The production of natural gas liquids (NGLs) increased twice as quickly as expected just two years ago in 2011. Current production of 3.2 MMb/d (gas plants + refineries) was only supposed to be achieved in 2016 and now the forecast is for 4 MMb/d by then. The result has been more rapid implementation of infrastructure to handle NGLs and that supply has exceeded demand so that exports are required. Today we look at the impact of the rapid production ramp up.

This is Episode 4 in a series based on Rusty’s keynote presentation at Benposium on May 14, 2013 titled “Why What We Thought We Knew About the North American Hydrocarbon Market No Longer Matters”. Despite the complicated title, it boiled down to a simple premise. If we look back to see what folk were forecasting for North American energy markets two years ago in 2011 and then compare that to today’s actual data and forecast, what would that tell us about the changing pace of North American energy production?

Looking at the data from Bentek – produced as always at the time in good faith based on what the market was telling them – we see that the scale of change going on in North American energy production exceeded everyone’s expectations. We looked at crude oil production forecasts in the Williston Basin and the Eagle Ford, the natural gas production forecast in the Marcellus and the US NGL production forecast from Bentek around the time of the June 2011 Benposium. What we found was that in every case – crude oil, natural gas and NGLs - today’s forecast numbers for what we expect by 2016 are way higher than they were back in 2011. In the first episode in the series (see Too Wrong for Too Long? – How 2011 Bakken Crude Forecasts Compare to Today) we looked at surging crude production in the Bakken. We learned how production surpassed earlier forecasts because rail transport options allowed producers to bypass the queue for pipeline takeaway capacity that might otherwise have slowed them down. In the second episode in the series we looked at how rapid growth in the Marcellus natural gas production forecast is going to have dramatic consequences for traditional natural gas flows into the northeast in the coming years (see How Marcellus Forecasts Changed the World Sooner Than We Thought). Episode 3 looked at how the Eagle Ford crude and condensate production forecast nearly doubled in just two years. Along the way a lot more of that crude production turned out to be condensate than anyone had guessed or planned for (see Too Wrong for Too Long – The Eagle Ford Crude Condensate Challenge).

Today we continue this series reflecting on the speed of change that shale production is dictating by looking at the consequences of increasing NGL supply.

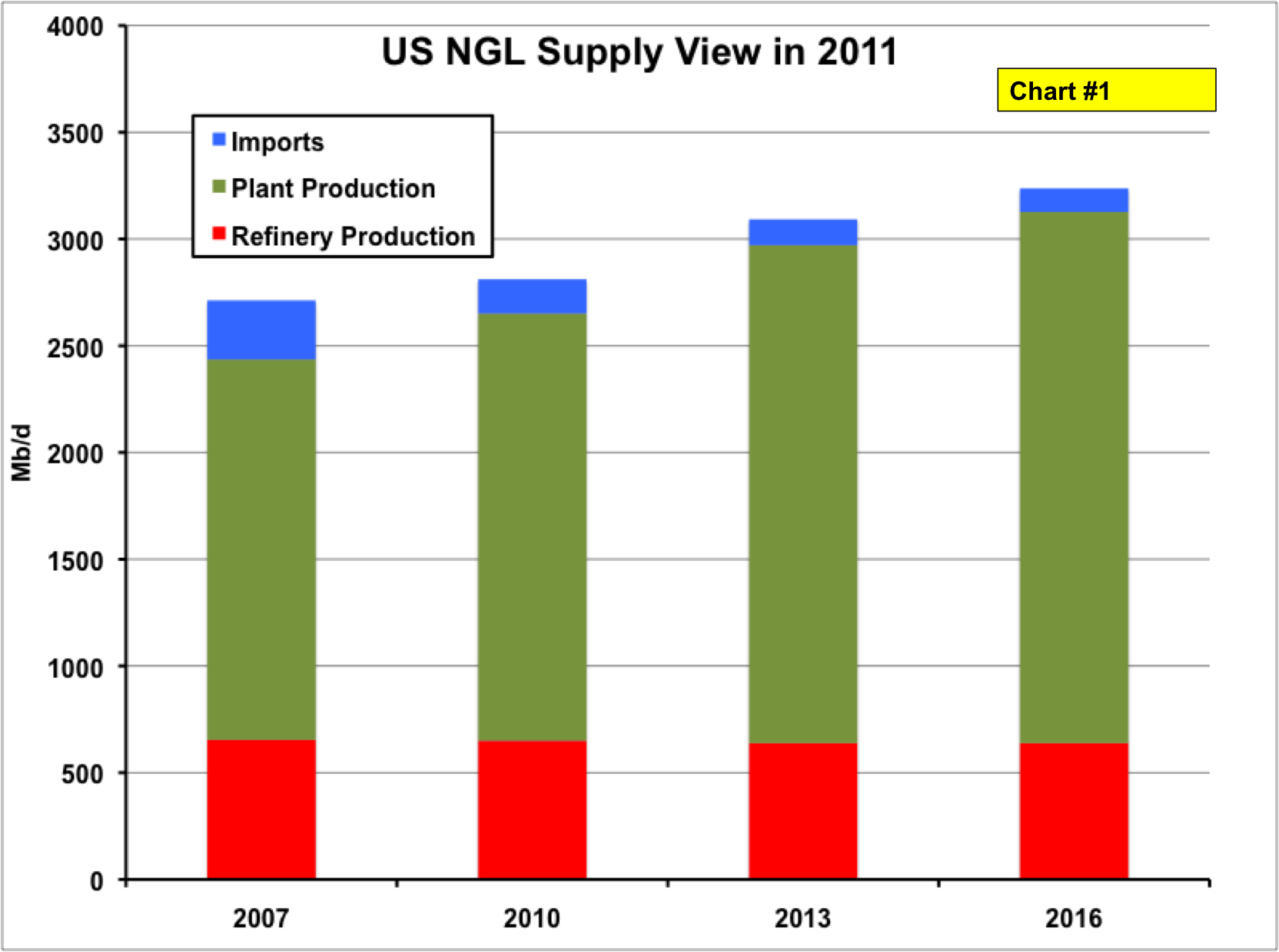

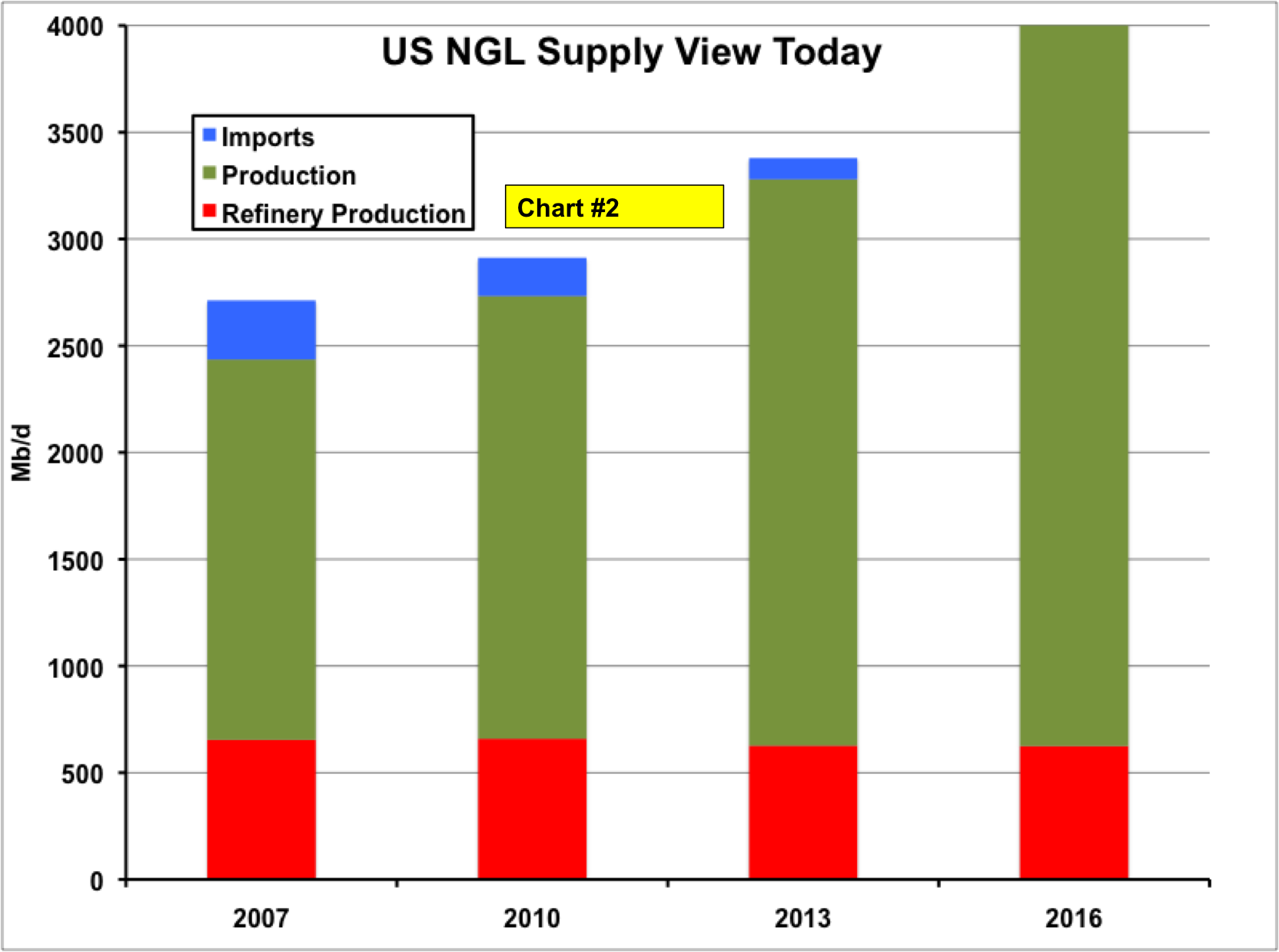

Back in 2011, the Bentek view was that total NGL supply from US natural gas processing plants, refineries and imports would increase from just over 2.7 Mb/d in 2007 up to 3.2 Mb/d by 2016 (see Chart #1 below). Over that period refinery production would be flat and imports would decline. All the growth would be in plant production of NGLs (green color in the chart columns). In a pattern that has become familiar throughout this mini retrospective series, we actually reached the 2016 forecast NGL supply three years earlier than forecast in 2013. The most recent numbers from the Energy Information Administration (EIA) show supply at 3.5 Mb/d today and that number is now projected to increase to 4 Mb/d by 2016 (see Chart #2 below). Once again refinery production stays flat in the forecast and imports decline to zero by 2016. And growth continues to come from increased plant production fed in no small part by the migration of natural gas drilling away from dry gas plays towards wet gas production in response to lower natural gas prices (see for example Can Mont Belvieu Handle the NGL Supply Surge?).

Source: RBN Presentation at Benposium, May 2013

Source: RBN Presentation at Benposium, May 2013

There are several consequences of this rapidly increasing NGL plant production – the most important being that supply exceeds demand – which means first that imports are no longer needed and also that increasing volumes of NGLs will be exported from the US over the next 5 years to balance demand.

Propane and butane exports have been getting the most attention lately (we covered growing propane export plans back in November 2012 (see Exports Prescribed for Propane Relief) and more recently in March 2013 (see Come on Move Your Propane – Do The Conga). These export volumes are forecast by Bentek to increase from about 300 Mb/d today up to 600 Mb/d by 2018 (see Chart #3 below). Propane and butane exports will not only be headed to Latin America, where most of the volume is going today, but also increasingly to the Far East, especially when the Panama Canal expansion gets finished that will allow larger shipments (expected to be 2015 – see Panama Tailored to Fit Larger Vessels). Most of these volumes to begin with will be propane from several developing terminals on the Gulf and East Coasts. Enterprise Product Partners L.P. is currently the largest Gulf Coast export dock operator – they just completed an initial expansion of their facility operated with Oil Tanking on the Houston Ship Channel to 225 Mb/d with another 75 Mb/d expansion planned for 2015. Targa Resources is the other Gulf Coast export terminal operator and their expansion to 130 Mb/d is scheduled for completion in the fall. Energy Transfer Partners Sunoco is also expanding their east coast export facility at Marcus Hook (see Big Surge Comes to Whoville). And another half dozen additional export projects have been announced for the Gulf Coast, which if even half of them get built, will be more than enough capacity to get surplus propane barrels onto the water.

Comments

In Rusty's article 10/22/2012, "Fifty Shades of Condensates" - Which One Did You Mean ?" He defines lease condensate as having an API Gravity ranging between 45 to 75 degrees. Sandy Fielden in the 6/102013 posting defines condensate at the wellhead as having an API between 550 and 80 degrees !! Who is right and who is wrong here ?

In reply to Your definition of condensate and Rusty's don't agree by Pete Kinsella

The truth is that there are no right and wrong answers to this question - the standard by which the industry measures condensate is a moving target. The latest Turner Mason Crude Market Outlook referes to condensate as having an API of 55 degrees and above. That is just one definition. The blog written by Al Troner in July gives a comprehensive review of condensate definitions (see Through The Looking Glass).