Yesterday the price of ethane in E/P mix in Conway dropped again, now down to 14.5 cnts/gal, or $6.09/Bbl. A lot of the ethane barrels that move down the ONEOK Overland Pass NGL pipeline from Opal, WY to Conway, KS get priced out based on Conway ethane numbers. We talked about this situation last Wednesday in Not Gonna Lie.

Purity non-TET ethane in Mt. Belvieu, TX held up at 46.1 cnts/gal, or $19.36/Bbl. Still this is about half of the Mt. Belvieu price in January 2012. So ethane prices are down. What does this mean for producers and gas processors? Moreover, ethane supply is projected to increase by more than 50% over the next five years. That’s a lot of ethane. Which will probably crush the price. Will that kill the wet gas goose that is laying all the golden eggs? We better look at the numbers carefully.

| This is Part VI of a multi-part series on the Golden Age of Natural Gas Processors. The first five parts covered the Crude-to-Gas Ratio, Increasing NGL production, Uplift Calculation Math, Gas Plant Profitability, and the relationship between GPM and processing returns. Today we look at the sensitivity of total processing uplift and plant profitability to ethane prices. |

There is only one market for ethane, and that is the petrochemical market. Over the next few months several petchems will upgrade their facilities to run more ethane. But there is a good chance that ethane production will exceed the capacity of those upgrades in 2015, based on the Bentek projection in The Great NGL Surge. Until several new petchem plants are completed in the 2016 timeframe, it looks like ethane could be in a surplus supply situation.

The good news – bad news is that surplus ethane will not result in processing cutbacks.[1] Processing plants can produce the other NGLs (propane, butanes and natural gasoline) and reject the ethane. Rejection means that ethane is either left in the gas stream or blended into the plant tailgate gas stream and sold at natural gas prices (on a BTU Basis). Ok, the good news is that we don’t have to shut down the plant -- or the production upstream of the plant. But the bad news is that we don’t get ethane prices for ethane, we get lousy natural gas prices. How bad is that? For that answer we can look back at our sample plant revenue and value-add calculations that have been used in previous posts in this series.

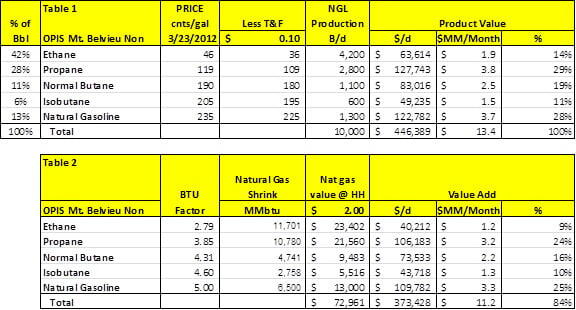

Tables 1 & 2 below are the same format we’ve used all along in this series, updated for yesterday’s OPIS Non-TET NGL prices. Our sample plant generates $446M/day or $13.4 MM/month based on current prices, while the shrinkage costs about $73/M/day. Thus the total uplift is $11.2 MM/month. But note one other important fact. Although ethane makes up 42% of the volume extracted from our plant, it generates only 14% of the revenue and only 9% of the value-add uplift. That is because ethane prices are so cheap relative to the other NGL products.

How cheap are they? Recall from Part III that ethane has about 66,500 BTU/gallon. If we multiply by 42 to get BTU/Bbl, that yields the BTU factor in the above table. (2,790,000 BTU/Barrel or 2.79). If we divide the price of ethane on a per barrel basis by the BTU factor, we’ll get the price of ethane on an MMBTU basis. (0.46 * 42) / 2.79 = $6.92/MMbtu. Obviously that’s a lot higher than the price of natural gas at $2.00 /MMbtu. But that number pales against natural gasoline. Here’s the same calculation with the natural gasoline price of 235 cnts/gallon, or $2.35/gallon, and using the natural gasoline BTU factor. (2.35 * 42) / 5.00 = $19.74/MMbtu. So natural gasoline is almost three times the price of ethane on a BTU basis and almost ten times the price of natural gas.

We worked all of this math to establish the simple fact that the heavy NGLs (butanes and natural gasoline) are worth a lot more than ethane. And a whole lot more than gas.

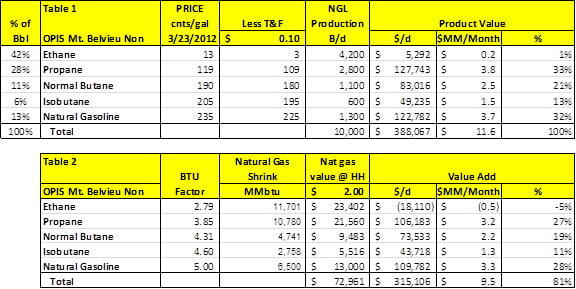

So now let’s reverse our calculation. What would the price of ethane be if it were to fall to fuel value. Except for brief aberrations, ethane should not fall below its value in the natural gas stream since ethane can be rejected at the plant and sold as natural gas. Using a $2.00 natural gas price, that would be (2.00 * 2.79)/42 = $0.13 or 13 cnts/gal. (BTW, pretty close to the price of ethane in Conway yesterday.)

So let’s plug this ethane price into our calculation table below. Product value dropped from $13.4 MM/Month to $11.6 MM/Month. Value-add dropped from $11.2 MM/Month to $9.5 MM/Month. That’s $1.7 MM/Month, certainly nothing to sneeze at. But in the big scheme of life it is only a 15% hit off an extremely profitable value-add calculation.

Here’s the moral to this story. Ethane don’t matter to me. Ok, perhaps that is a bit of an overstatement. It matters, but the uplift on the other four NGLs is so astronomical at today’s price levels that both producer and processor will continue to be very profitable. And the wetter the gas (e.g, the higher the BTU content), the less ethane matters, because the uplift is just that much more money, regardless of the ethane value.