During the past two years the US domestic crude transportation business has been revitalized by a huge increase in shipments of crude oil by rail. In the Bakken region alone over 600 Mb/d of crude is shipped to market by rail. The number of rail terminals in producing regions loading crude oil onto rail tank cars has increased from a handful at the end of 2011 to 88 and growing today. A further 66 crude oil unloading terminals have been built or are under construction. Today we summarize the crude oil terminal build out by region and by railroad.

Previously on Crude Loves Rock’n’Rail…

The first episode in this crude by rail series provides an introduction and overview of the “Year of the Tank Car” (see Crude Loves Rocking Rail). We describe the rapid growth in US crude oil production that put pressure on pipeline logistics and made rail a viable alternative for moving crude to market. The second installment (see Crude Loves Rocking Rail – The Bakken Terminals) began our survey of rail loading terminals with a map and a complete list of facilities in North Dakota. The follow up episodes covered EOG, Hess and Inergy, Plains, Enbridge and Global, Bakken Oil Express, Dakota Plains, BakkenLink and Savage and Bakken terminals north of the Canadian border in A Plethora of Terminals in the Williston Basin. We discussed the development of rail terminals loading heavy oil sands bitumen crude in Western Canada in two episodes Heat It! (Bitumen Economics Part 1) and Part 2. The last episode on rail loading covered terminals built outside the Bakken and Canada in the Niobrara, Eagle Ford, Permian and Anadarko basins as well as Cushing, OK (see Load Terminal Craze). Next we surveyed rail destination terminals covering the East (see East Coast Delivery Terminals) West (see West Coast Destinations) Eastern (see The Bakken St James Shuttle) and Western Gulf Coasts (see Houston Ship Channel and Outside the Ship Channel respectively. The most recent episode (see Brent WTI and the Impact on Bakken Netbacks) provided a comparison map to show how a Bakken producer would reckon the destination and mode of transport to give them the best return or “netback”.

The Big Picture

In this episode we present summary tables from our series to highlight where rail load and destination terminals have been built and which railroads the terminals can connect with. Aside from these tables it is also helpful to visualize where crude is moving by rail on a map. Here are a couple of web resources that we found useful. The first is a map of the US with most of Canada and Mexico that shows the main Class 1 railroad infrastructure by Railroad Company. The map is available from the Port of Vancouver website here. When we get some bandwidth we should add the crude-by-rail terminals to this map. A second useful resource is specific to BNSF railroad. As we shall see, BNSF is by far the dominant player in crude-by-rail movement and they have reinvested some of their profits in an interactive map especially for oil freight. You can see the map here. Although it only covers BNSF infrastructure it shows all the load and unload regions as well as the BNSF terminals.

Loading Regions

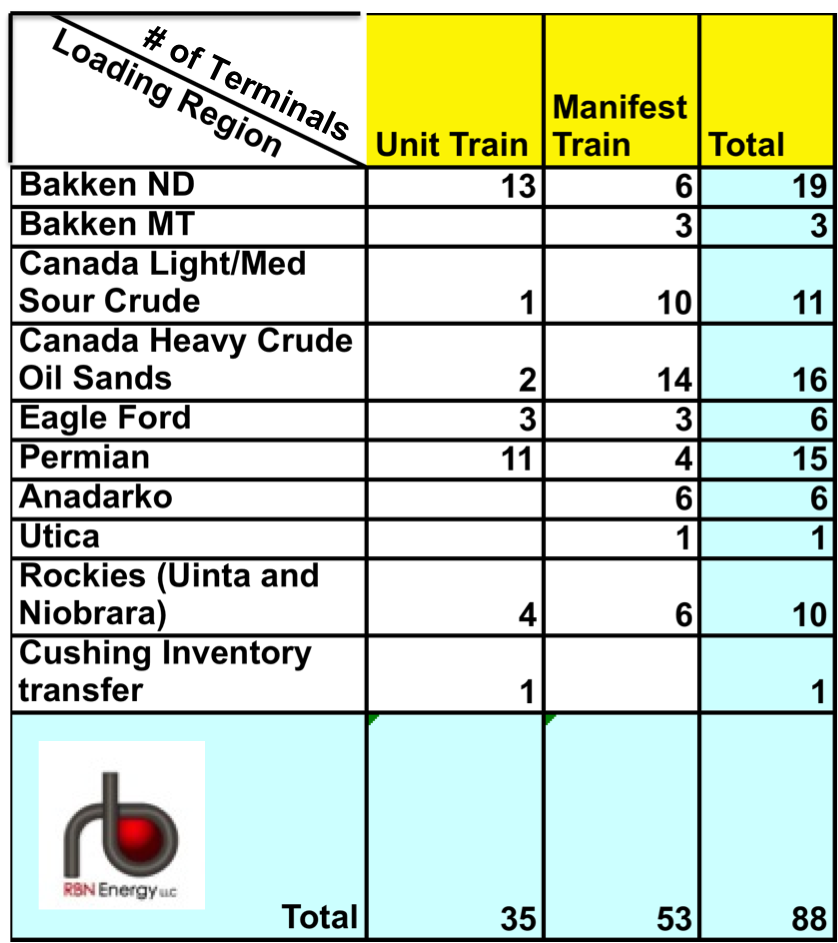

We covered each of these load regions in separate episodes earlier in the series. Table #1 below is a summary of the terminals that are currently being used to load crude onto rail tank cars. Note that this table contains terminals that were not included in earlier episodes of this series because the details were not available to us at that time. Some of the terminals will not complete construction until the end of 2013 or early 2014 but most are operational. It will not be a surprise to anyone following our narrative that the Bakken has the most load terminals of any crude producing region. Since we last surveyed the terminals in North Dakota a new manifest terminal has been added at Boyle in Stark County, operated by Cenex Energy also known as CHS transport. This is a manifest terminal on the BNSF railroad. According to the BNSF interactive map we mentioned a minute ago, there are also 3 CHS manifest terminals across the State border in Montana. In all there are 22 terminals serving the Bakken on the US side with 13 able to load unit trains (100 rail tank cars or more). Many of the 11 terminals included in the “Canada Light/Medium Sour Crude” row of the table are loading crude from Bakken production on the Canadian side of the border.

Behind the Bakken in terms of numbers of load terminals comes the Western Canadian oil sands region of Alberta and northern Saskatchewan. We identified 16 terminals in the region – mostly small-scale manifest train loading operations. By the end of 2013 two of these terminals will be able to load unit trains. Since we originally covered the Permian Basin (links to all the previous episodes in the series are in the opening section above so we will not keep repeating them), we received information from RBN members about rapid build out of loading terminals in West Texas. There are now at least 15 load terminals in the Permian and 11 of these are being developed for unit trains. Another big growth region for crude by rail is the Rockies with 10 terminals in operation or being built with four unit train facilities. There are fewer rail terminals loading crude in the Eagle Ford because there is already significant pipeline infrastructure in place. The grand total of crude loading terminals is 88 – the vast majority of which have been built out from scratch in the past two years – indicating how responsive the railroads and midstreamers have been in putting these deals together

Table #1: Source: RBN Energy

Destinations

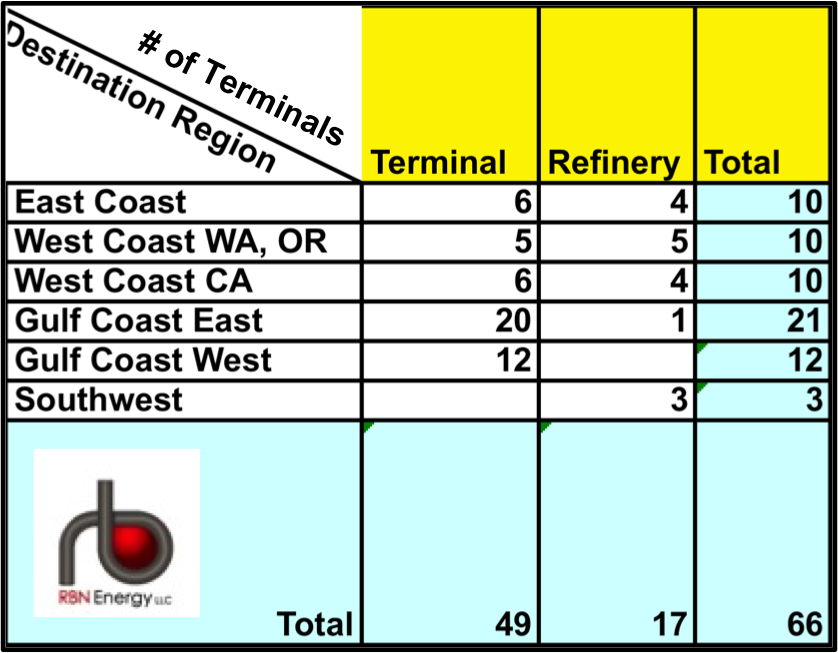

Table #2 below summarizes the destination terminals where crude is unloaded. The table is divided by unloading region. The terminals are then divided into two columns indicating whether they are merchant terminals or built specifically for one refinery. The main trends to note in this table are that 49 out of the 66 or 74 percent are what we have called merchant terminals. Midstream companies that charge a throughput fee generally operate these terminals. The majority of these facilities offer access to waterborne barges for final distribution to refineries. The largest number of refineries that have built their own receiving facilities is in Washington State where – led by Tesoro, all the major refineries have or are building rail receipt terminals. The area with the least number of refinery specific terminals is the Gulf Coast. In the Gulf Coast west of the Mississippi there are 20 terminals on the river (some as far north as Illinois) that transfer crude from rail to barges or pipelines. In the Texas Gulf Coast (west) there are 12 terminals. The total number of destination terminals that we identified is 66.

Table # 2 Source: RBN Energy Analysis

Railroads

Our third table (Table #3 below) summarizes the load and destination terminals by railroad connection. Among loading terminals in the crude oil producing regions, BNSF is the big guy on the block. By the fortunate accident of having their existing network running right through the Bakken as well as the Permian, Rockies and Anadarko basins, they connect with 41 crude loading terminals or 46 percent of the 88 loading terminals we identified. Not that BNSF has exactly stood still and taken their freight revenue from this windfall. They have made extensive investments and worked closely with companies like EOG in the Bakken to make crude by rail efficient and cost effective.

Comments

Hi Sandy,

Are any of the unit trains moving oil or product both ways? One would think that trains to WA state could bring back diesel and gasoline to ND, and trains from the oil sands could bring back dilutent, thus maximizing tank cars that now have lease rates that have tripled and locomotive and track time.

Thx,

Alex