The Biden administration has placed some big bets on clean hydrogen, seeing it as a replacement fuel for some hard-to-abate industries and putting it at the heart of its long-term decarbonization efforts. All of these bets are backed by a brand-new tax credit. But the goal isn’t just to drive production of more hydrogen — it’s also to make hydrogen in a specific way, with measurable decreases in greenhouse gas (GHG) emissions. That means producing hydrogen that qualifies for the tax credit is going to be a lot easier said than done. The proposed rules include a concept called deliverability — one of the “three pillars” of clean hydrogen — that adds further challenges to producers hoping to cash in on the tax credit and puts into further peril any number of potential projects. In today’s RBN blog, we’ll explain how deliverability works, how it fits into the proposed rules, and the challenges it will pose for hydrogen producers and power generators alike.

RBN Energy’s US CO₂ Infrastructure map brings together legacy Enhanced Oil Recovery (EOR) assets, as well as announced large-scale Carbon Capture and Sequestration (CCS) and Carbon Capture, Utilization and Sequestration (CCUS) projects, all in our signature concise, accurate, and intelligible style.

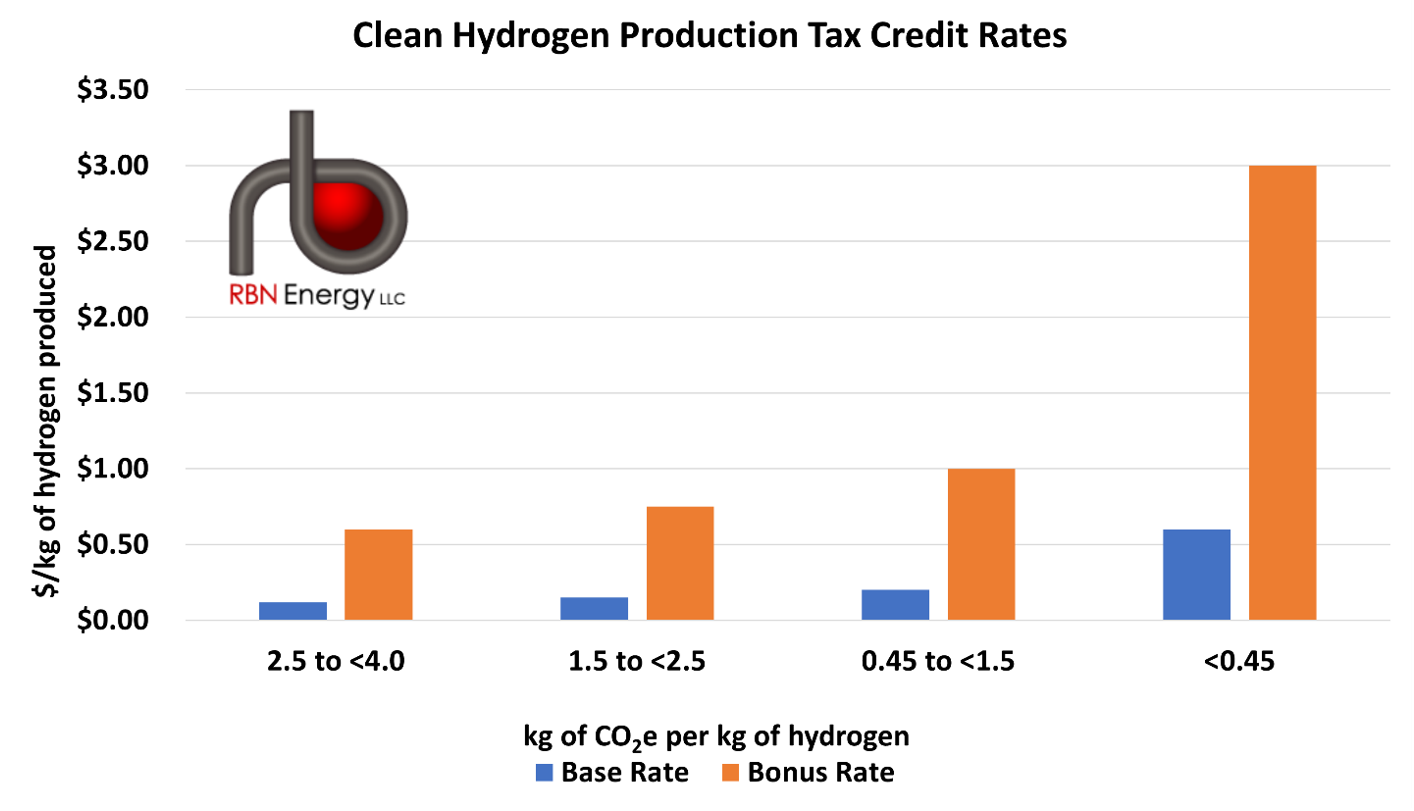

A frequent topic of debate — and fierce lobbying — following passage of the Inflation Reduction Act (IRA) in August 2022, the proposed rules around the federal government’s Hydrogen Production Tax Credit (PTC), also known as 45V, were rolled out in late December 2023. Under 45V, credits of up to $3/kilogram (kg) are available based on the rate of lifecycle GHG emissions during a clean hydrogen facility’s first 10 years of operation. As defined by the IRA, clean hydrogen is produced in a way that results in a lifecycle GHG emissions rate of not more than 4 kg of carbon dioxide (CO2) equivalent per kilogram of hydrogen (CO2e/kg). As we described in Part 1 of this series, that new standard could severely limit how much of the tax credit is available to many of the potential low-carbon hydrogen production facilities. For example, a blue hydrogen project — one in which hydrogen is produced through the auto thermal reforming (ATR) or steam methane reforming (SMR) of natural gas, with the resulting emissions mitigated by carbon capture — can qualify for the credit if it has sufficiently high carbon-capture rates, but the proposed regulations likely limit it to the bottom two tiers of the credit (two pairs of blue and orange bars to left in Figure 1) due to a “locked” upstream natural gas feedstock emissions factor. As you can see, there are four tiers to the credit, based on the lifecycle GHG emissions rate, and the credit is far less generous for production that falls into the bottom three tiers (three blue and orange pairs to left) than the highest tier (blue and orange pair to far right).

Figure 1. Breakdown of 45V Tax Credit. Source: Treasury Department Note: The PTC includes a base rate (blue bars) and a bonus rate (orange bars), which is 5X the base rate and is for producers that meet prevailing wage and apprenticeship requirements.

About the song

“Gimme Three Steps” was written by Ronnie Van Zant and Allen Collins and appears as the third cut on side one of Lynyrd Skynyrd’s debut album, Pronounced Leh-nerd Skin-nerd. The song was written about an incident that happened to singer Ronnie Van Zant at a bar in Jacksonville, FL, called The Pastime. Ironically, “Gimme Three Steps” failed to chart when it was released as a single in November 1973; it has since become one of the band's most popular songs. On a side note, mega-selling Los Angeles band Poison played this song regularly as a part of their set in LA clubs before being signed to their first record deal. Personnel on the record were: Ronnie Van Zant (vocals), Gary Rossington (lead guitar), Allen Collins (guitar), Ed King (bass), Billy Powell (keyboards), and Bob Burns (drums).

Pronounced Leh-nerd Skin-nerd was recorded between March and May of 1973 at Studio One in Doraville, GA, with Al Kooper producing. Most of the songs on the album had been played and tested live for some time and were rehearsed to perfection at the band’s rehearsal space: Hell House, a non-air-conditioned cabin with a tin roof outside of Jacksonville, FL. They liked the spot because they could play loudly at all hours with no neighbors or police within earshot. Hell House has since burned to the ground and the land on which it sat is now a gated residential subdivision with street names that pay homage to Lynyrd Skynyrd song titles. The album was released in August 1973 and went to #27 on the Billboard 200 Albums chart. It has been certified 2X Platinum by the Recording Industry Association of America. Two singles were released from the LP.

Lynyrd Skynyrd is an American rock band formed in Jacksonville. The band’s roots go back to 1964, performing under a variety of names, with different personnel, before deciding on the moniker Lynyrd Skynyrd in 1969. The name came from Leonard Skinner, a high school gym coach in Jacksonville who hated rock and roll and long-haired guys who played it. They have released 14 studio albums, 14 live albums, 23 compilation albums and 30 singles. The band was inducted into the Rock and Roll Hall of Fame in 2005. More than two dozen band members have passed through their ranks since their formation. The last original member, Gary Rossington, passed away in March 2023 at the age of 71. Rossington hand-picked Damon Johnson (Brother Cane, Black Star Riders) to be his replacement. Cane, along with Johnny Van Zant, Rickey Medlocke, Michael Cartellone, Mark Matejka, Peter Keys and Keith Christopher, continue to record and tour as Lynyrd Skynyrd. After touring the U.S. on the mega-successful Sharp Dressed Simple Man Tour with ZZ Top, the band began their Celebrating 50 Years of Lynyrd Skynyrd Tour in December 2023. The tour resumes in March 2025.

Comments

Before people get too fired up about hydrogen they need to consider the negatives. It's actually a worse atmospheric pollutant than CO2. It's very light so escaped H2 rises through the atmosphere and devours ozone (O3). And it's the smallest molecule so it's difficult to contain. Rubber hoses used to connect things, or to refuel moble transport leak it out. Fill a balloon with H2 and see how long it lasts. One needs to consider how much will be lost through leakage and spillage, especially through poorly maintained equipment, if the entire economy converts to H2.

Lest you think this is just my personal delusion, do some web searches and you'll find serious scientific papers worrying about this.

But politicians want to be seen to do something, so they'll create the next big problem without thinking about it too much first. After all your high school chemistry says H2 burns cleanly so what could possibly go wrong?