This winter the Northeast US is being blasted with record cold weather. As a result, daily natural gas prices in both New York and New England have spiked more than $30/MMBtu above the US benchmark at Henry Hub, LA. But the average price you’ll pay for natural gas in the region will likely depend on whether you root for the New York Giants or the New England Patriots. With their dismal records and embarrassing mistakes, it’s not easy being a Giants (or Jets) fan these days. But on average – thanks to new gas pipeline capacity added this past fall, natural gas prices in New Jersey and New York have remained less volatile relative to US benchmark Henry Hub, LA than prices in New England. That is because the six-state region continues to suffer from woefully inadequate gas transmission infrastructure. Today we begin a two-part analysis of the still-stalled effort to deliver more supplies to gas-hungry New England.

In the first blog in this three-part series—“Another Gassy Day in New York City—The New Gas Pipelines”—we described how several major pipeline projects between the Marcellus and the Big Apple have eased gas delivery constraints in the region and shrunk price differentials this year. The economic impact of this de-bottlenecking should be substantial: Spectra Energy figures its $1.2 billion New Jersey-New York expansion project, which came online November 1 (2013), will save customers $700 million/year in lower gas prices. In contrast the failure to relieve gas-pipeline congestion in New England has had the opposite effect, driving up wintertime gas prices and even threatening the reliability of the electric grid by forcing gas powered generation to shut down in the absence of firm supplies.

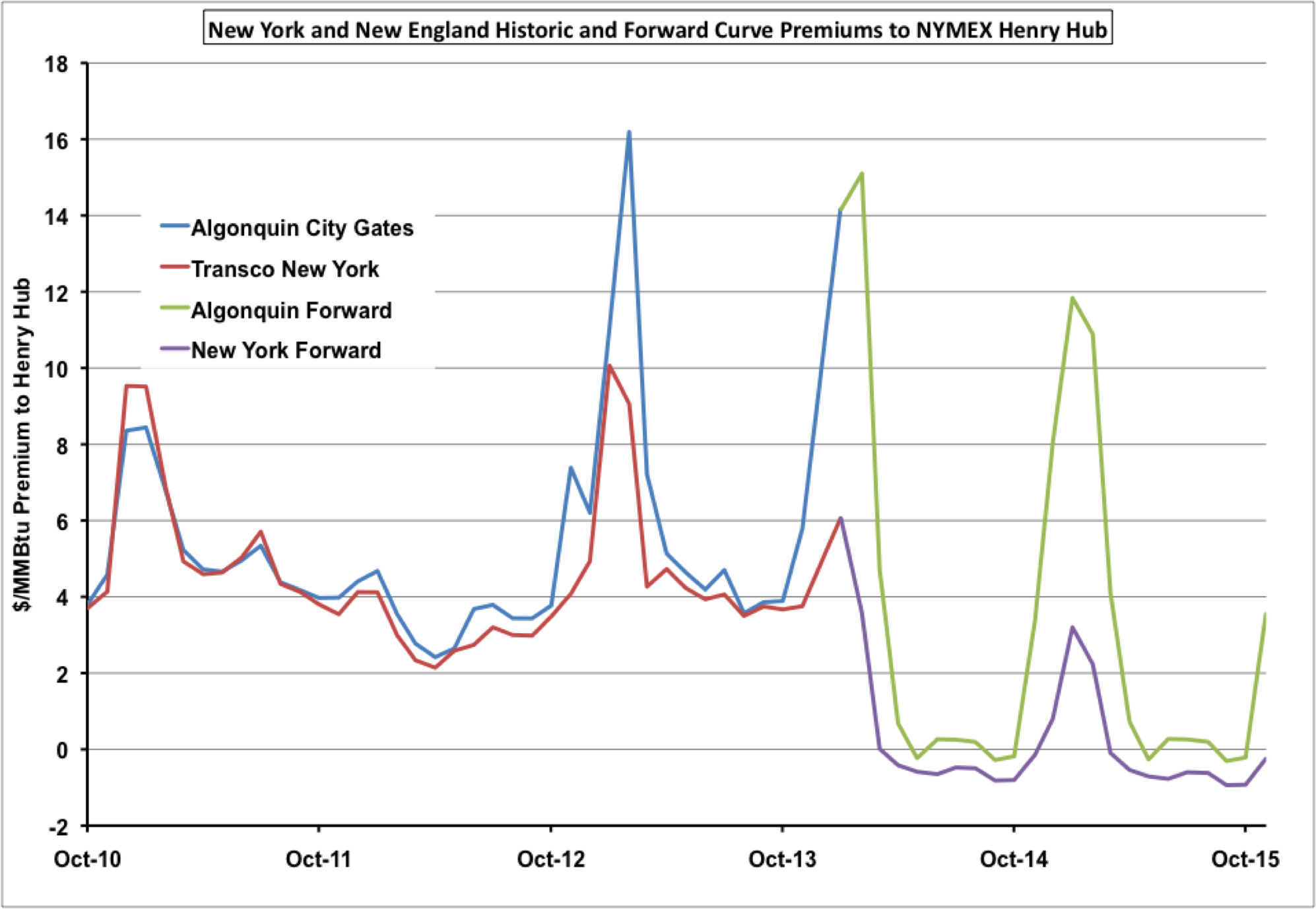

Figure 1 shows monthly average historical and forward-curve prices for natural gas delivered into New York City and at Algonquin city gates in New England as of December 31, 2013. The prices are shown as premiums to CME/NYMEX Henry Hub Louisiana. The historical data shows that both New York and Algonquin average prices increased in the winter months. Recent pipeline enhancements that eased most constraints into northern New Jersey and New York City have reduced winter New York City premiums to Henry Hub going forward but the lack of pipeline capacity serving New England means that Algonquin premiums to Henry Hub remain larger in the winter months going forward. (Forward curves tell us the value that futures traders will pay today for deliveries in the future--see Seasons in the Shade for more on natural gas forward curves and seasonality).

Figure 1

Source: CME data from Morningstar (Click to Enlarge)

New England wants to use more natural gas. Homeowners and businesses in the region know there are potential savings if they switch to gas from oil for space heating. (See “Fuel for the City—Dislodging Oil From the Northeast,”) The power generation sector also sees potential cost savings from switching to gas as well as regulatory benefits to shifting away from coal and oil to comply with tightening environmental regulations. But as we said in “Déjà vu All Over Again—Northeast Natural Gas, Pipelines and Big Decisions,” New England can’t benefit fully from cheap Marcellus gas until sufficient pipeline capacity is in place to deliver gas when it’s needed—even on the coldest winter day. The rub is that the Federal Energy Regulatory Commission (FERC) will not allow new pipeline projects to be built unless they demonstrate “market need” by securing binding commitments of 10 years or more for the capacity the new or expanded pipelines would provide. Unless New England can find a way to power through FERC’s pipeline-approval process (and their own state regulatory issues, for that matter) the region may face gas-delivery shortfalls for years to come.

Five pipelines provide virtually all of New England’s gas—the Tennessee Gas Pipeline (TGP), the Algonquin Gas Transmission (AGT) line, and the Iroquois Gas Transmission (IGT) line from the west through New York State, and the Maritimes & Northeast Pipeline (MNP) and the Portland Natural Gas Transmission (PNGT) from the east and north through New Brunswick and Quebec, respectively. (There’s also the Everett, MA LNG import terminal, though it’s become much less of a factor because higher international gas prices make imports to the US uneconomic at present.) Figure 2 below, from an ICF International report to ISO-New England, the region’s electric-system overseer, shows the region’s pipelines as well as its gas-fired power plants. (Several more gas-fired plants are being planned.)

About the song

“Please Come to Boston,” written and sung by Dave Loggins, was released in 1974; it rose to Number 5 on Billboard’s Hot 100 and to Number 1 on Billboard’s Easy Listening chart.