Eager to boost oil and natural gas production, the government of Mexico is in the midst of a multi-year effort to introduce more private-sector involvement and competition. The hope is that a series of reforms will lead to more investment and—over time—a Mexican energy sector that more closely resembles that of Mexico’s amigos North of the Border. Today, we continue our look at the ongoing transformation of U.S.-Mexico hydrocarbon trade and what it may mean for energy companies on both sides of the Rio Grande.

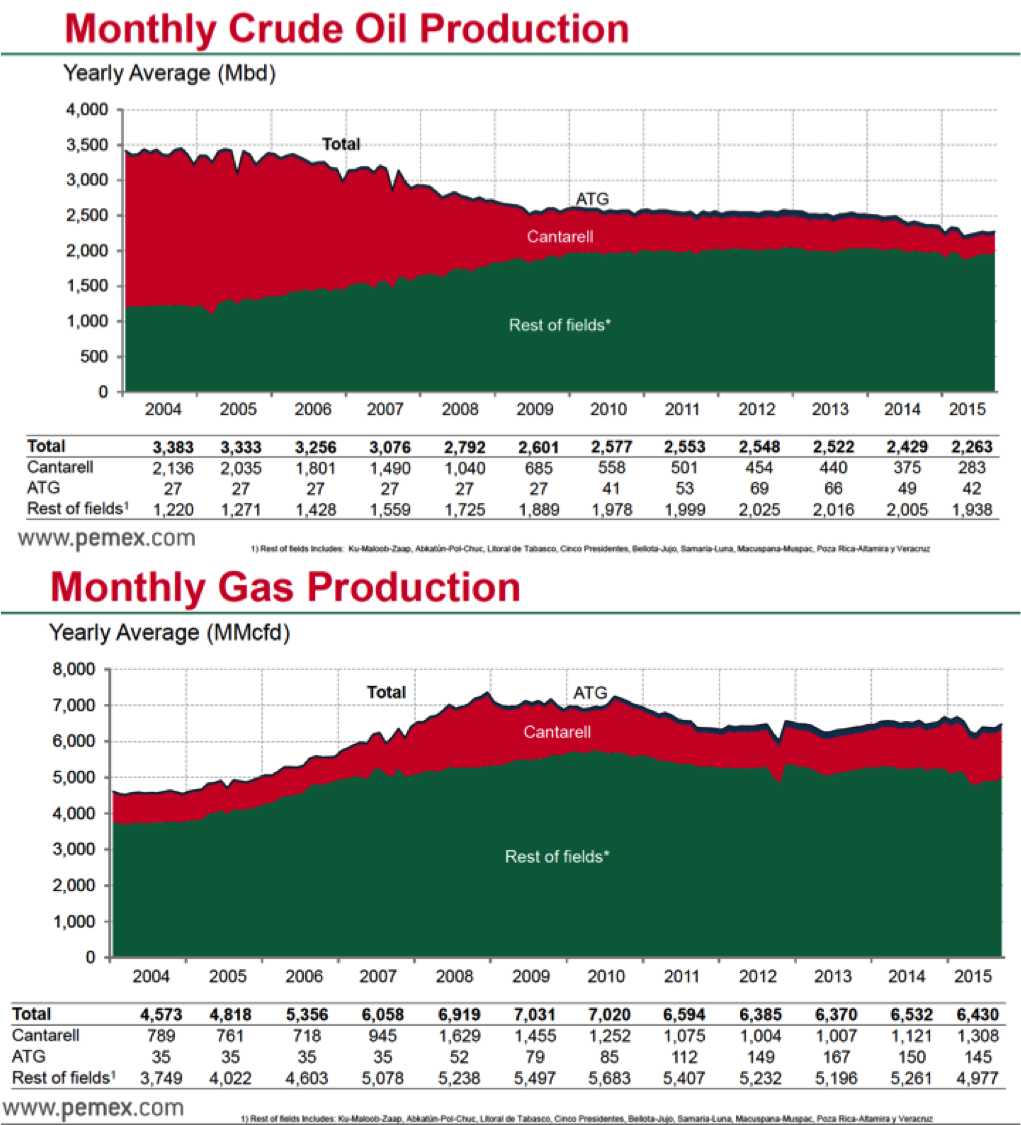

Since 2010, U.S. crude oil production has risen by 71%--from 5.5 MMb/d in 2010 to an average of 9.4 MMb/d in the first eight months of 2015, according to the U.S. Energy Information Administration (EIA). U.S. natural gas marketed production is also up: from about 61 Bcf/d in 2010 to 79 Bcf/d, on average, in the January-through-August period in 2015, again according to EIA. Over the same period, however, oil and gas production at Petróleos Mexicanos (Pemex)—Mexico’s state-owned energy company and (since 1938) the only producer in that country—has slipped and stagnated. Pemex’s oil production averaged 2.6 MMb/d in 2010 (from a peak of 3.4 MMb/d in 2004, when its Cantarell field in the Gulf of Mexico was going great guns; see upper chart in Figure 1) and has fallen every year since; in the first nine months of 2015 it averaged 2.3 MMb/d.

Figure 1; Source: Pemex, Investor Day Presentation, October 2015

Pemex gas production, meanwhile, has dropped from about 7.0 Bcf/d in 2010 to 6.4 Bcf/d in 2015’s January-through-September period (lower graph in Figure 1), even as demand for gas within the country has soared. (As you might expect, Mexican production of natural gas liquids is off too: from 377 Mb/d in 2010 to 330 Mb/d so far this year.) The U.S. and Mexico of course have different geologies and different magnitudes of oil and gas reserves, but there are similarities as well. For example, both countries have extraordinary shale oil and gas reserves; both also have been exploiting hydrocarbons beneath their parts of the Gulf (though Mexico’s focus has been on shallow-water finds). What many have suggested is that the real story behind Mexican production decline is the state-controlled nature of Pemex, and the financial and other pressures at Pemex that for years have 1) minimized investment in exploration/production of new oil and gas fields in the Gulf; 2) stymied development of northern Mexico’s potentially prolific Burgos shale region (just south of the Eagle Ford); and 3) slowed the pace of improvements to Pemex’s refineries, pipelines and other energy-related infrastructure. As we said in Episode 1, this combination of falling production and insufficient investment has only exacerbated the disconnect between the quality/volumes of (mostly heavy) oil Pemex is producing and its refinery configurations (which result in too much high-sulfur fuel oil and not enough high-value transportation fuels being produced).

About the song

“With a Little Help from My Friends” was written by John Lennon and Paul McCartney and appears as the second song on side one of The Beatles’ eighth studio album, Sgt. Pepper’s Lonely Hearts Club Band. Lennon and McCartney wrote the tune for Ringo Starr to sing on the album. They recorded the song in March 1967 at EMI Studios in London the day before the band posed in their costumes for the Sgt. Pepper album cover shoot. The song has been covered by many artists, with the most popular one being Joe Cocker, who sang it while making his presence felt at the Woodstock Musical Festival in 1969, and the documentary film that followed the event. Cocker released his version on a single in the UK in October 1968; it went to #1 on the UK Singles chart. Personnel on The Beatles’ version were: Ringo Starr (lead vocals, drums, tambourine), Paul McCartney (bass, piano, backing vocals), John Lennon (rhythm guitar, cowbell, backing vocals), George Harrison (lead guitar, backing vocals), and George Martin (Hammond organ).

Sgt. Pepper’s Lonely Hearts Club Band was recorded between November 1966 and April 1967 at EMI Studios and Regent Sound in London, with George Martin producing. It was released in May 1967 and went to #1 on the Billboard 200 Albums chart and all album charts worldwide. It has been certified 11x Platinum by the Recording Industry Association of America and has sold more than 32 million copies worldwide. The LP won four Grammy Awards and remains one of the top-selling albums of all time. Released during the Summer of Love in 1967, it became a defining moment in pop culture, and helped solidify the album format as a legitimate art form. No singles were released from the LP.

The Beatles were an English rock band formed in Liverpool in 1960. With members John Lennon, Paul McCartney, George Harrison and Ringo Starr, they changed the course of pop music and culture, becoming one of the most popular rock bands of all time. They released 17 studio albums, six live albums, 54 compilation albums, 36 EPs and 63 singles. The band has sold more than 600 million records worldwide. The Beatles have won numerous awards, including an Academy Award, seven Grammy Awards, four Brit Awards and Ivor Novello Awards, and are members of the Rock and Roll Hall of Fame individually and as a band. The Beatles officially broke up in 1970, with all members going on to successful solo careers. John Lennon was murdered in December 1980 and George Harrison died in November 2001. Paul McCartney and Ringo Starr still record and tour as solo artists.