Western Canadian heavy crude oil producers have a lot of rail tank cars on order but so far none of the loading terminals in the production region can handle unit trains. The pace of terminal development in Alberta is far slower than North Dakota in 2012. Because you can ship raw bitumen without diluent there are potential cost savings over pipelines but the load and offload facilities are more complex. Today we conclude our mini survey of Canadian heavy crude loading terminals.

Yesterday’s blog (March 19, 2013) was the first of two on rail loading facilities for heavy crude in Western Canada. This second part will not make much sense without reading Part 1 first. All of the episodes in this crude by rail series can be found at the www.rbnenergy.com website under the Daily Energy Post tab. If you did read yesterday’s post then recall that increased Canadian heavy crude production in the next few years will struggle to find space on congested pipelines to the US Gulf Coast. That congestion has caused price discounts for crudes like Western Canadian Select (WCS) against the benchmark US inland West Texas Intermediate (WTI) and heavy crude grades on the Gulf Coast like Mexican Maya. If Canadian producers can get their crude to the Gulf Coast – the destination where the greatest number of refineries are configured to process heavy crude – they can realize far higher prices. So while waiting for new pipeline capacity slated to come online by the end of 2014, they are looking seriously at rail alternatives.

We left off yesterday discussing how transporting heavy crude by rail offers options to shippers as far as the amount of diluent included with the heavy bitumen crude. When heavy crude is shipped by pipeline it needs to be diluted to a required specification to flow in the pipe – generally about 30 percent diluent to 70 percent bitumen. That “dilbit” blend can be loaded on and off rail tank cars like other lighter crudes. Bitumen can also be transported by rail in a form known as "railbit" using 15 - 20 percent diluent or in its raw form with no diluent at all. The amount of diluent that is used depends on the type of rail tank car and the offloading facilities at the destination.

The advantages of shipping raw bitumen by rail with no diluent or as railbit with less diluent are:

- Saving on the cost of acquiring diluent to blend with bitumen - including transportation – often from the US (see Fifty Shades of Eh? Part 1 and Part 2). Altex Energy estimates the incremental cost of purchasing and transporting 30 percent diluent at around $9/Bbl (source: www.altex-energy.com)

- Less diluent means more transport capacity is available for bitumen – meaning you ship up to 30 percent more crude

- Refiners do not desire diluent mixed with bitumen – it creates a dumbbell crude that contains light components that are not useful to refineries configured to process heavy crude (see Turner Mason and the Goblet of Light and Heavy)

- Not having to dilute bitumen with diluent makes transport safer because if the rail tank car is damaged it won't escape into the environment since it does not flow at ambient temperature

The disadvantages are:

- Railbit and raw bitumen have to be transported in rail cars that are insulated to prevent the bitumen from solidifying in cold weather

- Loading raw bitumen in cold weather requires heating equipment at the loading terminal

- Raw bitumen has to be transported in rail cars that contain steam coils for re-heating the bitumen at destination

- The destination rail offloading facility has to be equipped with steam and nitrogen injection systems to heat the rail car coils and remove the crude – slowing the offloading process

- Additional cleaning treatments are required to prepare railcars for reuse

- Bitumen is heavier than dilbit and rail cars can only carry 550 Bbl of bitumen versus 650 Bbl of lighter crudes

The additional cost of shipping raw bitumen by rail is hard to pin down accurately but the infrastructure needed to handle heavy crude requires investment. PBF Energy who currently ship 40 Mb/d of raw Canadian bitumen to their Delaware City, DE refinery estimated that crude costs them $5/Bbl more to ship than light crude sent by rail from North Dakota. Canadian producer Southern Pacific’s plans to ship railbit with 20 percent diluent from Fort McMurray in Alberta to the Gulf Coast include returning the rail tank cars to Canada full of diluent that can be sold to reduce the roundtrip rail cost.

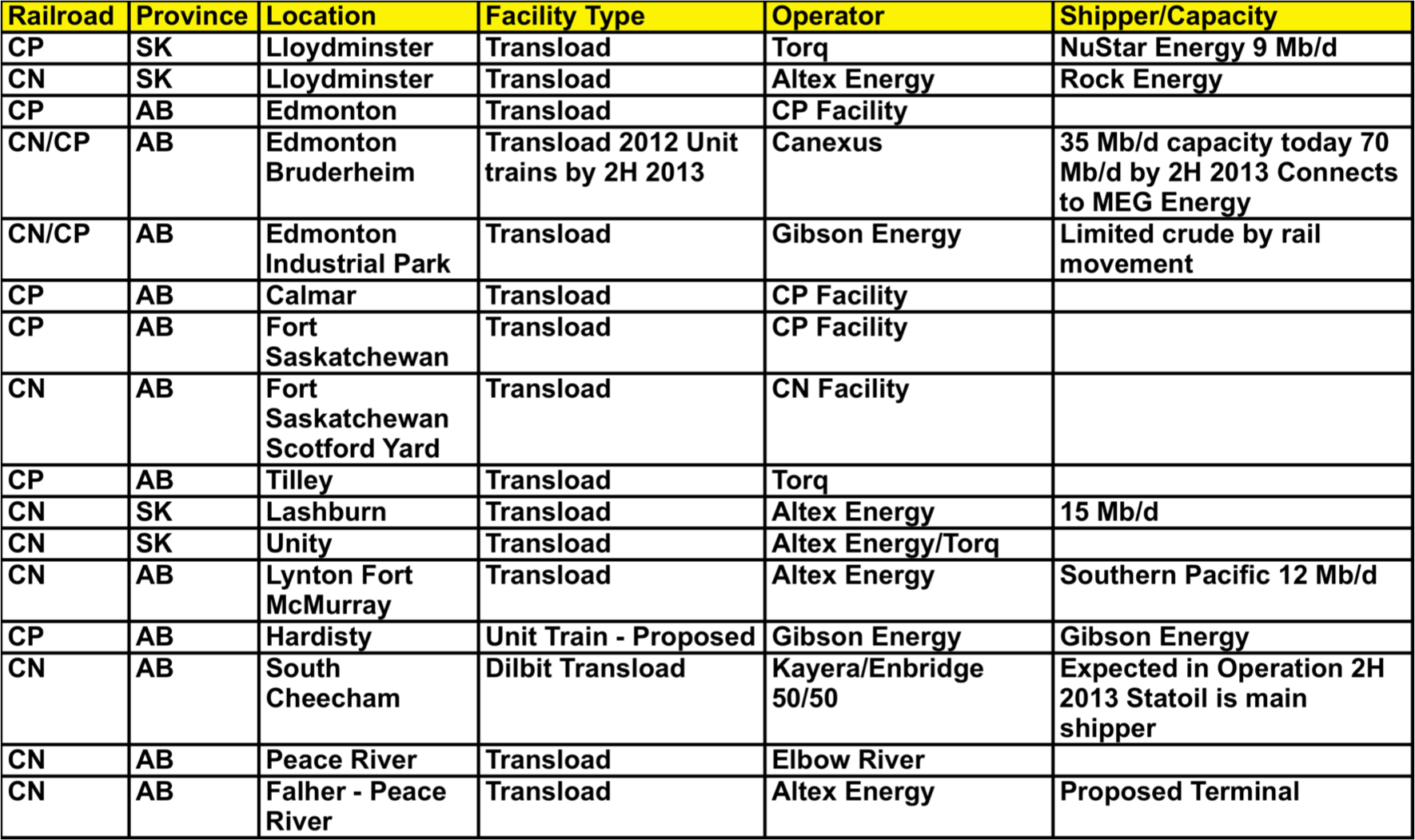

Heavy crude rail loading facilities in Western Canada

The table below lists heavy crude rail loading facilities that are either operating or planned in the heavy oil production region of Western Canada. For each terminal we list the railroad, location, operator and any known shipper and capacity information. Many of these are small facilities with truck to rail transload capability. Only one – the Canexus operated Edmonton Bruderheim terminal will be able to handle unit trains during 2013. There are plans by two other operators - Gibson Energy at Hardisty and Torq/NuStar at Lloydminster to build out unit train size loading terminals. Following the table we provide additional color on the operations of the principal terminal owners and operators.

Source: RBN Energy

Gibson Energy Inc

Gibson is one of the largest truck haulers of oil, natural gas liquids, propane, butane, condensate and refined products in North America. Gibson built 5 truck to rail transloaders in Western Canada during 2012. Gibson’s March 2013 Investor Presentation states that they are shipping about 6 Mb/d of heavy and light crude. Gibson has two large terminals with storage facilities at Edmonton and Hardisty and both of these sites are served by railroads. The Gibson Edmonton terminal has access to both Canadian Pacific (CP) and Canadian National (CN) railroads but the company does not appear to be loading crude onto rail there currently. Gibson is discussing plans with producers and shippers to build a unit train heavy crude oil loading facility on the CP railroad at the company’s Hardisty terminal. Based on the Hardisty terminal development plans, Gibson Energy estimates costs of $14-$21/Bbl for rail shipment to the Gulf Coast from Hardisty. Gibson further breaks that down as $17 - $21/Bbl for manifest trains (meaning the rail tank cars can be mixed with other freight and will typically take longer to travel to their destination) and $14 - $17/Bbl for dedicated unit trains.

Altex Energy

Altex Energy is a privately owned Canadian company that builds and operates rail terminals in Western Canada specifically to ship crude oil to the US Gulf (the company’s name is short for Alberta to Texas). Altex has 4 terminals in the heavy oil production regions and works closely with the CN railroad. Three of these terminals are smaller transloading facilities in Lloydminster, AB, Lashburn, SK and Unity, SK. The Lashburn facility loads 15 Mb/d. Altex operates the Lynton rail terminal at Fort McMurray. Southern Pacific Resources a heavy oil sands producer has contracted with CN and Altex to ship up to 12 Mb/d from Lynton to a Genesis Energy terminal in Nachez, MS, (85 miles north of Baton Rouge, LA). The bitumen will then be transferred to barges for onward distribution to Gulf Coast refineries. The Southern Pacific agreement with Altex, CN and Genesis is for 5 years and also involves trucking crude oil 28 miles from Southern’s STP-McKay production plant. The bitumen will be shipped with 20 percent diluent and the rail tank cars will ship diluent back to Alberta on the return trip. Southern Pacific estimates the cost of truck, rail and barge transport to Gulf Coast refineries to be $31/Bbl.

Altex is planning to build additional transload terminals at Falher close to Peace River and Fort Saskatchewan, AB close to Edmonton.

Torq Transload

Torq is a specialist trucking and rail terminal operator based in Dollard, SK. The company has rail transload terminals in the Saskatchewan part of the Williston basin at Shauvenon and Bromhead (see A Plethora of Terminals in the Williston Basin). Torq also has heavy crude transload terminals in Lloydminster, AB, Tilley, AB and Unity, SK. The Lloydminster terminal (Torq/NuStar) is the largest facility – shipping about 9 Mb/d of raw bitumen to the 74 Mb/d NuStar asphalt refinery in Paulsboro, NJ. NuStar’s has touted plans to enlarge the Lloydminster facility to a unit train operation with 80 to 120 tank car capacity.

Canexus Corp

Canexus owns a rail to crude transloading terminal just outside Edmonton at Bruderheim, AB that currently handles up to 35 Mb/d. The company is building out a unit train facility that will increase capacity to 70 Mb/d by the second half of 2013. This project is linked to a pipeline from producer MEG Energy Corp’s Stonefell, AB storage terminal. Like Southern Pacific, MEG will ship bitumen to the Gulf Coast on CN railroads and then distribute it by barge to refineries

Canadian Pacific and Canadian National Railroads

Both CP and CN serve the southern part of Alberta and Western Saskatchewan including Lloydminster and Edmonton. Both railroads also have facilities at the Fort Saskatchewan oil and gas distribution center northeast of Edmonton. Only CN has a rail line that runs out to the oil sands production regions northeast of Edmonton at Fort McMurray and northwest at Peace River. CN developed a plan for moving heavy crude by rail back in 2008 during a previous pipeline capacity crunch. Those plans – involving an alliance with Altex Energy – never came to much. CN has better destination options for Canadian heavy oil producers because its network stretches all the way to the Louisiana Gulf Coast. CP routes mostly run east across Canada. CN signed an agreement this month (March 2013) to move crude through the LBC Tank Sunshine terminal in Geismar, LA.

Future Expectations

The terminals built out so far for transloading crude onto rail in the heavy oil sands region are not yet significant. Peters and Co – a Calgary investment research company – estimates that year end 2012 shipments of heavy oil out of the region by rail amounted to about 60 Mb/d. These are expected to double during 2013 to 120 Mb/d. Those numbers won’t make much of a dent in the 1 MMB/d additional heavy crude production expected in Western Canada over the next five years. The only clear evidence of significant interest in crude by rail shipments of heavy crude is in the tank car industry’s back order book. That order book of about 48,00 railcars contains 19,000 from Canadian producers (source: Rail Theory Forecasts). These railcars are insulated to carry heavy crude but will not be delivered until 2014 so they could represent a precautionary hedge by Canadian producers worried that they will need to ship more crude by rail if planned pipelines to the Gulf Coast do not get built.

It is understandable that Canadian producers are not building out loading terminals today with quite the fervor of their Bakken counterparts in 2012. As we said in Part 1, most heavy crude is going to end up at the Gulf Coast where refinery demand is greatest. With only one destination, the flexibility of rail loses some of its advantage – especially since producers know that additional pipeline capacity is on the way. When (and if) new pipeline capacity from Alberta to the Gulf Coast is completed, shipping costs by pipeline will be far lower than rail in spite of the advantages of shipping without diluent. Once the pipelines are built the price differentials between WCS and Maya can be expected to narrow and producers will no longer be able to recoup any of the higher cost of rail from the spread.

Looking at Canadian heavy crude rail load terminals you get the distinct impression that producers are kicking the tires on rail at the moment. Those that have invested significantly – like MEG Energy and Southern Pacific have specific needs based on new production coming online at a time when pipelines are full. None of the larger producers appear to be abandoning pipelines in the same way as we saw in North Dakota during 2012. If Canadian pipeline projects such as Keystone XL, the Northwest Gateway and Trans Mountain expansion do not get built then the rail option will attract far more attention. In the meantime, heavy oil rail load capacity development is looking more like a watch and wait game.

Next up in our crude by rail series we round out our loading terminal survey with a look at facilities outside of the Bakken and Canada