Two years ago in June 2011 Bentek forecast that crude production in the Williston Basin would grow to 900 Mb/d by 2016. Today’s production in North Dakota and Montana is already at that level. What we are learning about US shale production is that it has been growing at twice the rate of every forecast out there. Today we begin a new series looking at what we are learning about the accelerating pace of North American shale production.

This week several members of the RBN Energy team attended the best energy fundamentals conference in the business - Bentek’s annual Benposium in Houston. They covered all the North American energy markets in detail including updated forecasts of hydrocarbon production and the latest midstream infrastructure developments. Bentek also provide supply demand forecasts for crude, natural gas and natural gas liquids (NGLs).

Rusty gave the keynote presentation on Tuesday (May 14, 2013) titled “Why What We Thought We Knew About the North American Hydrocarbon Market No Longer Matters”. Despite the complicated title, it boiled down to a simple premise. If we look back to see what folk were forecasting for North American energy markets two years ago in 2011 and then compare that to today’s actual data and forecast, what would that tell us about the changing pace of North American energy production?

Looking at the data from Bentek – produced as always at the time in good faith based on what the market was telling them – we see that the scale of change going on in North American energy production exceeded everyone’s expectations. We looked at crude oil production forecasts in the Williston Basin and the Eagle Ford, the natural gas production forecast in the Marcellus and the US NGL production forecast from Bentek around the time of the June 2011 Benposium. What we found was that in every case – crude oil, natural gas and NGLs - today’s forecast numbers for what we expect by 2016 are at least double what they were back in 2011.

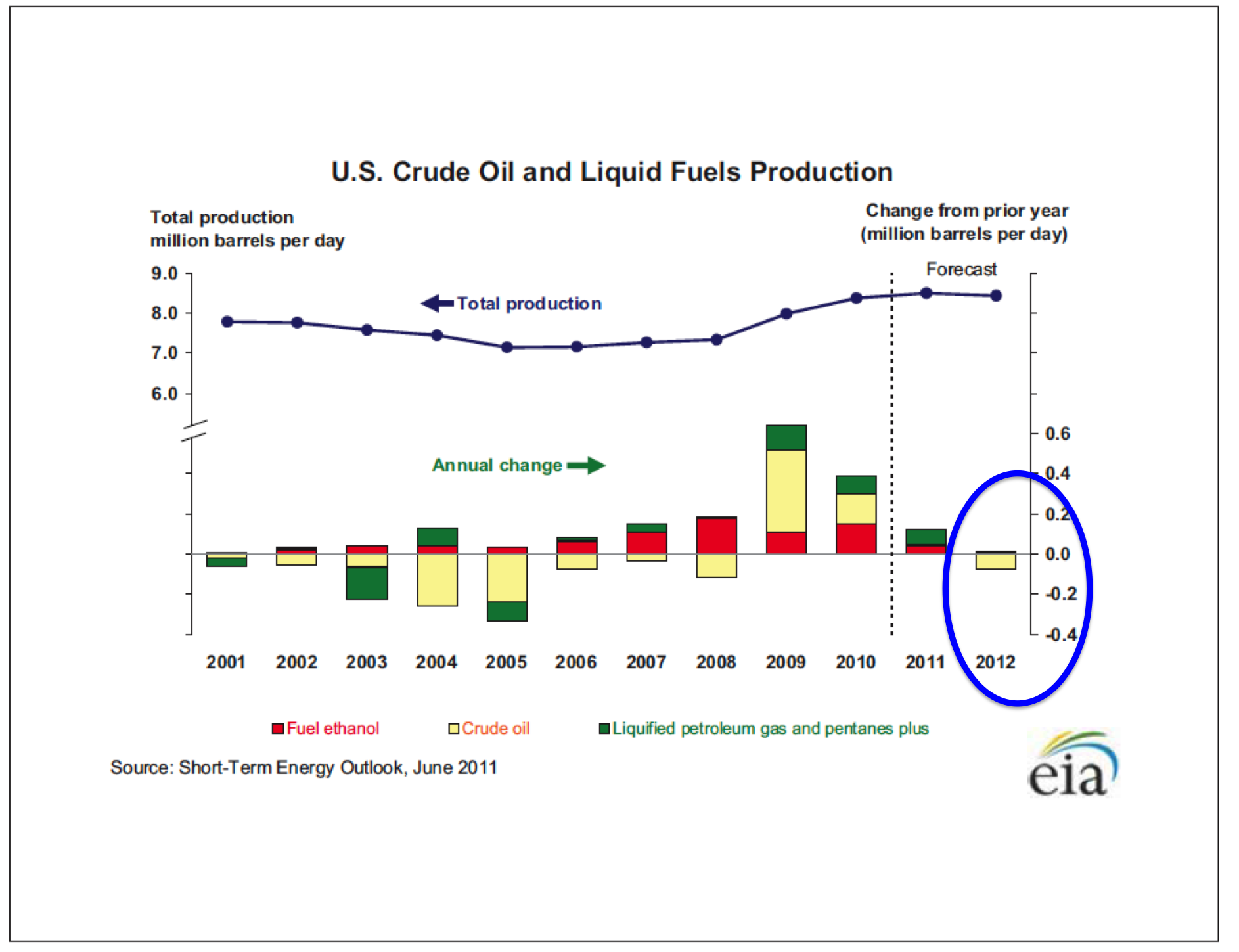

As you can imagine, looking back at old forecasts is not a popular game among consultants to the industry – or for that matter anyone who makes predictions for a living. While researching this blog it didn’t take us long to find the chart below for example from the Energy Information Administration’s (EIA) short-term economic outlook back in June 2011. This was the EIA forecast for US crude oil production for 2012 at the time (green circle). They were predicting that US crude oil production in 2012 would fall by 100 Mb/d. As it turned out, US crude oil production increased by nearly 1.1 MMb/d during 2012. Oops!

Source: EIA

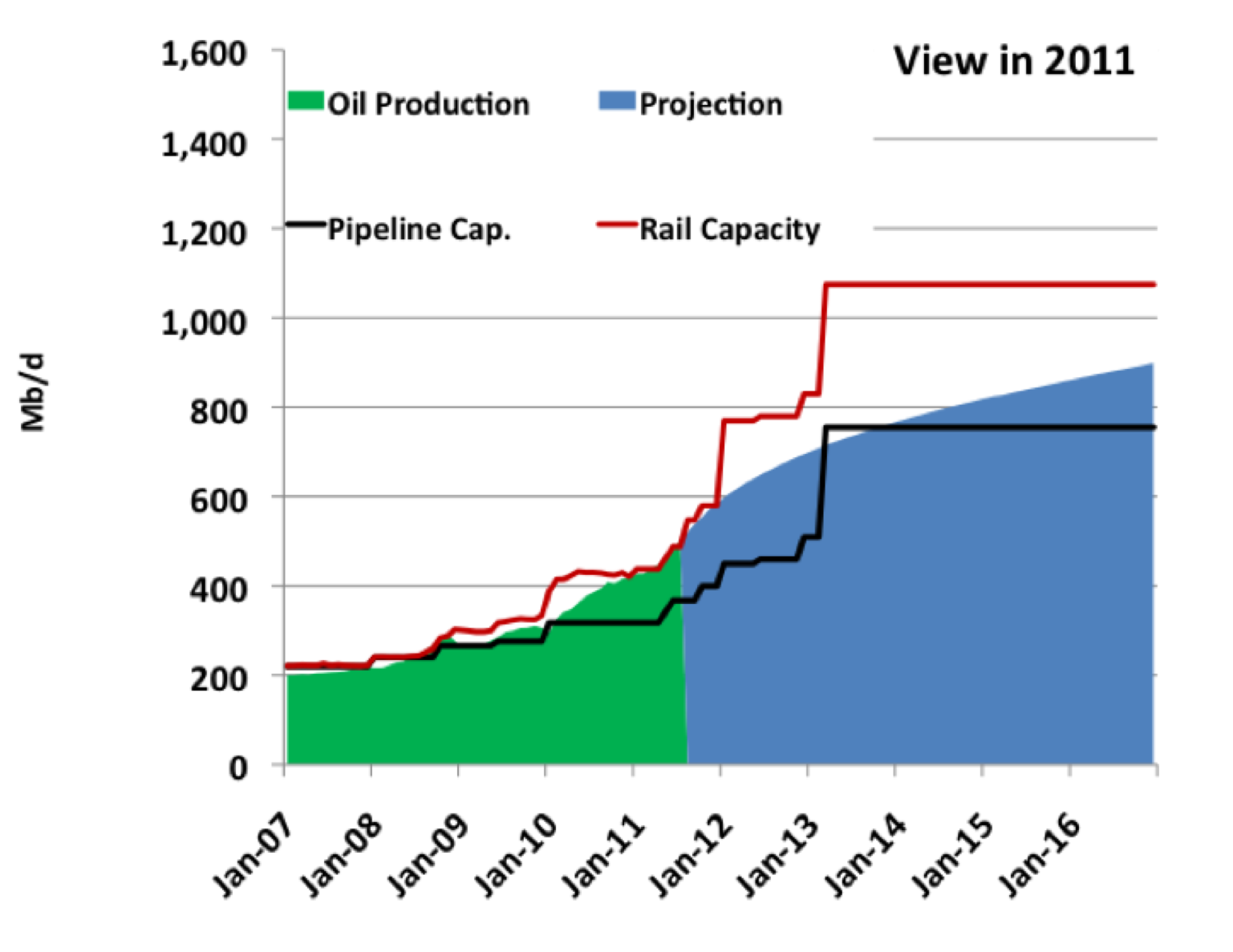

We start our journey back in time with a look at crude oil production in the Williston Basin of North Dakota and Montana. The chart below shows the Bentek forecast in June 2011 for crude production. As you can see, actual crude production numbers were available for April 2011 (green shaded area) and they had reached around 500 Mb/d – up from 200 Mb/d back in 2007. Production had more than doubled in the space of just over two years. Back then the forecast (blue shaded area) was for production to increase to about 900 Mb/d by the end of 2016.

By June of 2011 crude production already exceeded pipeline takeaway capacity from the Bakken (black line on the chart). New planned pipeline capacity coming online was not expected to relieve that constraint until early 2013. As a result, producers like EOG has already begun to move crude oil to market by rail at the end of 2010 and during 2011 crude-by-rail takeaway capacity (red line on the chart) grew to 120 Mb/d. Midstream companies had realized that rail was potentially a good short term solution to the Bakken takeaway problem and by mid 2011 plans were in existence to increase rail takeaway capacity by 300 Mb/d during 2012 to handle the forecast increase in production.

Source: RBN Energy Benposium Presentation 2013

Already by 2011 increasing Bakken and Canadian production were building a crude stockpile in the constrained Midwest market that did not have adequate pipeline outlets to Gulf Coast refinery centers. As a result the US Midwest benchmark crude West Texas Intermediate (WTI) had begun to be heavily discounted against crudes sold at the coast that were priced relative to the Brent benchmark. By the start of 2011 the WTI discount to Brent was over $5/Bbl but it widened rapidly throughout 2011 to peak at over $26/Bbl in September of that year. In June 2011 the posted price that Bakken producers received for their crude was discounted to WTI by about $13/Bbl because of the lack of pipeline capacity. When you added that discount to the WTI/Brent spread it meant that producers in North Dakota were getting about $30/Bbl less for their crude than the international price of Brent crude. That was a pretty big incentive to build a railroad terminal.

Between June 2011 and today – as seen in the chart below – the view of Bakken production changed dramatically. By February of 2013, actual production (green shaded area on the chart) had grown to 900 Mb/d – exactly what it was previously expected to be in 2016. And the forecast this month (May 2013) is for production to grow to just under 1.4 MMb/d by the end of 2016 getting towards double what it was forecast to be in 2011 (blue shaded area on the chart). As we have discussed previously these unexpectedly high production increases were caused by dramatic improvements in drilling and fracturing technology and efficiency (see Will the Crude Production Boom Keep Running).

About the song

The song “Too Gone, Too Long” sung by Randy Travis reached #1 on the Billboard Country chart in March 1988

Comments

I am lucky to have found your site, it is extremely useful and always seems detailed to just the right degree. Please keep up the great work as I for one truly appreciate it. Job well done all.

Respectfully,

Greg Kouri