U.S. interstates are populated with electronic displays that update drivers in real-time on traffic conditions, road closures, weather alerts and other important events. If there was a sign for executives steering our nation’s oil and gas producers, it would likely read “Poor Visibility, Slow Down Ahead.” After a short-lived price rally in Q1 2025, the industry faced lower commodity realizations and macroeconomic headwinds in Q2 2025, which spooked investors and hardened a cautious investment approach. In today’s RBN blog, we analyze the latest results of the 39 major U.S. E&P companies we cover and look at what’s ahead.

Analyst Insights are unique perspectives provided by RBN analysts about energy markets developments. The Insights may cover a wide range of information, such as industry trends, fundamentals, competitive landscape, or other market rumblings. These Insights are designed to be bite-size but punchy analysis so that readers can stay abreast of the most important market changes.

ExxonMobil announced on Tuesday, August 26, 2025, that it has reached Final Investment Decision (FID) on a large-scale reconfiguration project at its Baytown, Texas Refinery and Petrochemical Complex.

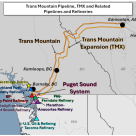

The Trans Mountain Pipeline Expansion (TMX) has been running “spectacularly well since startup” and plans are being considered to boost the pipeline’s capacity, Trans Mountain Chief Financial Officer Todd Stack said during a fireside chat Wednesday at RBN’s School of Energy Canada in Calgary.

A primary focus of E&Ps during the Shale Era has been driving down the cost of drilling and completing wells — doing so lowers producers’ break-even costs and increases their profitability. With the volumes of frac sand being used in the Permian and many other plays having grown dramatically in the past five years, a big push is on not only to minimize the cost of the sand itself, but to maximize the efficiency of sand delivery and sand management at the well site. All this has been spurring E&Ps to assume responsibility from oilfield service companies for the frac sand supply chain — anything from directly sourcing the sand to managing “last-mile” logistics. Today, we continue our series on the rapidly changing frac-sand world, this time concentrating on producers’ growing involvement in sand procurement and management.

Some shipowners plan to comply with the IMO 2020 deadlines for limiting sulfur in ship emissions by installing scrubber devices to clean the exhaust generated by burning less expensive high-sulfur bunker fuel. For many, this may work out to be more economical, at least in the interim, than using more costly IMO 2020-compliant fuel with sulfur content of no more than 0.5% or converting the vessel to run on an altogether different fuel such as liquefied natural gas. However, narrowing “sulfur spreads” this year have put that compliance strategy at risk by tripling the time it would take for shipowners to recoup their scrubber investments. Today, we continue an analysis of the changing economics of scrubber installation in the run-up to IMO 2020.

Crude production is at all-time highs in the Bakken and the Niobrara, and the latest pipeline-capacity expansions out of both regions have been filling up fast. At the same time, producers in Western Canada are dealing with major takeaway constraints and are on the hunt for still more pipeline space. Midstream companies are trying to oblige, proposing solutions like a major Pony Express expansion or a new Bakken-to-Rockies-to-Gulf Coast fix — the Liberty and Red Oak pipelines — that could help address all of the above. The catch is that, with multiple producing areas funneling crude along the same general eastern-Rockies corridor and the outlook for continued production growth uncertain, how’s a shipper to know whether to sign a long-term deal for some of the incremental pipe capacity now being offered? Today, we consider the need for new takeaway capacity, the potential for an overbuild scenario, and what it all means for producers and shippers.

Over the past three years, the U.S. frac sand market has been transformed. Demand for the sand used in hydraulic fracturing is more than twice what it was in early 2016. Dozens of new “local” sand mines have come online, slashing the need for railed-in Northern White Sand in the Permian and a number of other fast-growing plays. Frac sand prices have fallen sharply from their 2017 highs. And exploration and production companies, which traditionally outsourced sand procurement and “last-mile” sand logistics to pressure pumpers and other specialists, are taking a more hands-on approach. It’s a whole new world. Today, we continue our series on the major upheavals rocking the frac sand world in 2019 with a look at the development of local sand sources in the Eagle Ford, SCOOP/STACK and the Haynesville.

Enbridge is taking a serious look at converting its Southern Lights pipeline, which currently transports diluent northwest from Illinois to Alberta, to a 150-Mb/d crude oil pipe that would flow southeast. The potential reversal of Southern Lights is made possible by the facts that Western Canadian production of natural gasoline and condensate — two leading diluents — has been rising fast, and that demand for piped-in diluent from the Lower 48 is on the wane. Alberta producers could sure use more crude pipeline capacity out of the region — and getting crude down to the U.S. Midwest would give them good access to a variety of markets. With Western Canadian diluent production increasing fast, maybe Kinder Morgan’s Cochin Pipeline, another diluent carrier, could also be flipped to crude service later on. Today, we consider how Southern Lights’ conversion/reversal might help.

The U.S. frac sand market has been turned on its head. Over the past three years, demand for the sand used in hydraulic fracturing has more than doubled, dozens of new “local” sand mines have been popping up within the Permian and other fast-growing plays, and frac sand prices have fallen sharply from their 2017 highs. The big changes don’t end there. Exploration and production companies (E&Ps), who traditionally left sand procurement to the pressure pumping companies that complete their wells, are taking a more hands-on approach. And everyone is super-focused on optimizing their “last-mile” frac sand logistics — the delivery of sand by truck, plus unloading and storage of sand at the well site — with an eye toward minimizing completion costs and maximizing productivity. Today, we begin a blog series on the major upheavals rocking the frac sand world in 2019.

Last year, the impending implementation of International Maritime Organization’s rule mandating the use of lower-sulfur marine fuels starting January 1, 2020, widened the price spread between rule-compliant 0.5%-sulfur bunker and the 3.5%-sulfur marine fuel that has been a shipping industry mainstay. Traders’ thinking was that demand for high-sulfur bunker would evaporate in the run-up to IMO 2020, as the new rule is known. But since early January, the spread between low- and high-sulfur fuel at the Gulf Coast has narrowed from nearly $11/bbl to less than $2/bbl. The culprit is a shortage of heavy-sour crude caused by a number of factors. Today, we begin a two-part series on low-sulfur vs. high-sulfur fuel and crude values as IMO 2020 approaches.

By mid-year, Enbridge plans to initiate an open season for long-term, firm capacity on its existing 2.8-MMb/d Mainline crude system from Western Canada to the U.S. Midwest starting in mid-2021. Securing a sure way for Western Canadian heavy-crude producers to export crude from the Alberta oil-sands region — combined with additional southbound pipeline capacity from the Midwest to the Gulf Coast, would give Texas and Louisiana refineries an alternative to using overseas imports and would boost crude volumes being shipped from existing and planned export terminals. Today, we conclude our series on the pipeline’s contracting plans with a look at the impact of a straight-shot, joint-tariff pipe as well as joint pipe-barge transportation solutions from the oil sands to the Gulf Coast.

Increasing U.S. shale oil production has benefitted many U.S. refineries, but along the Gulf Coast, the primary beneficiaries have been in Texas. As production increased in the Permian and Eagle Ford plays, new pipelines were built to supply refinery centers in Corpus Christi, Houston, and Beaumont/Port Arthur. In contrast, the availability of shale crude by pipeline to refineries in Southeast Louisiana has lagged. However, new pipeline capacity to the crude hub in St. James, LA, is about to change the dynamic in a major way. Today, we continue our series on St. James by discussing the Bayou State’s refinery infrastructure and how new pipelines could impact refinery crude slates.

The U.S. midstream sector has been on a development binge the past few years, mostly in an effort to catch up — and then keep up — with production growth in the Shale Era’s two premier plays: the Marcellus/Utica in the Northeast and the Permian Basin in West Texas and southeastern New Mexico. What’s sometimes overlooked, however, is that significant numbers of new pipelines, processing plants and other key assets are being built in smaller, lower-profile production areas. The Niobrara’s Denver-Julesburg and Powder River basins are cases in point. Exploration and production activity in the D-J in particular has been soaring, and the resulting gains in crude oil, natural gas and NGL output has been stressing the region’s hydrocarbon-related infrastructure, thus spurring the development of new processing plants and pipelines. Also, interest in the Powder has been renewed — production there has been rebounding after crude-production ups and downs and gas-production declines through the 2010s. Today, we discuss highlights from RBN’s new Drill Down Report on the Niobrara production region.

In the past month, two integrated majors with strong footprints in the Permian Basin announced plans to increase their refining capacity along the Texas Gulf Coast. During the last week of January 2019, ExxonMobil announced a final investment decision to expand its Beaumont, TX, facility’s capacity by 250 Mb/d, making it the largest U.S. refinery, and then confirmed an investment with Plains All American and Lotus Midstream to build a 1-MMb/d pipeline to ship crude to its Beaumont and Baytown, TX, refineries. In the same week, Chevron announced its purchase of the 110-Mb/d Pasadena, TX, Houston Ship Channel refinery from Brazil’s national oil company, Petrobras. Both Exxon and Chevron boasted record Permian production in their fourth quarter 2018 earnings calls. Today, we review Chevron’s purchase and Exxon’s expansion in light of Permian production growth and the changing Gulf Coast refining market.

Enbridge’s 2.8-MMb/d Mainline system from Alberta to the U.S. Midwest has been running close to full, as have the other crude oil pipelines out of Western Canada. The Mainline is a unicorn among these pipes, however, in that none of its capacity — zilch — is under long-term contract. Instead, under Enbridge’s almost nine-year-old Competitive Tolling Settlement (CTS), shippers each month submit nominations stating the volumes of crude they would like to transport the following month on various elements of the Mainline system, then hope they get what they need when the available capacity is divvied up. In an effort to give producers and refiners the pipeline-capacity certainty they say they want — and to optimize the efficiency of the Mainline’s operation — Enbridge has been working with shippers on a CTS-replacement plan that would commit as much as 90% of the capacity on the pipeline system to shippers who enter into long-term contracts. Today, we continue this blog series with a look at how the prospective “priority access” capacity-allocation system is shaping up, how it might affect planned pipeline projects, and how it may facilitate the transport of a lot more crude from Alberta to the U.S. Gulf Coast.

Crude-by-rail (CBR) has been a saving grace for many Canadian oil producers. With extremely limited pipeline takeaway capacity, rail options from Western Canada to multiple markets in the U.S. have acted as a relief valve for prices — there for producers when they need it, in the background when they don’t. In 2018, we saw a major resurgence in CBR activity from our neighbors to the north, with volumes reaching an all-time high of 330 Mb/d just this past November. But just as quickly as CBR seemed ready for takeoff, the rug got pulled out from underneath those midstream rail providers and traders who had lined up deals and railcars to take advantage of wide price spreads. When Alberta’s provincial government announced its 325-Mb/d production curtailment beginning at the start of 2019, many midstream/marketing and integrated oil companies bemoaned what it could potentially do to market opportunities. And they were spot-on. Wide price differentials for Canadian crudes to WTI disappeared quickly and eliminated most, if not all, of the economic incentive to move crude via rail, and even by pipeline. In today’s blog, we recap the recent move away from crude-by-rail by some of Canada’s largest CBR players, and discuss the risks of long-term CBR commitments in volatile times.

The recently mandated reduction in Alberta crude oil production has helped to ease takeaway constraints out of Western Canada, but only temporarily. Worse yet, it’s unclear how long it will take to add new takeaway capacity from challenged projects like the Trans Mountain Expansion Project or Keystone XL. In the midst of all this trouble and uncertainty, Enbridge is pursuing a potentially controversial plan to revamp how it allocates space — and charges for service — on its 2.8-MMb/d Mainline system, the primary conduit for heavy and light crudes from Western Canada to U.S. crude hubs and refineries. Today, we begin a series on the company’s push to shift to a system that would allocate most of the space on its multi-pipe Mainline system to shippers that sign long-term contracts.

The U.S. Treasury Department last week announced new sanctions on Petróleos de Venezuela, S.A. (PDVSA), the national oil company of Venezuela, that effectively halts imports of Venezuelan crude oil into the U.S. Given that the Venezuelan crude imported to the U.S. is of the heavy sour variety, which is not produced in large amounts in the U.S. (except for California), certain refineries along the Gulf Coast are left scrambling to find alternative sources of feedstock for their facilities. Today, we evaluate historical crude oil imports from Venezuela, the refineries that are most heavily impacted, and the potential effects of the sanctions on U.S. refiners.