The fact is, many major E&P acquisitions include at least some production assets that don’t align with the acquiring company’s long-term strategic plans. Also, it’s often true that big-dollar M&A increases the buyer’s debt level — and it’s typical in such cases that the company commits to quickly reducing its debt through the divestiture of non-core assets. As we discuss in today’s RBN blog, there’s a lot of that going on now, and in many cases smaller, private-equity-backed producers are scooping up the acreage and production being sold.

Through the first half of the 2020s there’s been a frenzy of upstream M&A activity in the U.S., with a good number of deals valued in the billions or even tens of billions of dollars. Earlier this week, for example, Crescent Energy announced plans to acquire Permian producer Vital Energy for $3.1 billion in stock. Just over a year ago, Crescent closed on the $2.1 billion, stock-and-cash purchase of SilverBow Resources, a leading E&P in the Eagle Ford, and in January, Crescent bought more Eagle Ford acreage and production from Ridgemar Energy for $905 million. (More on Crescent in a moment.)

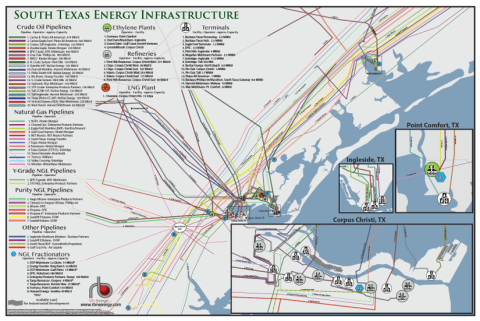

RBN Energy’s South Texas Energy Infrastructure Map brings together all the pieces of the critical and complex puzzle of the greater Corpus Christi region. Spanning from Point Comfort, TX to Corpus Christ, TX and south of the Agua Dulce natural gas hub, the map details the processing, transportation and export facilities in RBN Energy’s classic clear, concise and easy to comprehend style.

Or consider Pioneer Natural Resources, which followed up several years of mostly organic growth with the 2021 purchases of Parsley Energy (for $7.6 billion) and DoublePoint Energy (for $6.5 billion; see Buy Buy Buy for more on the deals), only to be gobbled up by an even bigger fish, ExxonMobil, in May 2024 for a cool $64.5 billion (including the assumption of Pioneer debt). Since then, ExxonMobil has worked to reduce its debt, in part through (you guessed it!) the sale of non-core assets.

ConocoPhillips

The same has been happening at ConocoPhillips, which made headlines last year with its $22.5 billion acquisition of Marathon Oil. As we discussed in Everybody Dance Now, the real gems in the deal for ConocoPhillips were Marathon’s highly complementary production assets in the Eagle Ford, the Bakken, and the Permian’s Delaware Basin. The transaction also gave ConocoPhillips the greater scale it needed to compete with the likes of ExxonMobil and appeared to be the best option for Marathon, which was probably too small to be a major acquirer.

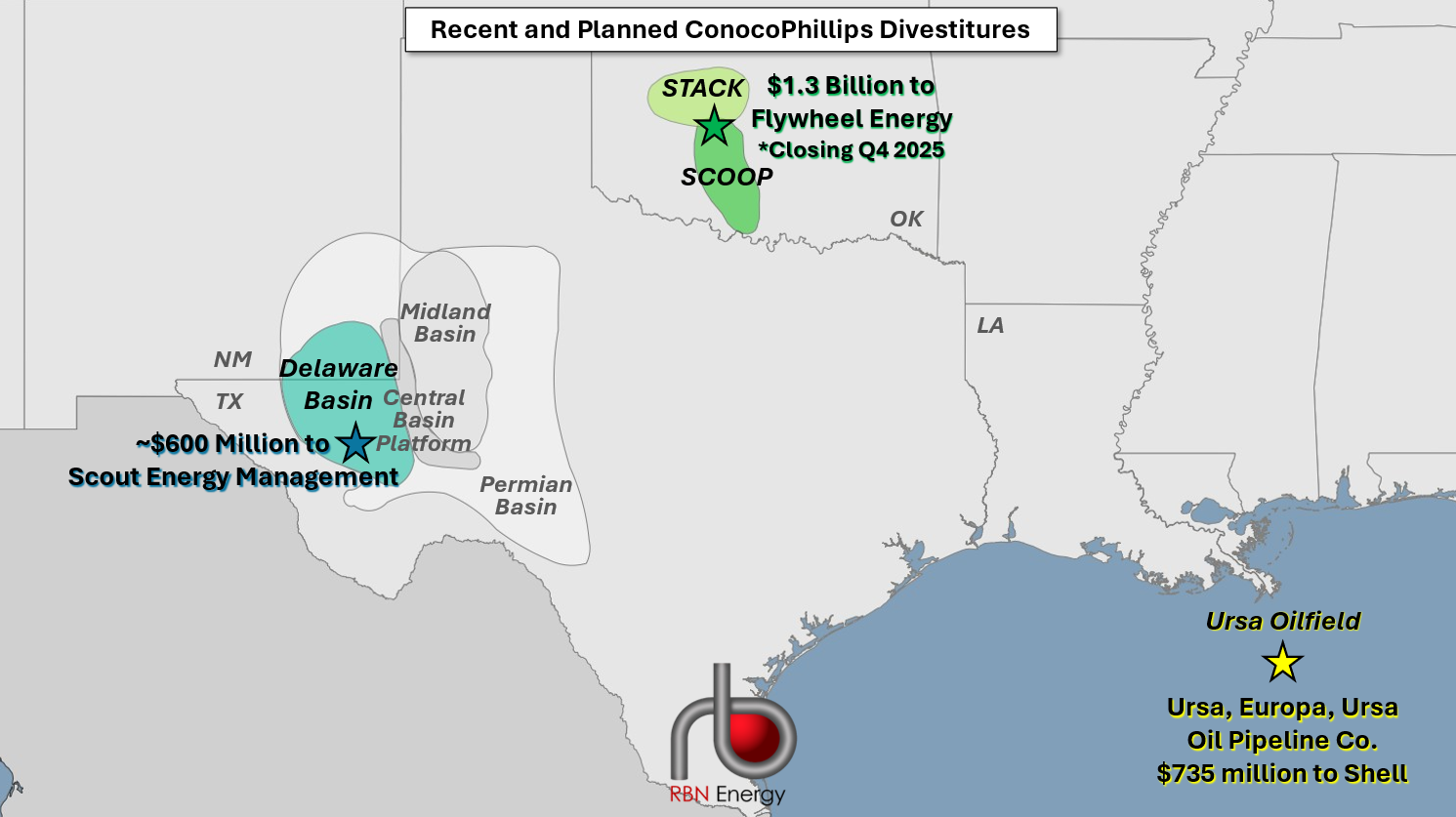

Marathon also came with something ConocoPhillips didn’t see fitting into its long-term strategy: about 300,000 net acres in the Anadarko, more specifically natural-gas-focused assets in the SCOOP/STACK play in Oklahoma that have been producing about 40 Mboe/d in recent months — one-quarter of that (or about 10 Mb/d) in the form of crude oil. ConocoPhillips announced August 7 that it has reached an agreement to sell those assets (green star in Figure 1 below) to an undisclosed buyer for $1.3 billion. According to published reports, the purchaser is Flywheel Energy, a privately held, Oklahoma City-based E&P backed primarily by energy-sector investor Stone Ridge Energy. The deal is expected to close in Q4 2025.

Figure 1. Recent and Planned ConocoPhillips Divestitures. Source: RBN

About the song

“We Are Never Ever Getting Back Together” was written by Taylor Swift, Max Martin and Shellback. It appears as the eighth song on Taylor Swift’s fourth studio album, Red. The up-tempo pop song is about frustration with an ex-lover who wants to reunite their romantic relationship. Released as the first single from the album in August 2012, it went to #1 on the Billboard Hot 100 Singles chart and Hot Country Songs Singles chart. It won a Billboard Music Award for Top Country Song and has been certified 6X Platinum by the Recording Industry Association of America (RIAA). Personnel on the record were: Taylor Swift (lead, backing vocals), Max Martin (keyboards) and Shellback (guitar, bass, keyboards, programming).

Red is Taylor Swift’s fourth studio album. It was recorded in 2011-12 at Blackbird Studio and Pain in the Art Studio in Nashville; Ballroom West in New York City; Instrument Landing in Minneapolis; Conway Studio, Village Recording Studio and The Garage in Los Angeles; and Ruby Red in Atlanta. Produced by Taylor Swift, Nathan Chapman, Jeff Bhasker, Dann Huff, Jacknife Lee, Max Martin, Shellback, Butch Walker and Dan Wilson, the album was released in October 2012. It went to #1 on the Billboard 200 Albums chart and has been certified 7X Platinum by the RIAA. Seven singles were released from the LP.

Taylor Swift is an American singer, songwriter and record producer. She is known for her autobiographical songwriting and is one of the best-selling music artists of all time — and the first billionaire female musician. Swift has released 11 studio albums, four live albums, four re-recorded albums, 32 compilation albums, five EPs and 61 singles and has sold over 300 million records worldwide. She has appeared in five motion pictures and has been featured in four documentaries. Swift has won eight ACM Awards, 40 American Music Awards, two Brit Awards, 49 Billboard Music Awards, 12 CMA Awards, an Emmy Award, and 14 Grammy Awards. She continues to record and tour, and recently announced that her upcoming 12th studio album, The Life of a Showgirl, will drop in October. Swift announced the release of two one-time-only limited pressings of the LP in violet and wintergreen/onyx vinyl on her web store, and they sold out within an hour.