For the past decade, producers in the Permian Basin have been the driving force in domestic production growth, but lately there has been a hard-to-miss slowdown in incremental production rates for crude, gas and natural gas liquids (NGLs). While Permian producers are primarily motivated by crude oil economics, those volumes also come with a lot of associated natural gas and NGLs. These commodities are therefore fundamentally interlinked. So if there’s a hangup with one, the effects will be felt across the upstream and then cascade downstream. There is a lot of money riding on these markets and the impacts of an extended slowdown in the Permian could be monumental, not just in the energy industry but also in the broader U.S. and global economies. In today’s RBN blog, we will examine what’s to blame for plateauing production in the U.S.’s most prolific basin and gauge what its big-picture implications might be.

Join us at our historic 20th School of Energy!

School of Energy: Foundations is a two day, in person conference designed to help energy professionals better understand the forces shaping crude oil, natural gas, NGLs, refined products, and petrochemicals.

Attendees will learn from RBN experts, work with Excel based analytical models, participate in Q&As, and network with industry peers.

Build the foundation to better navigate volatile energy markets.

Warning! Today’s blog is, in part, a subliminal advertorial for RBN’s upcoming School of Energy which will highlight the interlinkages of commodity markets. The conference will be held on June 26-27 in Houston at the Houstonian.

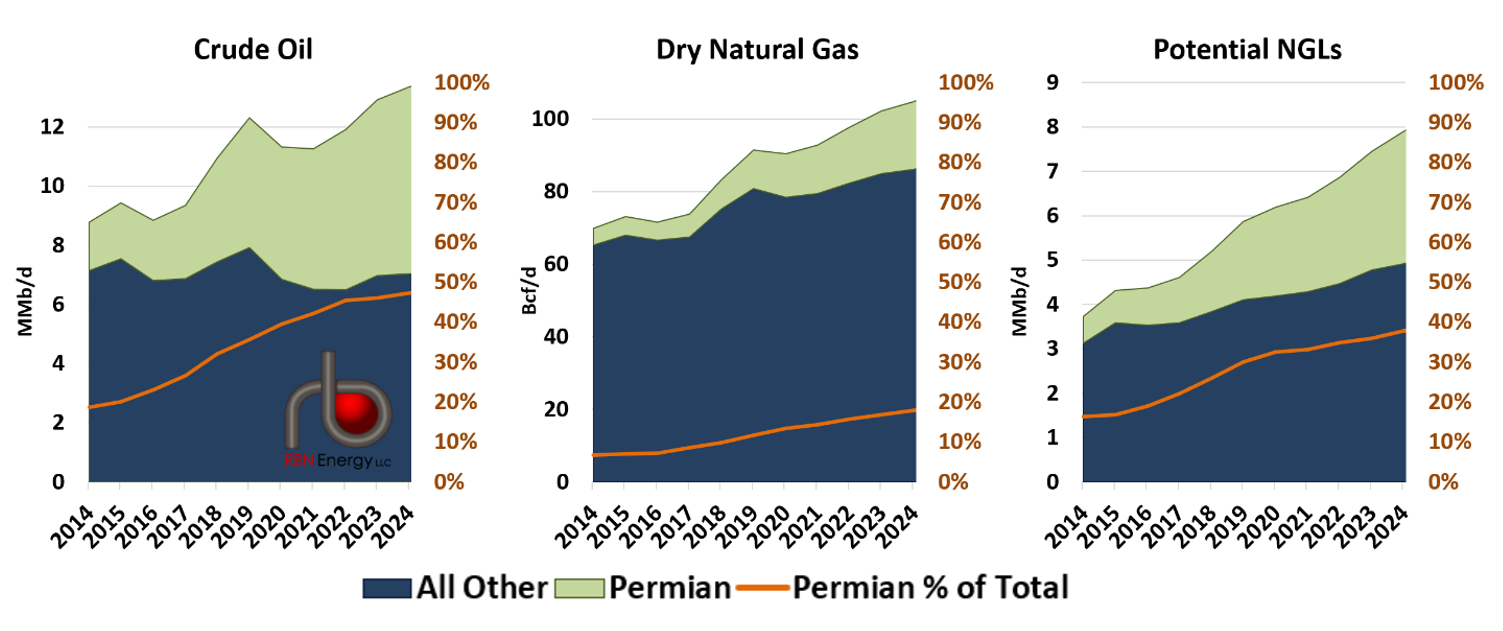

The rebirth and rise of the U.S. energy sector has been among the brightest spots in the domestic economic picture over the last 15 years, leading to a renaissance in industrial production, a huge reduction in the U.S. trade deficit, and energy independence from adversarial energy-producing countries. Over that time, the Permian has been a consistent driver of production growth of what RBN terms the “drillbit hydrocarbons”: crude oil, natural gas and NGLs. While the focus of Permian producers has always been on the crude stream, this crude oil comes with significant amounts of natural gas and NGLs. As shown in Figure 1 below, the shale play in West Texas and southeastern New Mexico has accounted for an ever-increasing proportion (orange lines and right axes) of overall domestic production of each commodity. Today, the Permian produces nearly half of all U.S. crude, about 20% of the country’s dry natural gas and almost 40% of its NGLs (ethane, propane, butane, isobutane and pentanes+) from processing.

Figure 1. The Permian’s Share of U.S. Production. Source: EIA

About the song

“All My Rowdy Friends Have Settled Down” was written by Hank Williams Jr. and appears as the first song on side two of Hank Williams Jr.’s 33rd studio album, The Pressure Is On. Released as a single in September 1981, it went to #1 on the Billboard Hot Country Songs Singles chart. “All My Rowdy Friends” would be referenced again in Williams’s 1984 tune, “All My Rowdy Friends Are Coming Over Tonight.” This song, reworked as “All My Rowdy Friends Are Here on Monday Night,” became the theme song for Monday Night Football. Personnel on the record were: Hank Williams Jr. (lead vocals), Kenny Bell (acoustic guitar), Reggie Young (electric guitar), Joe Osborn (bass), "Cowboy" Eddie Long (steel guitar), Vernon Derrick (mandolin), Lisa Silver (violin), Larry Knechtel (piano), Joe Osborn (bass), and James Stroud (drums).

The Pressure Is On was recorded in Nashville in 1981 and produced by Jimmy Bowen. Released in August 1981, it went to #5 on the Billboard Top Country Albums chart and #76 on the Billboard 200 Albums chart. Two singles were released from the LP, including the unofficial redneck national anthem, “A Country Boy Can Survive,” which went to #2 on the Billboard Hot Country Singles chart.

Hank Williams Jr. (also known as Bocephus) is an American singer, songwriter, and multi-instrumentalist. He is the son of country music legend Hank Williams and the father of Hank Williams III, a singer known for his mix of country, rockabilly and punk run. Hank Jr. made his first television appearance singing his father’s songs on The Ed Sullivan Show in 1963 at the age of 14. He has released 56 studio albums, 25 compilation albums and 109 singles, has won numerous ACM and CMA Awards and a BMI Icon Award, and is a member of the Country Music Hall of Fame. He continues to record and tour and will be touring the U.S. from May through September 2024.