Over the past six months, natural gas production in the Marcellus has continued to ramp up, despite low gas prices and pipeline capacity constraints. It would have grown even faster if capacity had not held back well completions. But new pipeline capacity is coming, and as it comes on line, the production growth rate will accelerate. In the not too distant future, the Northeast will no longer need imports from Canada. Then imports from the Midwest will be backed out. And eventually all inflows from the U.S. Gulf region could come to a halt. That will be a vastly different gas market than we’ve known over the 25 years since decontrol. In today’s blog we’ll drill down into some of the important implications of this, the Great Flow Reversal of 2016.

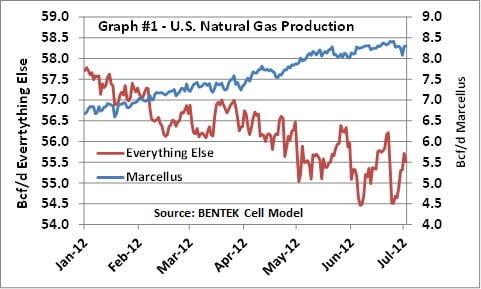

Before we get into the nitty-gritty, let’s briefly recap the findings of Part I and Part II of this series. In Part I we examined how production in the Marcellus has been increasing while the aggregate of all other producing regions has been declining. Graph #1 is an update of that story. These are Bentek numbers from their Cell Model that assesses daily supply and demand in ten different regions (Cells) across North America based on pipeline flow data. The blue line is Marcellus production on the right scale, up from 6.7 Bcf/d on Jan. 1, 2012 to about 8.3 Bcf/d today. That is up a huge 1.6 Bcf/d since the first of the year, but dipping slightly in the most recent two weeks. The red line is production from all other regions, down from 57.7 Bcf/d in January to 55.5 Bcf/d today. That most recent dip in production is mostly offshore production cutbacks due to the Debbie hurricane threat. Effectively Marcellus has been holding up production for the rest of the country.

In the balance of Part I we looked at Tennessee pipeline, and how an oversupply of natural gas in the northeastern Pennsylvania dry portion of the Marcellus has been driving prices down, while prices just 100 miles to the east in Tennessee Zone 6 were frequently the highest prices in the nation. We attributed this volatile price differential to pipeline capacity constraints into the Northeast.

That got us to Part II, where we started with a June 21st blowout in the Tennessee Zone 4 Marcellus price versus the Tennessee Zone 6 price. And that eventually took us to a review of the pattern of natural gas demand in the Northeast. Graphs #2 and #3 below break that story down a little further. Graph #2 shows Industrial and Power Burn (gas fired power generation) demand since 2008. In those sectors the high demand period is in the summer when cooling loads result in high demand. But the range between high and low demand is never more than 2 to 3 Bcf/d. The big swing in demand is still from the Residential and Commercial sectors in the winter -- when demand jumps from less than 2 Bcf/d in the summer to more than 25 Bcf/d in the winter.