The Bentek Eagle Ford crude oil production outlook back in 2011 pointed to a four fold increase in production to 900 Mb/d over the five years to 2016. That number was actually achieved in under two years and today’s forecast calls for 1.5 MMb/d production by 2016. Those growth rates are remarkable enough but the super light nature of the crude being produced means much of it is better classified as condensate. The challenge for producers and refiners in Texas going forward is to find adequate markets for increasing volumes of condensate. Today we continue a series reflecting on the speed of change that shale production is dictating.

A couple of weeks back Rusty gave the keynote presentation at Benposium on May 14, 2013 titled “Why What We Thought We Knew About the North American Hydrocarbon Market No Longer Matters”. Despite the complicated title, it boiled down to a simple premise. If we look back to see what folk were forecasting for North American energy markets two years ago in 2011 and then compare that to today’s actual data and forecast, what would that tell us about the changing pace of North American energy production?

Looking at the data from Bentek – produced as always at the time in good faith based on what the market was telling them – we see that the scale of change going on in North American energy production exceeded everyone’s expectations. We looked at crude oil production forecasts in the Williston Basin and the Eagle Ford, the natural gas production forecast in the Marcellus and the US NGL production forecast from Bentek around the time of the June 2011 Benposium. What we found was that in every case – crude oil, natural gas and NGLs - today’s forecast numbers for what we expected by 2016 are at least double what they were back in 2011. In the first episode in this series (see Too Wrong for Too Long? – How 2011 Bakken Crude Forecasts Compare to Today) we looked at surging crude production in the Bakken. We learned how production surpassed earlier forecasts because rail transport options allowed producers to bypass the queue for pipeline takeaway capacity that might otherwise have slowed them down. In the second episode in the series we looked at how rapid growth in the Marcellus natural gas production forecast is going to have dramatic consequences for traditional natural gas flows into the northeast in the coming years (see How Marcellus Forecasts Changed the World Sooner Than We Thought).

In this episode we look at how the Eagle Ford crude and condensate production forecast increased from 900 Mb/d to 1.5 MMb/d in just two years. Along the way a lot more of that crude production turned out to be condensate than anyone had guessed or planned for.

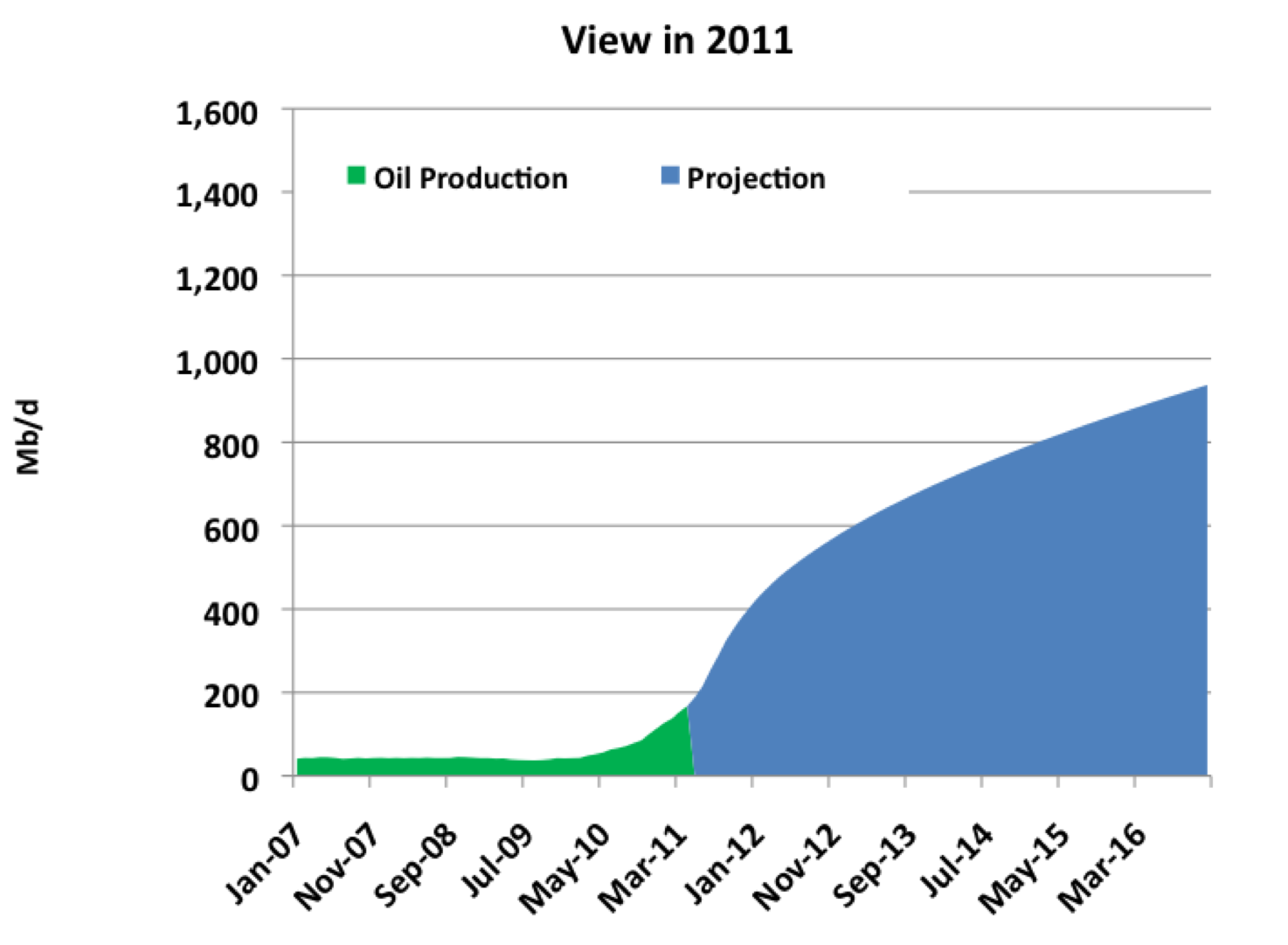

Looking back to Benposium in 2011 there was no slide showing the outlook for Eagle Ford production – it was just not that important at that time! Later in 2011 Bentek were showing the chart below that indicated a rapid growth prospect from 175 Mb/d of crude production in 2011 to 900 Mb/d in 2016. That was a pretty hefty four-fold increase and open to accusations of hype at the time.

Source: RBN Presentation at Benposium 2013

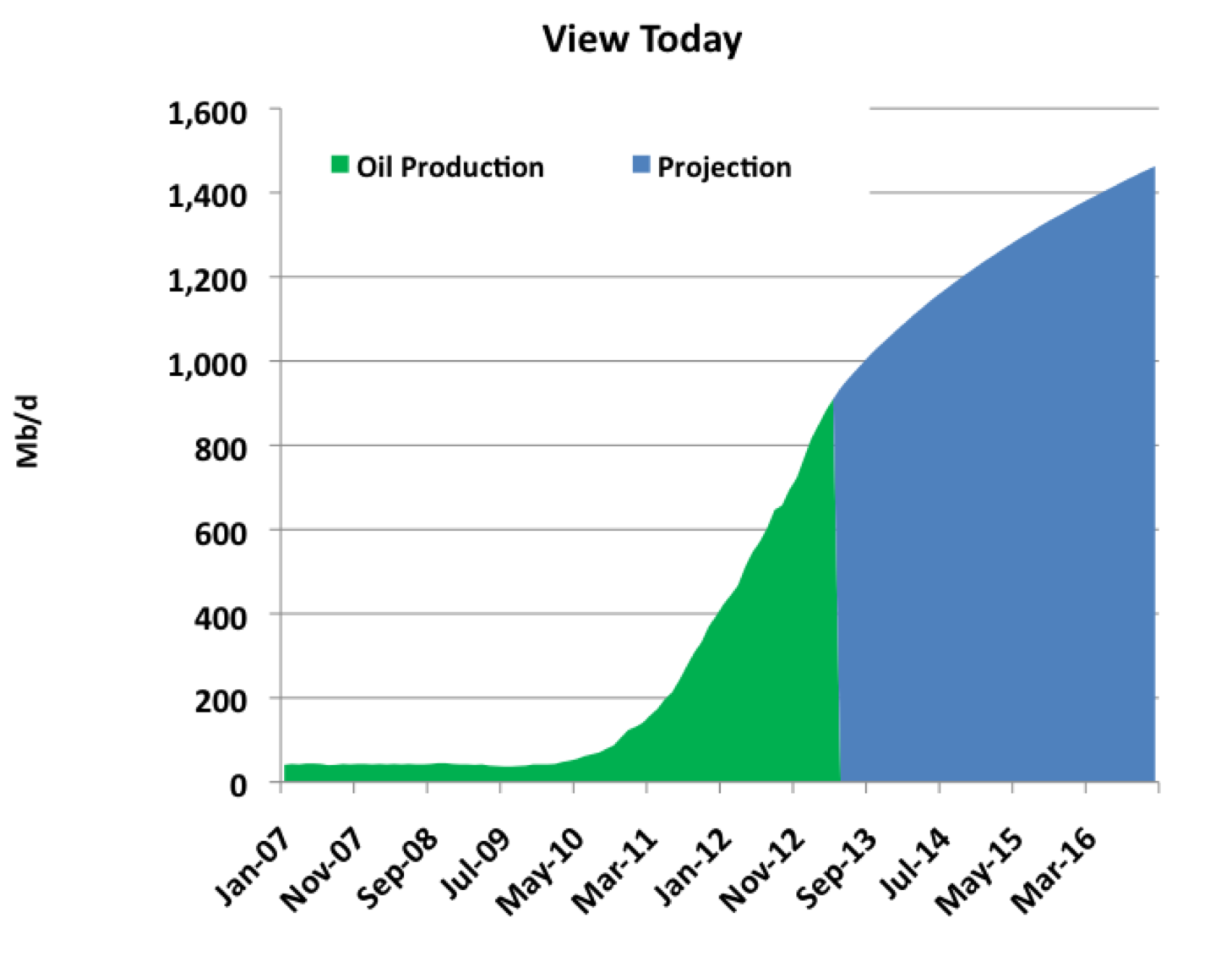

Of course the forecast in 2011 turned out not to be hype at all but rather an underestimate. The next chart (below) shows the outlook this year with production already at 900 Mb/d and headed to 1.5 MMb/d by the end of 2016. The dramatic increases in Eagle Ford crude production were enabled by increased and continued successful drilling – including a move away from dry gas to oil and liquids when natural gas prices fell towards the end of 2011. The other factor that facilitated the rapid increase in Eagle Ford production was the development of takeaway infrastructure. We have reported on that infrastructure build out previously (see Knocking on Heaven’s Door – Transport to Market and Eagle Ford Crude and Condensate Takeaway). Unlike the Bakken where early production spikes quickly ran into pipeline capacity constraints, the Eagle Ford has been blessed with more than adequate takeaway capacity. The Enterprise and Kinder Morgan crude pipelines completed in 2012 deliver between them 750 Mb/d of crude into Houston from the Eagle Ford. Pipelines belonging operated by Koch, Nustar, Magellan and Plains can also carry as much as 1.25 MMb/d of crude to Corpus Christi where it can be loaded onto barges for onward transportation to Houston, St James, LA or the Eastern Seaboard (including Canada).

Source: RBN Presentation at Benposium 2013

The major surprise that increasing Eagle Ford production presented producers and refiners with was that a great deal of the liquids production initially identified as crude oil was actually made up of lighter hydrocarbons more properly called condensate. Here at RBN we have made it our obligation to try and educate readers on the nuances of exactly what is and is not condensate (see Fifty Shades of Condensate – Which One Did You Mean and Through the Looking Glass). The bottom line is that an increasing amount of Eagle Ford liquids production falls into a category of light or super-light hydrocarbons called lease condensate. This liquid condensate has gravity between 45 and 80 degrees API compared to a “regular” light sweet crude such as the US benchmark West Texas Intermediate that has 40 degrees API. The fact that condensate is more like natural gasoline (also known as plant condensate) than crude oil changes the markets that it can be sold to.

The total volume of Eagle Ford production and the percentage that is condensate is growing. Our view is that Eagle Ford condensate production is already up to 500 Mb/d and will be growing by another 150 Mb/d to the end of 2015. Over in West Texas, the Permian basin also has 200 Mb/d of condensate production, expected to grow by another 30 Mb/d over the next two years. That adds up to total condensate production from Texas up to almost 900 Mb/d by the end of 2016 (see chart below). Gulf coast refiners need this stuff like a hole in the head. They are already getting more light sweet crude from Bakken and the crude oil side of Eagle Ford than they can use. Their lack of respect for condensate has led to near $20/Bbl discounts for condensate purchases at the wellhead (see Knocking on Heaven’s Door Part I). Which leaves a challenge for Texas producers trying to find a home for their condensate barrels – especially since they can’t be exported (see Fifty Shades Lighter - The Export Problem).

Comments

http://www.bizjournals.com/sanantonio/blog/2013/05/oil-production-in-eagle-ford-exceeds.html The Texas Railroad Commission reports Eagle Ford oil production currently at 530 mbpd and condendsate at 90 mbpd.