremely strong relative to natural gas. So natural gas processing remains in the golden age.

In the next Golden Age blog we’ll look at the profitability of natural gas processing – how much money natural gas plants make, who gets the money and what that means for the evolution of this market and this industry.

Comments

For those of you that interested in more on this topic, please visit: http://www.bentekenergy.com/GreatNGLSurge.aspx#2011 and feel free to email me via [email protected].

For those of you that interested in more on this topic, please visit: http://www.bentekenergy.com/GreatNGLSurge.aspx#2011 and feel free to email me via [email protected].