On the surface, the Bakken story in the mid-2020s may seem as boring as dirt. The boom times of 2009-14 and 2017-19 are ancient history. Crude oil production has been rangebound near 1.2 MMb/d — well below its peak five years ago. And that output has been getting gassier over time, creating natural gas and NGL takeaway constraints that have put a lid on oil production growth. But don’t buy into the view that the Bakken is yesterday’s news. Beneath the surface (sometimes literally), the U.S.’s second-largest crude oil production area is undergoing a major transformation that includes E&P consolidation, production (and producers) going private, the drilling of 3- and (soon) 4-mile laterals, novel efforts to eliminate flaring, and even a producer-led push for CO2-based enhanced oil recovery (EOR). As we’ll discuss in today’s RBN blog, these changes and others may well breathe new life into the Bakken and significantly improve the environmental profile of the hydrocarbons produced there.

Join us at our historic 20th School of Energy!

School of Energy: Foundations is a two day, in person conference designed to help energy professionals better understand the forces shaping crude oil, natural gas, NGLs, refined products, and petrochemicals.

Attendees will learn from RBN experts, work with Excel based analytical models, participate in Q&As, and network with industry peers.

Build the foundation to better navigate volatile energy markets.

Way back in 2012 — Year 1 in the RBN blogosphere — blogs about the Bakken were a regular thing. Everyone was mesmerized by that amazing shale play in western North Dakota and the eastern edge of Montana, where fast-growing volumes of crude oil and associated gas were being wrung out of seemingly impenetrable shale thanks to that dynamic duo of horizontal drilling and hydraulic fracturing. Sure, the drilling-and-completion techniques were far less sophisticated than they are now, but the production was rising fast enough to spur a frenetic infrastructure buildout. Folks were scrambling just to keep up. By 2014, Bakken oil production was topping 1.1 MMb/d — 11X the early-2009 level — and three-quarters of it (800 Mb/d!) was being loaded into tank cars and railed out because there wasn’t near-enough pipeline capacity to handle the gushing volumes.

Then came the mid-decade crude oil price crash, which sent Bakken production falling to less than 900 Mb/d by late 2016. It bounced back, though — by late 2019, the play’s output was topping 1.4 MMb/d until another price crash, this time brought on by a global pandemic. Production gradually rebounded post-COVID, but with far less oomph than in 2017-19. As we said in the introduction to today’s blog, Bakken crude output has hovered around 1.2 MMb/d in recent months.

So what’s been keeping Bakken production close to flat? A primary reason is the Bakken’s competitive disadvantages to the Permian, the U.S.’s largest production area, which offers lower breakeven prices and easier, cheaper access to key Gulf Coast refinery and export markets. In fact, while Permian production growth itself has stalled in recent months (see All My Rowdy Friends Have Settled Down), the sprawling West Texas/Southeast New Mexico shale play accounted for the entirety of U.S. production growth in 2022-23. Also, as we discussed earlier this year in Take It to the Limit, looming natural gas and NGL takeaway constraints in the Bakken have put a cap of sorts on crude oil production. (We’ll revisit and update the constraints issue later.)

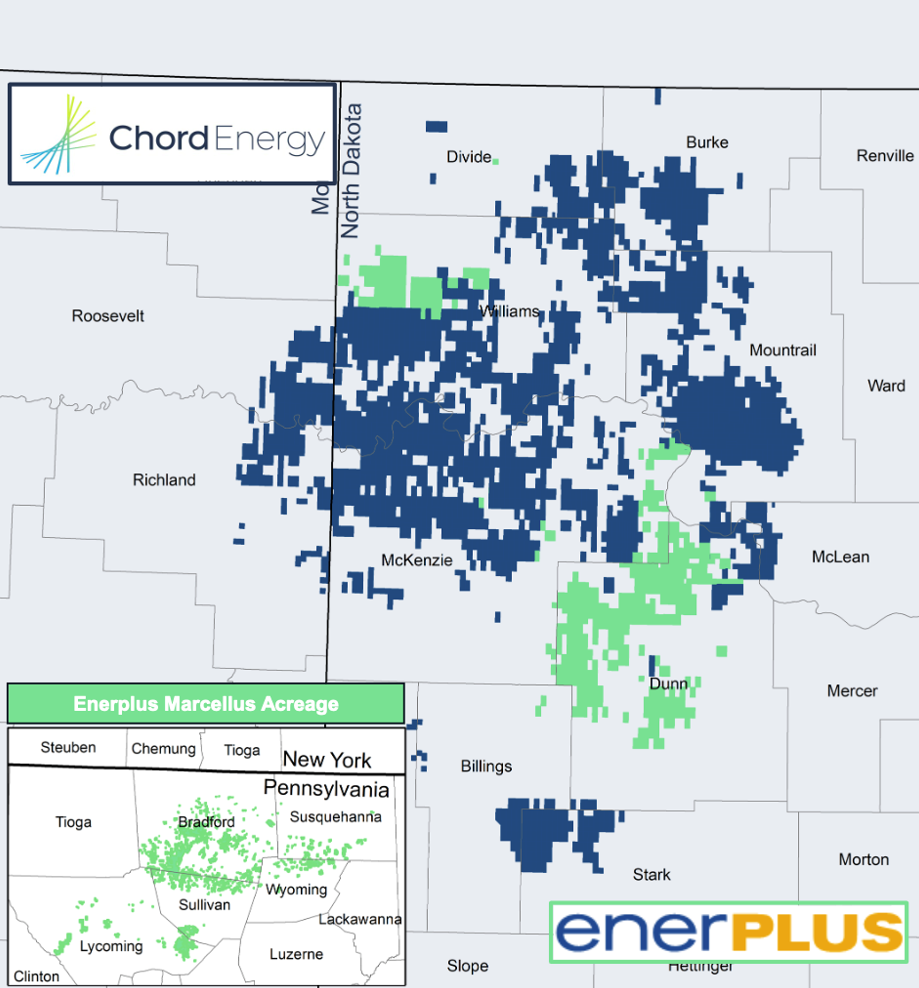

Figure 1. Chord Energy and Enerplus’s Acreage in the Bakken (and Enerplus’s Acreage in the Marcellus). Source: Chord Energy

About the song

“You Don’t Know Me” was written by Eddy Arnold and Cindy Walker in 1955. It was first released as a single by Jerry Vale in February 1956, and later, in April 1956, by Eddy Arnold. The highest-charting version of the song was by Ray Charles, whose version was released in July 1962 — it went to #2 on the Billboard Hot 100 Singles chart. Charles’s take was certified Gold by the Recording Industry Association of America (RIAA). It appeared as the second song on side one of Charles’s 17th studio album, Modern Sounds in Country and Western Music. Recorded at United Western Studios in Hollywood in February 1962, personnel on the record were: Ray Charles (vocals, piano), Hank Crawford (alto saxophone), Gil Fuller, Gerald Wilson (big band arrangements), and Marty Paich (string arrangements). Over the years the song has been covered by such artists as Patti Page, Floyd Cramer, Manfred Mann, Rick Nelson, and Elvis Presley. Charles covered it again with Diana Krall on his 2004 duets album, Genius Loves Company, which was Charles’s final studio album.

Modern Sounds in Country and Western Music was recorded at United Western Studios in Hollywood and Capitol in New York City in February 1962, with Ray Charles and Sid Feller producing. Released in April 1962, it went to #1 on the Billboard 200 Albums chart and stayed there for 14 weeks. It has been certified Gold by the RIAA. In 1999, the album was inducted into the Grammy Hall of Fame. Two singles were released from the LP.

Ray Charles (Ray Charles Robinson Sr.) was an American singer, songwriter, and pianist. Referred to as “The Genius” and “Brother Ray,” the blind musician helped to pioneer soul music in the 1950s by combining blues, jazz, R&B and gospel music. He released 62 studio albums, seven live albums, 39 compilation albums, and 127 singles. He has won 17 Grammy Awards, a Grammy Lifetime Achievement Award, Kennedy Center Honors, a George and Ira Gershwin Award, a National Medal of Arts, a Polar Music Prize, and a star on the Hollywood Walk of Fame. He is a member of the Rock and Roll Hall of Fame, the Rhythm and Blues Music Hall of Fame, and the Country Music Hall of Fame. Charles died at his home in Beverly Hills in June 2004 at the age of 73.