Since the mid-2010s, Mexico’s Comisión Federal de Electricidad (CFE) has developed a massive fleet of natural-gas-fired combined-cycle plants and helped to underwrite the buildout of a far-reaching network of gas pipelines from South Texas and West Texas into and through much of Mexico. Now, there’s a big push to extend that network southeast through the Yucatán Peninsula to serve new power plants and industrial facilities there. The question is, with the vast majority of the pipeline capacity down Mexico’s East Coast already locked up, where will the Yucatán’s incremental gas come from? In today’s RBN blog, we discuss this potential disconnect between Mexico’s gas-related aspirations and reality.

Build your energy market expertise at the 20th School of Energy: Foundations.

Learn from RBN experts, participate in hands-on Excel modeling, connect with industry peers, and gain a stronger understanding of today's interconnected energy markets.

September 9-10 | Houston, TX

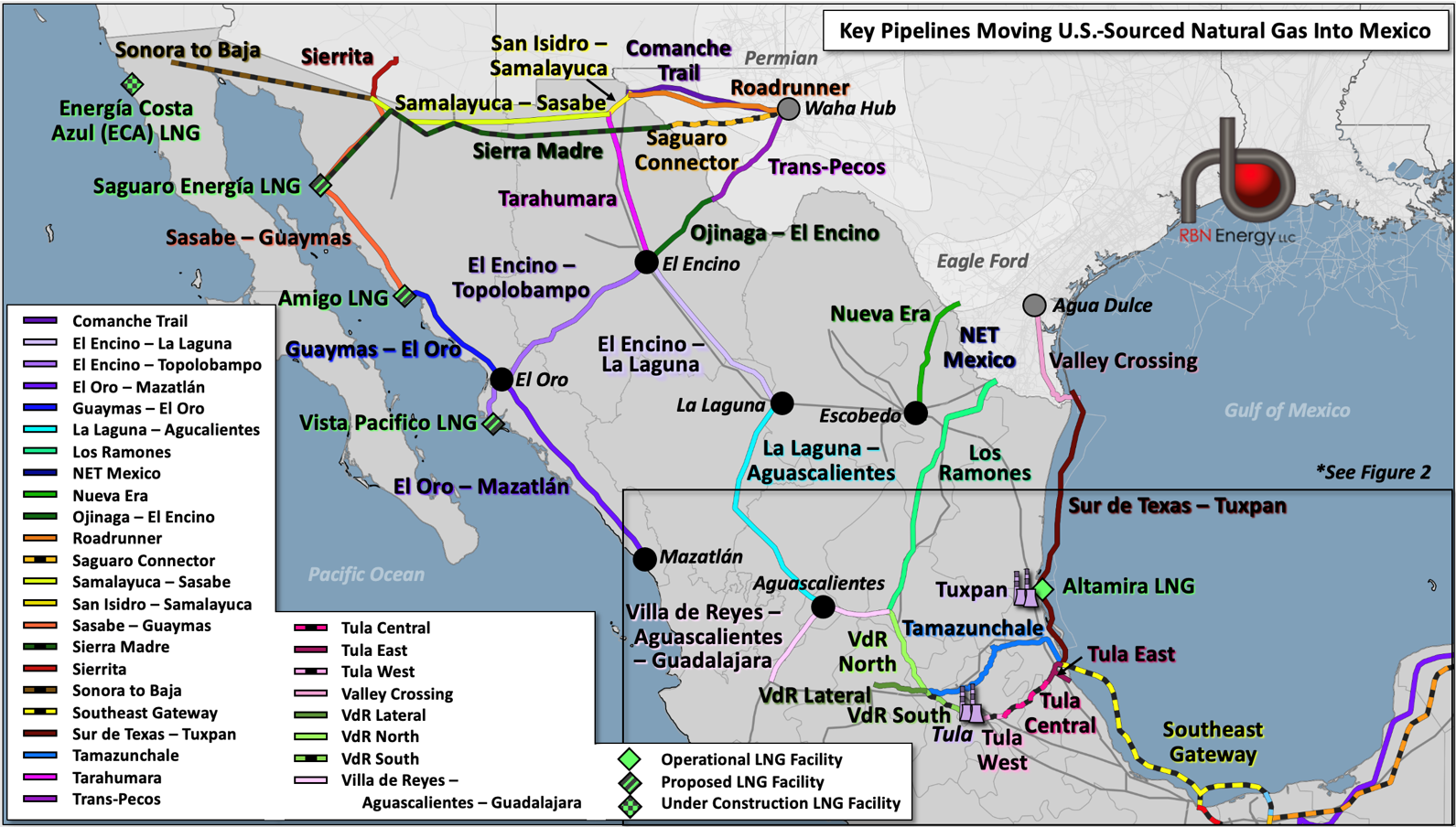

Last month, in Down in Mexico, we discussed the steady rise in U.S. natural gas exports to Mexico and the new, south-of-the-border pipelines, power plants and industrial projects that have been making those gains possible. As we said in that blog, pipeline exports to Mexico — mostly from the Permian and Eagle Ford production areas — now top 6 Bcf/d, and still-higher export volumes are likely as new pipelines, power plants, industrial facilities and LNG export terminals come online (a subject we’ll also be covering in our upcoming webcast). We also noted that there are three primary corridors for U.S.-to-Mexico gas totaling more than 11 Bcf/d:

- A 3.3-Bcf/d corridor that runs west/southwest from the Waha Hub (gray dot in top-center of Figure 1) through a number of pipelines that reach into north-central, western and central Mexico.

- A nearly 1-Bcf/d pathway that runs south from the Agua Dulce Hub (gray dot in center-right) and Eagle Ford production areas to interior (i.e., non-coastal) markets in eastern Mexico.

- A 7-Bcf/d-plus corridor that also runs south from Agua Dulce, but further east. (More on this in a moment.)

Finally, we pointed out what you might call an inconvenient truth for Mexico, namely that while the country has become increasingly dependent on natural gas, its domestic production has been close to flat, with only about 1 Bcf/d of production from Petróleos Mexicanos (Pemex) — the state-owned oil and gas producer and refiner — generally sold into the Mexican market. Of the other 3 Bcf/d of Pemex gas production, about 2 Bcf/d is used internally for its production and refining operations and 1 Bcf/d is unusable because of its high nitrogen content. (That’s also an issue up here in the States lately — see It’s a Gas Gas Gas.)

Figure 1. Key Pipelines Moving U.S.-Sourced Natural Gas into Mexico. Source: RBN

About the song

“Ahead of Ourselves” was written by Trent Reznor and Atticus Ross. It appears as the second song on Nine Inch Nails’ ninth studio album, Bad Witch. The band debuted the song live at a show in June 2018 at The Joint in Las Vegas — it was the only song from Bad Witch that was performed live before the album’s release. It is thought that the line, “celebration of ignorance,” came from astronomer Carl Sagan’s book, The Demon-Haunted World. Personnel on the record were: Trent Reznor (vocals, production, programming, saxophone), and Atticus Ross (production, programming).

Bad Witch was recorded in early 2018 and released in June 2018. It went to #2 on the Billboard Top Alternative and Top Rock Albums charts, and #12 on the Billboard 200 Albums chart. The record was influenced by David Bowie’s final LP, Blackstar. Reznor had collaborated with Bowie in the 1990s. It was the last in a trilogy of releases, following Nine Inch Nails’ previous two EPs. One single, “God Break Down the Door,” was released from the LP.

Nine Inch Nails (NIN) is an American industrial rock band formed in Cleveland in 1988 by singer, multi-instrumentalist and producer Trent Reznor. Sixteen members have passed through the group since its formation. Reznor was the only permanent member of the group until the addition of Atticus Ross in 2016. They have released 11 studio albums, one live album, one soundtrack album, six EPs, and 19 singles. NIN has sold more than 20 million albums worldwide. The band has won two Academy Awards, one Emmy Award, one Golden Globe Award, and two Grammy Awards. They were inducted into the Rock and Roll Hall of Fame in 2020. Reznor and Ross continue to record and tour with Nine Inch Nails. The duo is also actively involved in scoring motion pictures and television shows, to which they have devoted much of their time over the last few years.

Comments

Which U.S. MLP pipelines will be the big benefactors of increased NG shipments to Mexico??