Midstreamers developing natural gas takeaway capacity out of the Permian have understandably focused on pipelines to the Gulf Coast — and along the coast to LNG export terminals and other big gas consumers. But don’t forget the Desert Southwest, where demand for gas-fired power is soaring. Energy Transfer recently committed to building a 516-mile, 1.5-Bcf/d expansion to its Transwestern Pipeline system from West Texas to the Phoenix area, and hinted that it might double the project’s capacity due to the high level of interest. In today’s RBN blog, we discuss Energy Transfer’s aptly named Desert Southwest Project, what drove its quick progress to a final investment decision (FID), and what other westbound projects out of the Permian might still happen.

Analyst Insights are unique perspectives provided by RBN analysts about energy markets developments. The Insights may cover a wide range of information, such as industry trends, fundamentals, competitive landscape, or other market rumblings. These Insights are designed to be bite-size but punchy analysis so that readers can stay abreast of the most important market changes.

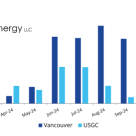

Crude oil exports out of Western Canada are nothing new but startup of the 590-Mb/d Trans Mountain Pipeline Expansion (TMX) quickly turned Canada into a global leader in waterborne crude exports, Jeff Kralowetz, Vice President of Business Development at Argus Media, said during Tuesday’s keynote

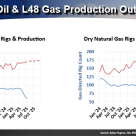

Improvements in drilling rig efficiency have allowed U.S. crude oil and natural gas production to move higher this year even as the overall rig count – which is normally a bellwether of production trends – has moved lower. That trend was discussed as part of the U.S.

The Bakken Shale is being hit especially hard by production cuts this spring. Crude oil-focused producers large and small have been shutting in wells and putting well completions on hold, slashing daily crude output by more than one-sixth. The rig count is down by half in less than two months — to 26, the play’s lowest level since mid-2016 — and thousands of oilfield workers have been let go. All this is happening despite the facts that the Bakken’s four-county core has some of the best shale assets outside the Permian and that in 2017-19 the play was super-hot, with crude production increasing by 50%. That three-year growth spurt spurred the development of a number of new crude gathering systems, many of which now face a period of significant underutilization. Today, we discuss highlights from our new Drill Down report on oil production and supporting infrastructure in the U.S.’s #2 shale play.

Well, it’s happened. The first signs of crude oil and gas production curtailments in the Permian Basin materialized over the weekend. That has followed weeks of extreme oversupply conditions, growing storage constraints and distressed pricing, all to deal with the abrupt and unprecedented loss of refinery demand for crude oil due to COVID, not just along the Gulf Coast, where the lion’s share of the U.S. refineries sit, but also more locally in West Texas. The rapidly shifting supply-demand balance, first from reduced local refining demand and now also the emerging production cuts, is adding volatility to the spreads and flows between the West Texas basin’s regional hub at Midland, and downstream hubs at Cushing and Houston. Today, we look at how the Midland market has responded to the downturn in local refining demand, and how production losses will factor into the balancing act.

With a dwindling market for their crude, many U.S. producers are confronting an unavoidable choice: shutting in existing production. Just go out and flip a switch and turn a valve, right? Wrong. Like everything else in the COVID era, shutting in production is complicated. It is the alternative of last resort for producers, whose primary directive is the economic extraction of oil and gas. But with demand for their products crushed, production from some wells no longer makes economic sense. Unfortunately, the process of shutting in wells is charged with contractual, economic and operational issues that the industry is scrambling to deal with. The situation is fraught with uncertainty, and many producers’ futures depend on how decisively they manage the shut-in process. Today, we discuss the urgent need to reduce oil production and the judgments producers will be making as they take wells offline.

The global economic shut-down caused by COVID continues to wreak havoc on U.S. markets. Last week, the dynamics that resulted in negative prices for NYMEX WTI thrust crude oil, and, more specifically, storage at Cushing, OK, into the national spotlight. The extraordinary imbalance in U.S. crude oil supply and demand has been pushing record volumes of oil into storage at the Cushing crude hub and tankage along the Gulf Coast. The same fundamental factors have also driven a surge in stocks of refined products like gasoline and diesel. Now the questions on everybody’s mind are, how long until storage tanks are completely full and what will that mean? Today, we’ll discuss recent trends and consider what record storage builds mean for the oil patch.

On Monday, front-month WTI at Cushing cratered to a negative $37.63/bbl. On Tuesday, the same futures price rose by nearly $48 to close at about $10/bbl — a positive $10, that is. As for WTI to be delivered in June, it lost well over a third of its value on Tuesday, ending up at less than $12/bbl, but over the past two days it has roared back to over $16/bbl. No doubt the WTI futures market will see more wild times in the days and weeks ahead as traders look to avoid the traps that ensnared the market as the May contract approached expiry. If there’s a lesson to be learned from the past week, it’s that it really helps to understand the ins and outs of the futures market — especially when it is so volatile. Perhaps the most important thing to wrap your head around is that while the futures market mostly involves financial players who will never take physical delivery of oil, the two markets — financial and physical — are fundamentally linked. Prompt-month futures converge on spot prices over time, while physical contracts are settled in part based on NYMEX futures, so producers will feel the sting of Monday’s negative prices when physical April deliveries are invoiced. Today, we begin a two-part blog series examining U.S. spot crude pricing mechanisms.

Underlying Monday’s financially driven oil price rout are physical markets that are in extreme turmoil as they contend with severely reduced demand resulting from the COVID lockdowns and rapidly filling storage tanks. In the Permian Basin, the epicenter of U.S. shale oil, the crude benchmark price — WTI at Midland — on Monday crashed to a historical low of negative $13.13/bbl before rebounding to a positive $13.01/bbl Tuesday. The same day, prices at the Permian natural gas benchmark Waha revisited negative territory for the third time this month, with a settle of minus $4.74/MMBtu for Tuesday’s gas day. Negative supply prices aren’t new to Permian producers, at least for gas — Waha settled as low as minus-$5.75/MMBtu in early April 2019. But up until a couple months ago, oil prices were supportive enough to keep producers drilling regardless. Now, that’s all over, at least for a while. What can we expect now that negative oil prices have arrived in the Permian? Today, we’ll dissect the latest bizarre pricing event to rattle the Permian natural gas and oil markets.

We have now entered the crude oil twilight zone. Never before has crude traded below zero, much less at the absurd level of negative $37.63/bbl. There is no doubt that demand for crude and motor gasoline are far below crude production volumes, leaving the market vastly oversupplied. But could it really be this bad? When you are talking about the market for physical barrels, the answer is “no”. It is bad. Really bad. But what happened yesterday had more to do with the mechanics of futures contracts and how they transition from month to month, than a complete mega-meltdown in physical barrels. That is not to say that negative prices for physical barrels are not already a fact of life in some locations. But negative $37.63/bbl? Something else must be going on. So, to put yesterday’s bizarre market action in perspective, we need to get into a few details on futures contract mechanics, and then look forward to what may be coming over the next few weeks. In today’s blog, we discuss the factors that are driving such extraordinary crude market developments.

In an energy market filled with incalculable uncertainty, it is no surprise that most of the focus is on the short term: production shut-ins, collapsing demand, refinery unit shutdowns, ballooning storage inventories and continually weakening prices. But even in the face of such dire circumstances in the weeks just ahead, there remains a cautious optimism — relatively speaking — for the resumption of some kind of new normal on the other side of COVID. You can see that expectation in the numbers, with the WTI May 2020 contract settling on Friday at $18.27/bbl, but the May 2021 contract up to $35.52/bbl. Granted, that May 2021 price would have been catastrophic if viewed in January 2020, but now it’s a bullish 95% increase over the front month. It is that shift in perspective that underlies the fundamentals content that we developed for our two-day Spring 2020 Virtual School of Energy, held last week in the cloud: how things were viewed BEFORE the meltdown, and how things look AFTER — over the next five years. Did you miss the conference? Not to worry. The entire 14 hours of content are available online in our encore edition. It’s almost like being there! Today’s advertorial blog reviews some of the most important findings we covered at School of Energy and summarizes our overall virtual conference curriculum.

For most of the past three years, Western Canadian producers have had to deal with crude oil pipeline constraints — takeaway-capacity shortfalls serious enough to spur huge price discounts for the region’s benchmark Western Canadian Select (WCS) that are sufficient to support the higher cost of crude-by-rail alternatives. But things are changing, and fast. WCS prices are at or near historic lows — low enough to convince a number of producers to rein in their capital spending and production. Crude-by-rail use is down, and there’s even space available on the usually maxed-out Enbridge Mainline system, the region’s primary pipeline egress. And wouldn’t you know it, just as production is slipping and constraints are easing, real progress is being made on three big pipeline projects that had long been in limbo: the Line 3 Expansion, the Trans Mountain Expansion (TMX) and Keystone XL. Today, we provide an update on Western Canadian crude takeaway capacity and examine whether the region may — irony of ironies — end up with too much.

U.S. crude oil production is off its historic highs, the rig count is in free-fall, and crude inventories are rising fast, with the Cushing-to-Magellan East Houston price differential drawing oil away from the Gulf Coast and to the Oklahoma storage hub. Oh, and global demand for crude is off by more than 20%. None of this bodes well for U.S. crude exports, which have been at or near record levels the past few months. What seems to be shaping up is a fierce competition among the owners of existing export terminals to offer the most efficient, lowest-cost access to the water. Today, we continue our series with a look at Enterprise Products Partners’ Houston-area crude oil storage, pipelines and docks.

The whirlwind of events that has transpired in the past couple of months — namely the coronavirus pandemic and the collapse of the OPEC+ coalition — has not only shaken up the energy markets, but quite literally sent it reeling in the opposite direction than where it was headed just a few months ago. The oil price decline has reverberated through the energy complex, and key indicators that drive industry decisions are veering far off from their recent course, and in many cases, also from historical norms. The world is continuing to change at a rapid pace as the industry navigates the uncertainty. Just yesterday, in an emergency meeting, OPEC announced it had reached a 23-nation agreement to cut a combined 9.7 MMb/d of crude oil production starting May 1, 2020. Today, we highlight some of the biggest moves happening in prices and price relationships in recent days and weeks as the realities of crude oil demand constraints, supply glut and low prices set in.

The crash in global crude oil markets has meant low prices for all producers, but no place more so than in Alberta’s oil sands. Transportation, blending and quality differentials mean that benchmark Western Canadian Select (WCS) is priced at a significant discount to light, sweet West Texas Intermediate. With WTI prices seemingly stuck below $30/bbl, the absolute price of WCS last week tumbled to all-time lows below $5/bbl. If they persist, will WCS prices south of $10/bbl generate wide-scale production shut-ins in the oil sands? Today, we continue our series on the challenges facing Alberta’s oil sands.

Energy markets are changing faster than at any time in history. It’s hard enough just to keep up with what’s happening today, much less try to anticipate what’s ahead on the other side of COVID. But that’s exactly what we’ll be doing next week at RBN’s Virtual School of Energy. More than one-third of the curriculum is a detailed review of RBN’s hot-off-the-presses forecasts for all the essential elements of U.S. crude oil, natural gas and NGL markets, including our freshly updated outlooks for production, infrastructure utilization, exports/imports and demand. Better yet, we’ll put these forecasts in the context of our fundamental analysis and models, so you can not only understand where it looks like we’re headed today, but gain the skills to adjust your outlook on the fly as circumstances change. Although this blog is an advertorial, stick with us if you would like to know more about how the RBN crystal ball works.

Just a few months ago, crude oil producers and marketers were wondering whether there would be enough marine terminal capacity along the Gulf Coast to handle the steadily increasing volumes of crude that would need to be exported over the next few years. Now, with WTI prices hovering around $25/bbl and producers slashing their 2020 drilling plans, expectations of rising U.S. production and exports are out the window. Instead, what may be shaping up is a fierce competition among the owners of existing storage facilities and loading docks to offer the most efficient, lowest-cost access to the water. Today, we continue our series with a look at two large Houston-area facilities: the Houston Fuel Oil Terminal and Seabrook Logistics Marine Terminal.

The collapse in WTI prices in March has been a crushing blow to the Permian, the Bakken and other U.S. shale plays that produce light, sweet crude oil. But as bad as sub-$25/bbl WTI prices are — especially for producers whose balance-of-2020 volumes aren’t at least partly hedged at higher prices — consider the record-low, $5/bbl prices facing oil sands producers up north in Alberta. Western Canadian Select, the energy-rich region’s benchmark heavy-crude blend, fell below $10/bbl more than a week ago, and on Tuesday WCS closed at $5.08/bbl. Producers, who already had been dealing with major takeaway constraints, are ratcheting back their output and planned 2020 capex, and slashing the volumes they send out via rail in tank cars. Today, we begin a short blog series on the latest round of bad news hitting Western Canada’s oil patch.