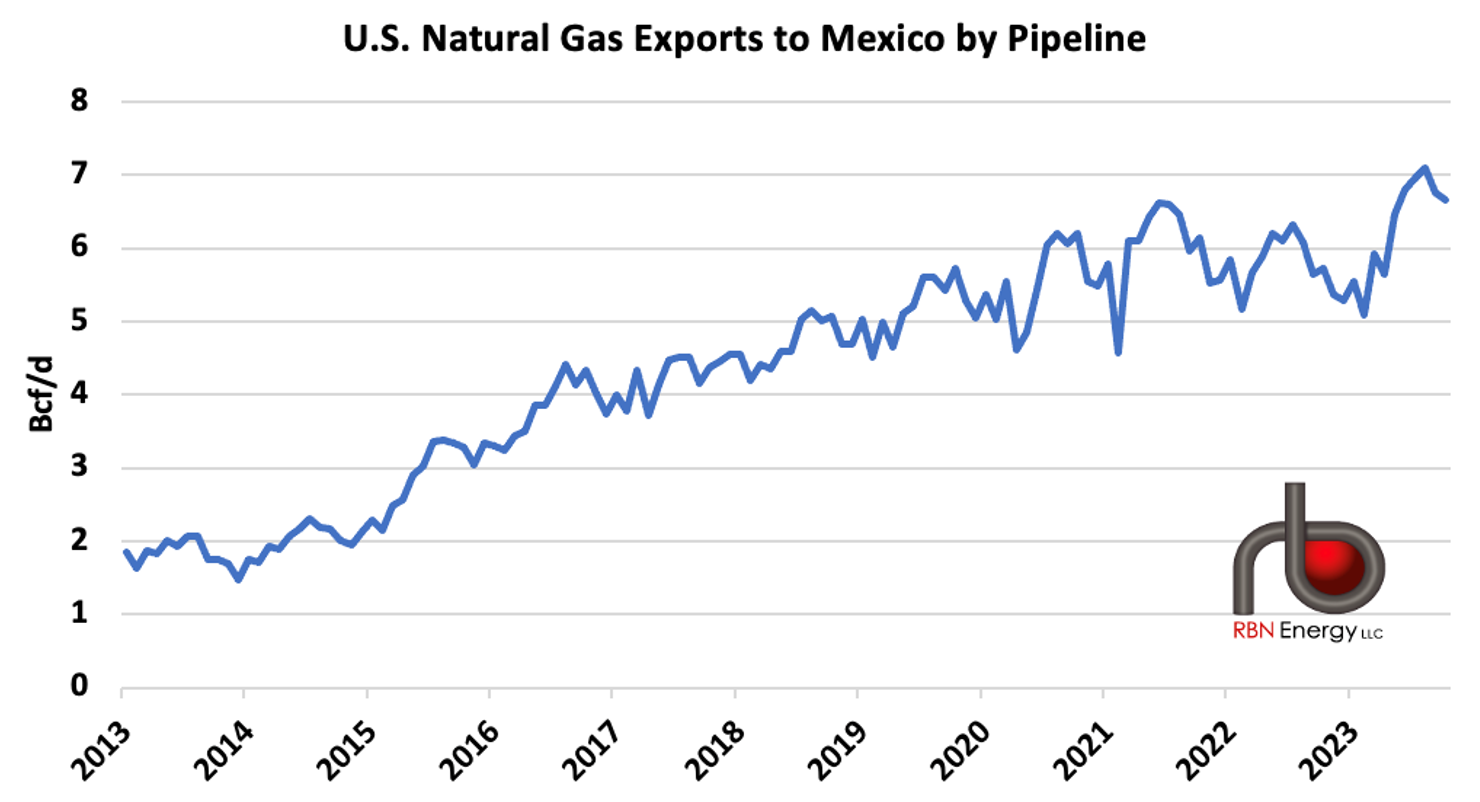

With all the talk about U.S. LNG exports and plans for more LNG export capacity, it can be easy to forget that more than 6 Bcf/d of U.S. natural gas — mostly from the Permian and the Eagle Ford — is being piped to Mexico. That’s more than 3X the volumes that were being piped south of the border 10 years ago, a tripling made possible by the buildout of new pipelines from the Agua Dulce and Waha hubs to the Rio Grande and, from there, new pipes within Mexico. And where is all that gas headed? Mostly to new gas-fired power plants and industrial facilities — a handful of new LNG export terminals being planned on that side of the border will only add to the demand. In today’s RBN blog, we discuss the ever-increasing flows of gas to Mexico and the tens of billions of dollars of new infrastructure making it all possible.

The RBN NATGAS Haynesville is a weekly natural gas fundamentals analysis focused on supply, flow, and LNG-driven demand dynamics within the Haynesville basin.

Back in 2013, in the very early days of the RBN blogosphere, we discussed what we saw as the growing gap between Mexico’s fast-growing need for natural gas and the country’s declining gas production. Man, were we onto something! Since then, Mexico’s Comisión Federal de Electricidad (CFE) has developed a massive fleet of gas-fired combined-cycle plants and helped to underwrite the buildout of a far-reaching network of gas pipelines from South Texas and West Texas into and through Mexico. Over the same 10-year period, Mexico’s gas production has declined by one-third, to about 4 Bcf/d, and only 1 Bcf/d of the gas produced there is actually sold into the domestic market — of the other 3 Bcf/d, 2 Bcf/d is used internally by Petróleos Mexicános (Pemex) for its production and refining operations and 1 Bcf/d is unusable because of its high nitrogen content (an issue also increasingly rearing its ugly head up here in the states lately — see It’s a Gas Gas Gas).

Figure 1. U.S. Natural Gas Exports to Mexico by Pipeline. Source: EIA

About the song

“Down into Mexico” was written by Delbert McClinton, Bob DiPiero, and Gary Nicholson and appears as the eighth song on Delbert McClinton’s 23rd studio album, Cost of Living. The song, delivered in McClinton’s unique Texas blues style, tells a tale of misadventure gone wrong with an unfortunate ending down in Mexico. Personnel on the record were: Delbert McClinton (vocals), Rob McNelly (acoustic, electric guitars, solos), Gary Nicholson (acoustic guitar), Spencer Campbell (bass), Kevin McKendree (organ), and Lynn Williams (drums).

Cost of Living was recorded between March 2004 and February 2005 at Fearless Recording and The Sound Emporium in Nashville, with Delbert McClinton and Gary Nicholson producing. Released in August 2005, the album went to #1 on the Billboard Top Blues Albums chart, #14 on the Billboard Top Country Albums chart, and #105 on the Billboard 200 Albums charts. The album won a Grammy Award for Best Contemporary Blues Album at the 48th Annual Grammy Awards. Two singles were released from the LP.

Delbert McClinton is an American singer, songwriter, and musician from Fort Worth. His professional career started in 1961 when he played harmonica on Bruce Channel’s #1 hit record, “Hey Baby.” In 1962, while on tour in the U.K. with Channel, McClinton taught a member of a pop group on the tour with them named John Lennon how to play blues harmonica. He has released 27 studio albums, three live albums, 12 compilation albums, and 17 singles. He has won four Grammy Awards. McClinton continues to record and tour.