In the previous posts of this series (Part I and Part II) we’ve looked at the relationship between NGLs and crude (weaker), the differences between the price performance of light and heavy NGLs (weaker vs. stronger) the frac spread for a typical plant (huge). Assuming we buy the logic that the crude-to-gas ratio will be this healthy for quite some time, what does that mean for the profitability of natural gas processing – how much value is created when wet natural gas is processed?

[Update: The crude-to-gas ratio has come in slightly in the past couple of days Henry Hub ICE cash increased to $2.21, April Futures closed at $2.36 and prompt crude futures bounced down and then back up to $107 (for May delivery). That brings the crude-to-gas ratio on a cash basis to 49X and on a futures basis to 46X].

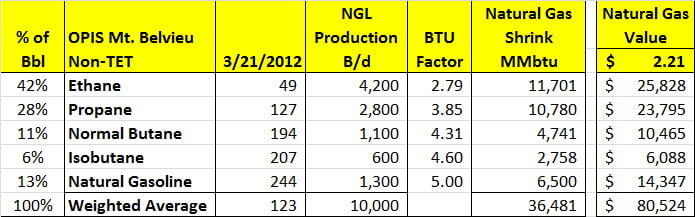

First let’s look at the revenue side. The table below on the left shows OPIS Mt. Belvieu Non-TET prices for yesterday, and for about one year ago – the week of March 21st. This is an update of the numbers discussed here in Part II on Tuesday which covered the price changes over the past year. The prices are weighted by a typical gas plant % yield of NGLs. On the right side we show calculations for the value of NGLs sold at these prices for our typical plant producing 10,000 barrels per day (b/d). So for example, at a 42% yield of ethane, the plant produces 4,200 b/d of that product. At yesterday’s price of $0.49 per gallon, that equals $87,098/day, or $2.6MM per month. Here’s the math: ethane at $0.49 * 42gal/bbl = $20.58/Bbl. Times 4,200 bbls = $87,098.

A couple of things to note. First, the value of products from this typical 10,000 B/d plant is $15.3 MM per month. That’s a lot of money. And second, the value of the ethane barrels produced at our plant is quite different from the yield of ethane at the plant – simply because the price of ethane is only 20% of the price of natural gasoline, and 39% of the price of propane. Ethane is a big part of the barrel but a much smaller part of the value added through processing of natural gas. Taken together, the two light NGLs – ethane and propane – make up 71% of the NGL barrel but only 47% of the value of the products produced by our typical plant.

The numbers get even more interesting when you look at the cost side – the value of the hydrocarbon molecules in these products at natural gas prices. This is the “shrinkage”, or the BTU value of the products extracted from the gas stream. The table below shows how these calculations work.

Looking again at ethane, the product has a BTU factor of 2.79. That means ethane has about 66,500 Btus/gallon * 42 = 2,790,000 Btus/Barrel / 1,000,000 = 2.79 MMbtu/bbl. So if we multiply the barrels produced of 4,200 * 2.79, we get 11,701 MMbtu of natural gas shrinkage necessary to produce our $87,098 of ethane. At a $2.21/MMbtu natural gas price, that gas is worth $25,828.

Note the differences between the value of the gas used to produce the product and the value of the product itself. It takes $25.8k of gas to produce $87.1k of ethane. But it only takes $14.3k of natural gas to produce $133k of natural gasoline. And that is the moral of this story. The uplift on heavy products is vast in comparison to light products. Translation, the typical natural gas processing plant makes most of its money on heavies. High prices of the heavies are the driver behind the huge uplift in value where $36.9k of natural gas can produce $511k of NGL products.

The obvious implication is that natural gas processing margins are highly dependent on the prices of butanes and natural gasoline. Recall from the previous Golden Age blogs that those are the products which have had the most resilient prices, and are most closely tied to the price of crude oil. Ethane and propane prices are significant for processing plant margins, but much less so than the heavy products. And it is those prices which have been weakest. The bottom line – today’s processing margins are likely to stay quite strong even if ethane and propane prices weaken further due to increasing supplies.

One final conclusion. The uplift in value shown by these calculations is huge. Who is realizing that value uplift and what determines the split of the dollars? That will be the subject of our next Golden Age blog.