The global economic shut-down caused by COVID continues to wreak havoc on U.S. markets. Last week, the dynamics that resulted in negative prices for NYMEX WTI thrust crude oil, and, more specifically, storage at Cushing, OK, into the national spotlight. The extraordinary imbalance in U.S. crude oil supply and demand has been pushing record volumes of oil into storage at the Cushing crude hub and tankage along the Gulf Coast. The same fundamental factors have also driven a surge in stocks of refined products like gasoline and diesel. Now the questions on everybody’s mind are, how long until storage tanks are completely full and what will that mean? Today, we’ll discuss recent trends and consider what record storage builds mean for the oil patch.

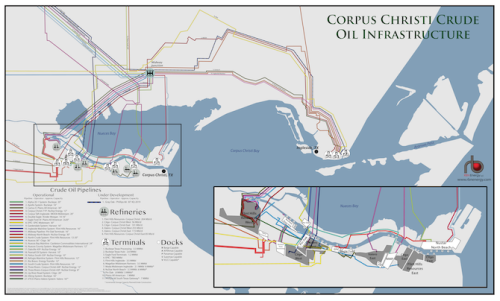

Gain insight and clarity into one of the United States’ most strategic Crude Oil Export Markets with RBN Energy’s Corpus Christi Crude Oil Infrastructure wall map.

For the week ended April 24, the Energy Information Administration (EIA) reported a total U.S. storage build of 9 MMbbl. That followed a 15-MMbbl build the week ended April 17, and a 19-MMbbl build the week before that. Over the past five weeks, crude storage levels in the U.S. have increased by 72 MMbbl, or an average of 2.1 MMb/d. To put that in perspective, the previous high storage build, according to EIA statistics, which date back to 1982, was 14 MMbbl in a week, or 2 MMb/d. The numbers for Cushing, the nation’s largest commercial storage hub for crude, have been similarly alarming, with the volume of crude going to storage the past five weeks averaging 4.8 MMbbl per week, or 700 Mb/d. But of the last five weeks’ 72 MMbbl of storage build, Cushing only accounted for one-third of the total U.S. Over half entered storage in PADD 3 — the Gulf Coast region — which has seen crude inventories increase by an average of 7.8 MMbbl per week, or 1.1 MMb/d, for the last several weeks. And it’s not just crude; stocks of transportation fuels have also seen a sharp uptick recently.

Let’s start this discussion by considering the dynamics of why storage has seen such dramatic increases. The short answer is that supply and demand are out of whack — way out of whack. Assessing the U.S. supply-demand balance is relatively straightforward. Supply equals production plus imports. As shown in the left column in Figure 1, U.S. production (green bar segment) as of April 24 stood at 12.1 MMb/d and imports (blue segment) averaged 5.3 MMb/d, for total supply of 17.4 MMb/d. Demand, in turn, equals refinery consumption plus exports. On the demand side, exports of 3.3 MMb/d (purple segment) and refinery runs of 12.8 MMb/d (orange area) couldn’t balance the market, so the remaining 1.3 MMb/d was shoved into storage. Over seven days, that 1.3 MMb/d gives us a weekly storage build of 9 MMbbl. Using that logic, if we then do a linear extrapolation of the average build rate for the last five weeks (dashed red line in right graph), 14.5 MMb/week from the ending stock balance on April 24 of 528 MMbbl to the EIA estimate of total working storage capacity of 653 MMbbl, total U.S. storage would be filled by mid-June. (For weekly updates on the balance, check out our Crude Gusher.)

About the song

"How Much More Can I Take" was written by Ian Hunter, and appears as the 12th cut on Ian Hunter's seventh solo album, Yui Orta. The title, Yui Orta, was a play on the Three Stooges phrase, "Why you … I ought to ..." On this album, Hunter reunites with longtime collaborator Mick Ronson, and shares the album billing as the Hunter/Ronson Band. The LP was recorded in the summer and fall of 1989 at the Power Station in New York City, with Bernard Edwards producing. Hunter was dropped from his label, Mercury Records, shortly after the album's release in November 1989. With basically zero support from Mercury Records, the album only went to #57 on the Billboard Top 200 Albums chart. Personnel on the record were: Ian Hunter (lead, backing vocals, piano), Mick Ronson (guitars, backing vocals), Pat Kilbride (bass), Mickey Curry (drums) and Tommy Mandel (keyboards).

Ian Hunter is an English singer-songwriter best known as the lead singer for the English rock band Mott the Hoople from its inception in 1969 to its dissolution in 1974, and for his solo career. Hunter released nine studio albums, one live album and three singles with Mott the Hoople. He has released 19 studio albums, two live albums and 25 singles as a solo artist. Hunter still records and occasionally tours, but at the age of 80 — and suffering from an acute case of tinnitus — his future touring plans are unsure at this moment.

Mick Ronson was an English guitarist, songwriter, arranger and record producer. He first came to prominence as David Bowie's lead guitarist as one of the Spiders from Mars. He went on to play with Ian Hunter, Lou Reed, Van Morrison, Bob Dylan, Morrisey and others. As a solo artist, Ronson made five studio albums, two live albums and five singles. With David Bowie, he appeared on six studio albums and two live albums. With Ian Hunter, Ronson appeared on five studio albums and one live album. Ronson was featured in a 2017 biographical documentary film entitled, Beside Bowie: The Mick Ronson Story. Ronson died of liver cancer in London in April 1993 at the age of 46.