At a time when market prices have been weakened by a surplus of new natural gas production waiting for demand to develop, Mexico has been stepping up to the plate by increasing imports. Gas demand for Mexican power generation, industrial use, and commercial and residential space heating continues to increase at a torrid pace south of the Rio Grande, much to the relief of gas producers in the Eagle Ford, the Permian Basin and other U.S. plays within reach of the international border. Today we provide an update on Mexico’s growing dependence on U.S.-sourced gas, and the implications for producers and midstream companies.

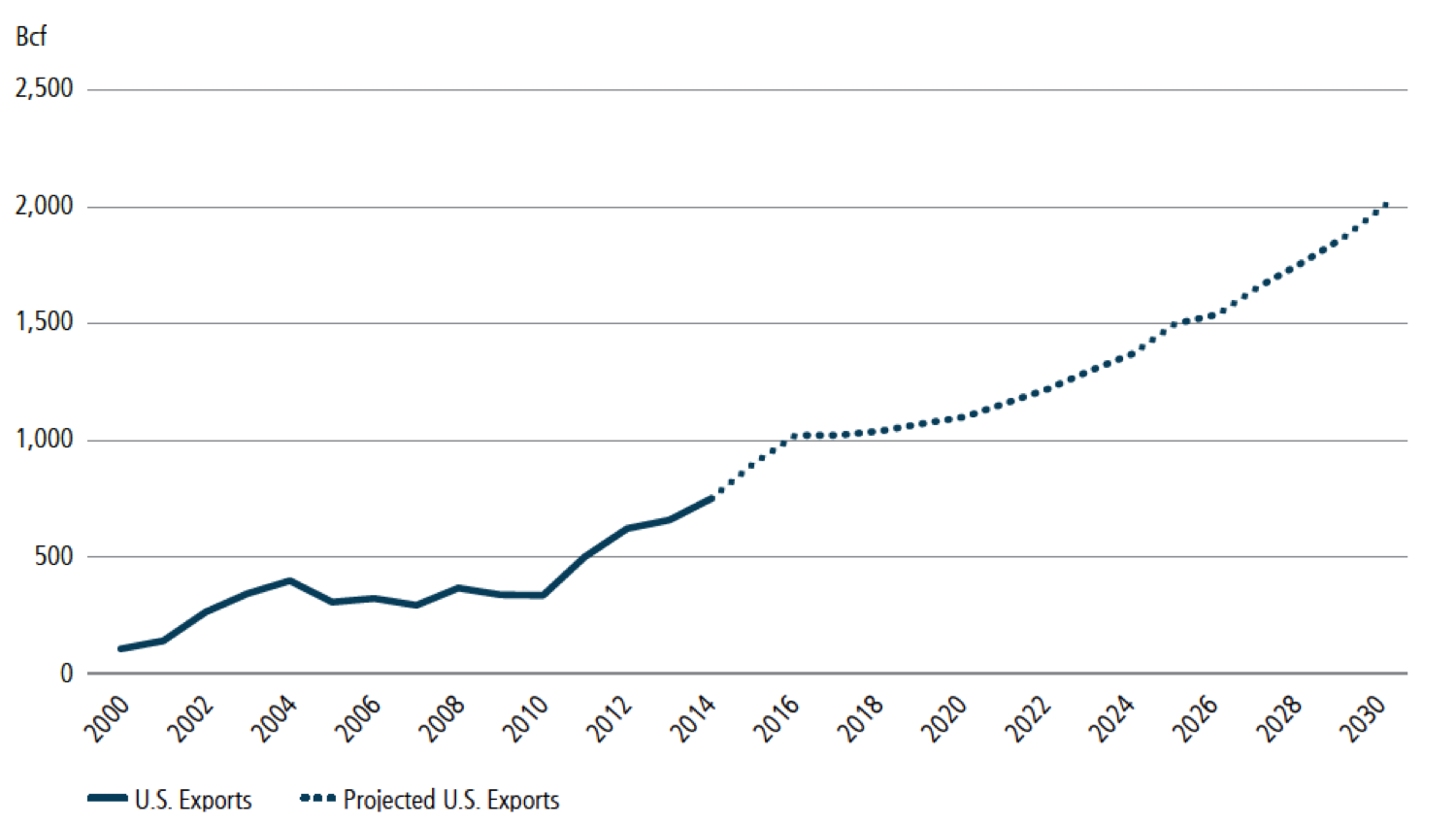

There’s said to be more than 500 Tcf of technically recoverable shale gas in Mexico, much of it in the Burgos and Sabinas basins just south and west of the Eagle Ford. But the shale plays south of the border are said to be geologically complex, and cracking their gas-extraction code is akin to cracking a very sophisticated safe. Besides, Mexico’s gassiest areas lack the road and water infrastructure that development would require, and (yet another negative) they are rife with drug-cartel gangs and violence. For now, Mexico, (whose 2014 gas demand averaged 7.2 Bcf/d) is focused on maintaining its sagging domestic gas production (4.4 Bcf/d last year), and on developing the gas pipelines it needs to import increasing volumes of U.S.-sourced gas and move it south to population and industrial centers, where Mexico’s state-owned Comisión Federal de Electricidad (CFE) and independent power companies are developing thousands of megawatts (MW) of gas-fired generating capacity to support a growing economy. It’s been quite a ride for U.S. gas exports to Mexico that have more than doubled from 2010 to 2014 (900 MMcf/d to 2 Bcf/d) and averaged 2.5 Bcf/d in the first two months of 2015 (up more than 40% from the previous January/February); by 2016, gas deliveries from the U.S. to Mexico are expected to average more than 2.7 Bcf/d (or 1 Tcf/year, according to the U.S. Department of Energy’s Quadrennial Energy Review released in April 2015; see Figure #1), and by 2030 DOE sees U.S. gas exports to Mexico doubling again, to 2 Tcf/year or nearly 5.5 Bcf/d.

Source: U.S. Department of Energy Quadrennial Energy Review, April 2015

Continued growth in Mexican gas demand and imports is welcome news not only to U.S. producers, who are looking for incremental demand to match their rising production, but to U.S. midstream companies (and energy investors), who are provided new opportunities to co-develop and invest in Mexican gas pipelines. Given Mexico’s growing need for U.S. gas, we’ve looked South of the Border several times, starting with our U.S. Natural Gas Headed Way Down South, Way Down To Mexico Way series, then in No Need for Mexicali Blues, and most recently in Help Me(xico) Make It Through The Night. (We also posted a blog last week about Mexico’s application to import U.S. crude oil – see Have Another Swap). In our coverage of gas we traced the quickening pace of Mexican demand (most of it tied to new gas-fired generation) and gas pipeline development, as well as the opening up of Mexico’s long-monopolized energy sector.

About the song

"They All Went to Mexico" was written by Greg Brown and appears as the fifth song on side two of Carlos Santana's fifth solo album, Havana Moon. Featuring Willie Nelson on vocals, the song was released as a single in May 1983. Personnel on the record were: Willie Nelson (lead vocals), Carlos Santana (guitar, backing vocals), Booker T. Jones (keyboards), Barry Beckett (keyboards), David Hood (bass), Graham Lear (drums), Flaco Jimenez (accordion), Mic Gillette (trumpet), and Armando Peraza, Raul Rekow, Orestes Vilato (percussion). The song was produced by Carlos Santana, Booker T. Jones, Barry Beckett, and Jerry Wexler.

Havana Moon was Santana's first foray into a hearty blend of Tex-Mex music. It featured guest artists such as Willie Nelson, the Fabulous Thunderbirds, Booker T. Jones, and Flaco Jimenez. It was recorded at The Automatt in San Francisco and produced by Jerry Wexler and Barry Beckett. Released in April 1983, the album went to #55 on the Billboard Top 200 Albums chart.

Carlos Santana is a Mexican-American guitarist who rose to fame with his Latin American rock band Santana in the late 1960s. He put the original Santana band together in San Francisco in 1966. Bill Graham arranged for the band to appear at Woodstock, and their successful show there helped to propel their debut album, Santana, to #4 on the Billboard Top 200 Albums chart in 1969. As a solo artist, Carlos Santana has released seven studio albums, three live albums, six compilation albums, and five singles. The band Santana has released 25 studio albums, seven live albums, 23 compilation albums, and 61 singles. Carlos Santana has collaborated on 25 albums with other artists. The band Santana has won one American Music Award, one Billboard Latin Music Award, four Brit Awards, five Grammy Awards, and two Latin Grammy Awards. As a solo artist, Carlos Santana has won one Billboard Century Award and one Grammy Award. He is the recipient of Kennedy Center Honors and his band Santana was inducted into the Rock and Roll Hall of Fame in 1998.

Willie Nelson is an iconic American singer, songwriter, musician, and actor. He has released 95 studio albums, 13 live albums, two soundtrack albums, 51 compilation albums, and 130 singles. He still records and tours, as does Carlos Santana.