In the recently fervent efforts of oil and gas companies to mitigate their environmental impact and improve their standing with investors and lenders, they are progressively striving to cut their own emissions of greenhouse gases and to offset the GHG emissions that are unavoidable through the use of carbon credits. Cutting emissions from well sites, pipeline operations, refineries, and the like won’t be easy or cheap, but at the least the results are measurable and provable — before, we emitted X, and now we emit X minus Y. The true value of voluntary carbon credits is more difficult to calculate. Sure, each credit is said to equal one metric ton of carbon dioxide or its equivalent, but how do you really measure with any certainty how many metric tons of CO2 will be absorbed by 1,000 acres of preserved forest in Oregon, or how much methane won’t be produced by changing the diet of 1,000 cows in Wisconsin? And how can you be sure that slice of Oregon wouldn’t have been left in place anyway, or that the dairy farmer has actually changed what he’s feeding his herd? In today’s RBN blog, we look at voluntary carbon credits, concerns about their validity, and ongoing efforts to ensure that they actually accomplish the goal of GHG reductions.

Only a few years ago, companies in every part of the oil and gas industry were trying to wrap their heads around the Shale Revolution and what it would mean for them. Producers were grappling with how to fine-tune their drilling and completion techniques to wring more crude oil, natural gas, and NGLs out of their rock. Midstreamers were repurposing existing pipelines and building new ones to accommodate mammoth production growth in the Marcellus/Utica, Bakken, and other fast-growing shale plays. Refiners were looking at crude-slate changes and physical alterations to their facilities to make fuller use of the light sweet crude the U.S. was suddenly producing in abundance.

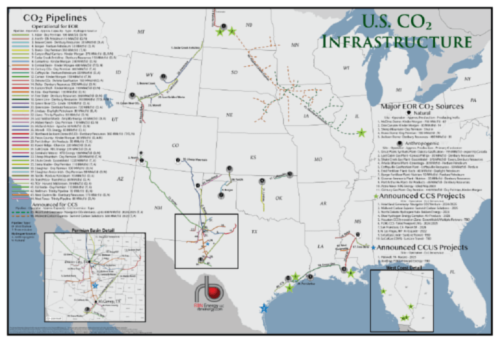

RBN Energy’s US CO₂ Infrastructure map brings together legacy Enhanced Oil Recovery (EOR) assets, as well as announced large-scale Carbon Capture and Sequestration (CCS) and Carbon Capture, Utilization and Sequestration (CCUS) projects, all in our signature concise, accurate, and intelligible style.

Now, in addition to coping with the energy-market dislocations associated with COVID-19, these same companies are educating themselves about ESG-related issues and establishing aggressive goals for reducing their GHG emissions — with some even aiming to become entirely “carbon-neutral” by mid-century. As we said in Part 1 and Part 2 of this blog series, a growing number of market players have been dipping their toes in these ESG waters by offering shipments of carbon-neutral LNG, crude oil, and LPG, where every metric ton (MT) of CO2 emitted during production, processing, shipping, and end-use consumption is said to be matched one-for-one with an MT of independently verified, “nature-based” carbon offsets. In Part 3, we discussed efforts by a number of U.S. and Canadian midstream companies to reduce GHG emissions from pipelines by, among other things, switching from gas to electric compressors, developing solar projects to power their operations, funding projects to reducing emissions elsewhere — and acquiring carbon credits.

About the song

“A Matter of Trust” was written by Billy Joel and appears as the third song on side one of his 10th studio album, The Bridge. Released as the second single from the album in July 1986, "A Matter of Trust" went to #10 on the Billboard Hot 100 Singles chart. Personnel on the record were: Billy Joel (lead, backing vocals, guitar, acoustic piano, synthesizer); David Brown and Russell Javors (guitar); Doug Stegmeyer (bass), Liberty DeVito (drums), and Jeff Bova (synthesizer).

The Bridge was recorded in 1985-86 at The Power Station, Chelsea Sound, and RCA Studios in New York City and Evergreen Studios in Burbank, CA. Produced by Phil Ramone, the album was released in July 1986. It went to #7 on the Billboard Top 200 Albums chart, and has been certified 2X Platinum by the Recording Industry Association of America. Four singles were released from the LP.

Billy Joel is an American singer, songwriter, and musician from New York who has sold over 150 million records worldwide. He started his career as a member of The Hassles, who made two albums for United Artists in 1967 and 1969. Joel then formed the keyboard and drum duo, Attila, who released one album for Epic in 1970. Stephen Thomas Erlewine of All Music wrote: "Attila undoubtedly is the worst album released in the history of rock and roll." Joel himself has called the album "psychedelic B.S." He started his solo career in 1971, with the release of his debut album, Cold Spring Harbor. Billy Joel has released 13 studio albums, six live albums, 16 compilation albums, and 61 singles. He has won five Grammy Awards, is a member of the Rock and Roll Hall of Fame, and has been awarded a Gershwin Prize for Popular Song from the Library of Congress and a Kennedy Center Honor. He continues to write music and occasionally perform live.

Comments

Part IV of the blog series, A Matter of Trust, is interesting and relevant. As for certification of authenticity, there's got to be some enforcement of those products that back new futures contracts. I have no idea how CME or other exchanges do it but presumably they have some leverage to keep the private analysts honest and, perhaps, push some methodologies over others.