Over the next five years, natural gas production in the Marcellus is expected to double, from just less than 8 Bcf/d today up to almost 16 Bcf/d in 2016. As that production enters the market, volumes that have traditionally served the Northeast market from LNG imports, Canadian imports, inflows from the Rockies/Midwest, and inflows from the Gulf will no longer be needed. Last week we examined possible scenarios for these flow shifts. Today we’ll look at the ramifications for regional supply imbalances and where the traditional supplies will be going if not to the Northeast in this, the Great Flow Reversal of 2016.

This is part IV of our series titled The Marcellus Changes Everything. In Part I we looked at the trajectory of Marcellus production, which has continued to increase even as other basins around the country have declined. In Part II we reviewed natural gas demand patterns in the Northeast, and how new sources of supply just two or three hundred miles away from the big market demand centers could impact regional flows. Last week in Part III we dissected the six primary sources of natural gas supplies into the Northeast market last winter using the Bentek Cell Model, and showed that regional production averaged 6.9 Bcf/d, Canadian imports were 1.3 Bcf/d, the region received 1.5 Bcf/d from the Rockies/Midcontinent and another 6.2 Bcf/d from the Southeast/Gulf region. Storage made up 2.9 Bcf/d of supply for the season and there was a tiny volume of LNG imports. In total, it was an average demand of about 19 Bcf/d.

That got us to the punch line. As another 8 Bcf/d of production comes into the market (Bentek forecast), there will no longer be a need for any LNG imports, Canadian imports, inflows from the Rockies/Midcontinent, or eventually even from the Gulf. By 2016, most of these flows will be history except for some inflows from the Gulf during the winter months.

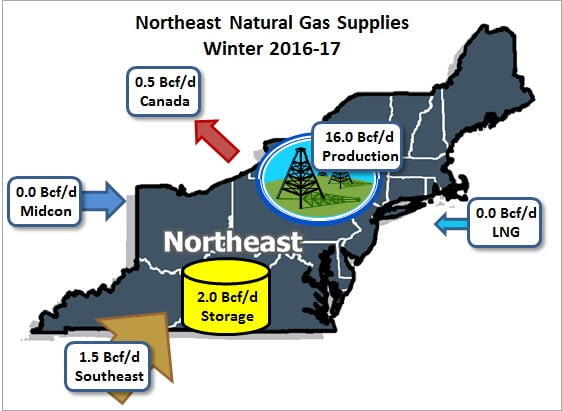

Consider the possibility of the scenario shown in the graphic below for the winter of 2016-17. Let’s say average demand comes in at the same number as this past winter – 19 Bcf/d. By that time the U.S. is exporting 0.5 Bcf/d into Eastern Canada, even in the winter. With zero inflows from the Midcontinent/Rockies, 1.5 Bcf/d from the Gulf and 2.0 Bcf/ out of storage, the market balances. Just a couple of years ago, 8.5 Bcf/d flowed into the Northeast from the Gulf during the winter months. After the Great Reversal, this number is down to 1.5 Bcf/d and could certainly continue lower. Winter flows on REX into Ohio are zero. Utilization of storage capacity has declined – gas supplies are right next door.

And all of this transpires in the winter. How about the summer? Well, presumably there is still 16 Bcf/d coming out of the ground. Summer demand in the Northeast runs about 11 Bcf/d. To store enough for 2.0 Bcf/d withdrawals (5 month withdrawal season) we’ll need to inject about 1.5 Bcf/d during the 7 month injection season. So 16 – 11 -1.5 = 3.5 Bcf/d that needs to go somewhere. Let’s assume that 0.5 Bcf/d gets exported to Eastern Canada, same as the winter months. That leaves 3.0 Bcf/d that needs to get out of Dodge, so to speak. Five possibilities come to mind to dispose of the surplus: (1) reverse inbound pipes from the Midcontinent, (2) reverse inbound pipes from the Southeast/Gulf, (3) Export the surplus as LNG, (4) use the additional volumes to generate power (presumably replacing coal), or (5) shut-in production and don’t make so much of the stuff in the first place.