Subtitle: Rupture in the Space-Time Continuum

Yesterday the highest and lowest natural gas prices in the country were only 100 miles apart - on the same pipeline. Weird stuff like this happens in the middle of winter, but not in late spring. The pipe is Kinder Morgan’s Tennessee Pipeline, a.k.a, TGP. The lowest price in the country based on ICE next day cash market trading was TGP-Zone 4 Marcellus, averaging $1.65/MMbtu for the day. The highest price was just 100 miles east in TGP Zone 6 at $2.56/MMbtu. In today’s world of tiny natural gas basis differentials (Honey, I Shrunk the Basis), this is an incredible shoulder-season differential of more than $0.90/MMbtu. What could cause such a rupture in the space-time continuum? How long will the situation continue? Why does this development portend dramatic, long-term changes in natural gas flows across North America? Of course, the culprit is the Marcellus, where production is still roaring regardless of low gas prices. Today we’ll look at the impact of all this new production just a hop, skip and jump away from the biggest natural gas markets in the country.

Production

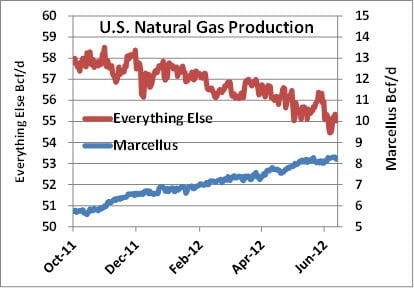

The graph below shows U.S. Natural Gas Production (total pipeline quality gas or residue gas, lower 48) from October 1, 2012 until today. These are Bentek numbers from their Cell Model (discussed here in Dodge the Bullet) that assesses daily supply and demand in ten different regions (Cells) across North America based on pipeline flow data. The blue line is Marcellus production on the right scale, up from 5.7 Bcf/d on Oct. 1, 2011 to about 8.2 Bcf/d today. The red line is production from all other regions, down from 57.8 Bcf/d in October 2011 to 55.1 Bcf/d today. So the Marcellus floated the boat for the rest of the country - up 2.5 Bcf/d while everything else was down 2.7 Bcf/d. Who knows what would be happening to gas prices if it weren’t for those darned Marcellus producers?

Flows

The majority of Marcellus production flows into one of five pipelines: Columbia Gas, Dominion, Texas Eastern, Transco and Tennessee. About one-third goes into Tennessee. Columbia and Transco have a little less than 15% each. The rest is split between Dominion, Texas Eastern and other pipes in the region. Tennessee dominated Marcellus flows from mid-2009 until 2011 when they started to hit capacity constraints. Whichever way you look at it, the growth of Marcellus production volume into Tennessee is staggering. The graphic below shows Bentek flow data for Tennessee’s Marcellus region receipt points. From near zero in October 2008, Tennessee receipts are now about 2.5 Bcf/d.

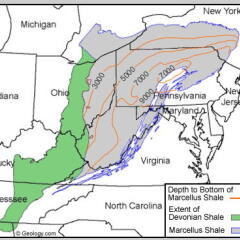

A lot of this gas comes into Tennessee from the northeastern or “dry” portion of the Marcellus, and the majority of that gas comes from four Pennsylvania counties: Bradford, Susquehanna, Tioga, and Wayne. In a happy circumstance for the pipeline, the Tennessee 300 Line goes pretty much straight through those counties. The gas Gods definitely smiled on Tennessee there. But that’s a lot of gas hitting a market traditionally used to no production whatsoever. And that has led to the incredible pricing disparity that started us down today’s path of enquiry.

Tennessee Pipeline (Market Area)

To understand what is going on, you need to know a little about Tennessee pipeline. Tennessee is one of the big “T” pipes (including Texas Eastern and Transco). It runs from the Mexican border to Northeastern Canada and ultimately all the way to Boston. The pipeline moves gas from the Gulf and Appalachia through the Ohio Valley into markets across the Midwest and Northeast, including New York and Boston.

Look at the map on the left, below. Tennessee enters the Northeast region at the Ohio-Kentucky border and then splits into two major routes or “legs” in Mercer County, Pennsylvania. The “200” leg continues north through New York state, connects with TransCanada at the Canadian border, and then heads east to Boston. The “300” leg goes straight through the prolific “dry” Marcellus producing counties of Bradford, Susquehanna, Tioga, and Wayne (dashed blue oval) before moving into the big market areas in New Jersey, New York City, and Connecticut. Finally the two legs join back up in Massachusetts.