When we described the quirky workings of the US renewable fuels mandates back in July and August of 2012 the topic was merely brain food for commodity market theorists and sleep deprived gasoline analysts. This month the market for big brother sounding “Renewable Identification Numbers” (RINS) - credited to refiners when they add ethanol to gasoline blends - is suddenly the hottest thing since sliced bread. The price of 2013 RINS shot from a few cnts/gal in January 2013 to an astronomical $1/gal on March 8, 2013. Earlier this week they were trading in the stratosphere, at about $0.70/gal. Today we look at what lies behind the current RIN furor.

The Ethanol Mandates

To understand what is going on with RINS you first need to know about the ethanol mandates. The Energy Policy Act of 2005 and the 2007 Energy Independence and Security Act (EISA) mandated increased use of renewable fuel in place of gasoline (see A Market of Contradictions: Ethanol Mandates Motor Gasoline and The Blend Wall). The Environmental Protection Agency (EPA) implements the mandates. By renewable fuel, the legislation principally refers to ethanol produced from corn but also covers biodiesel, cellulose biofuel (ethanol produced using crops other than corn), and advanced biofuel. Although the biofuel mandates are not without controversy the current market excitement is all about ethanol – by far the largest source of renewable fuel. Most US ethanol is produced from corn. The stated benefits of blending ethanol into gasoline are twofold. First ethanol is an oxygenate that reduces the carbon monoxide emissions that come from burning gasoline and second ethanol is renewable and in theory reduces our dependence on finite fossil fuels.

The EISA contains a mandate for a renewable fuel standard (RFS). Under the RFS refiners are required to sell specific volumetric target quantities of renewable fuels each year. These volumetric targets increase every year until 2015. Each year the EPA estimates gasoline and diesel consumption ahead of time and then sets percentage targets for renewable fuels for refiners to blend into gasoline. The target for corn ethanol blended into gasoline is 13.8 billion gallons (900 Mb/d) in 2013. Under the rules, the percentage of ethanol blended into gasoline is adjusted each year as required to meet the growing volumetric ethanol targets. The assumption behind this legislation was that US consumers’ appetite for gasoline would continue to grow and that the mandated volumes of ethanol would be comfortably absorbed into the gasoline pool using a 10 percent blend known as E10. That turned out to be a miscalculation and got us into the current mess because of something called the blend wall.

The Ethanol Blend Wall

Most US autos are not designed to operate using gasoline that contains more than 10 percent ethanol (E10). Some auto manufacturers have sold vehicles that can use 15 percent ethanol (E15) and even 85 percent ethanol (E85) but the complications of delivering gasoline using different ethanol specifications mean that the retail market is currently restricted to E10 for all practical purposes. That E10 restriction sets an upper limit on how much ethanol can be blended into gasoline. In effect, ethanol blended into gasoline cannot exceed 10 percent of gasoline demand. This implied upper limit is known as the ethanol blend wall.

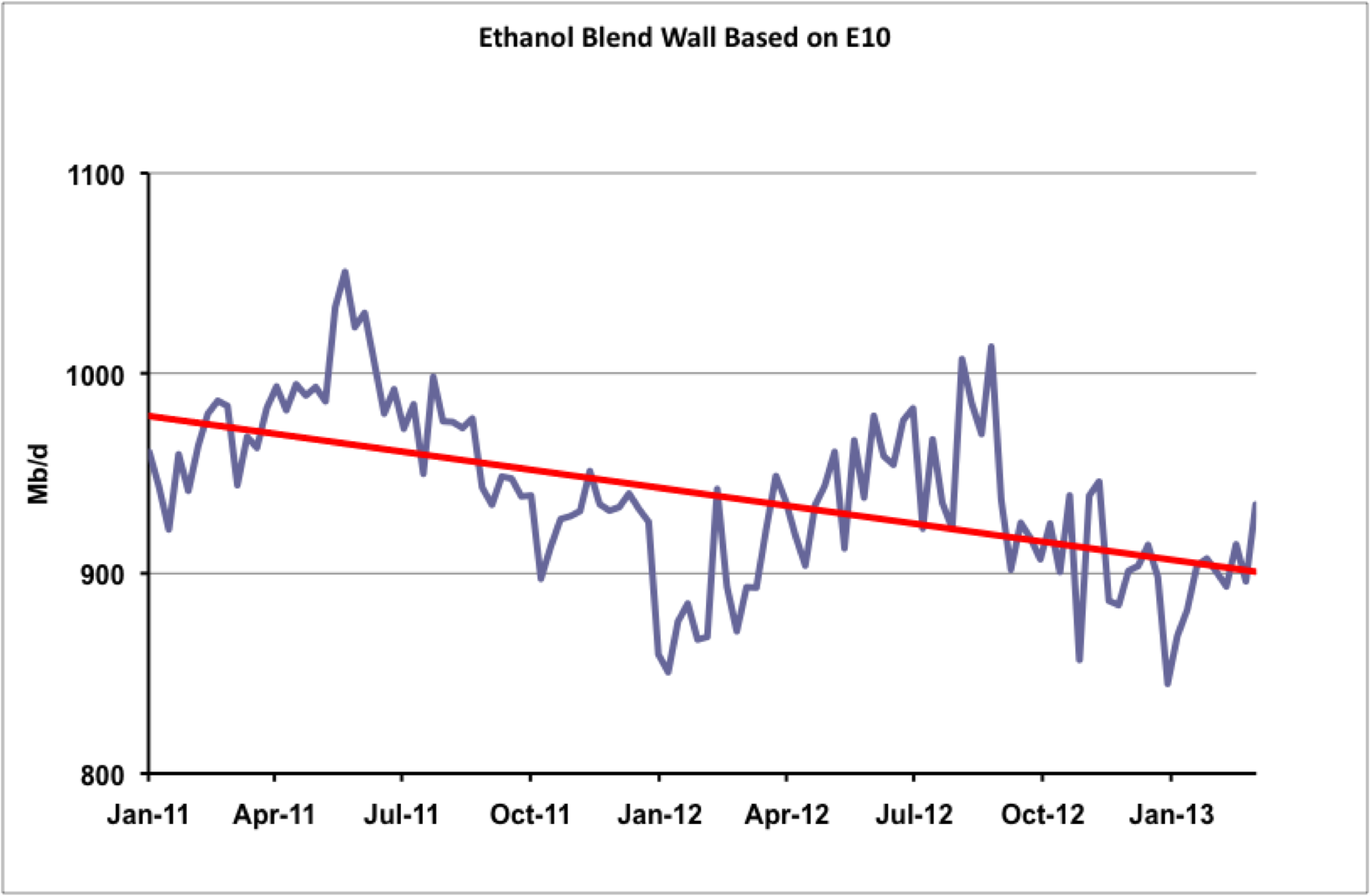

As we have discussed in previous RBN blogs, US gasoline demand is falling (see “Ethanol, Gasoline and Refineries – Another One Bites the Dust”) Increased federal mileage standards for auto manufacturers have resulted in more efficient vehicles. Higher gas prices have persuaded consumers to buy smaller more efficient cars. Since the recession, consumers have travelled less. As gasoline demand falls, the ethanol blend wall is reduced because the available pool of gasoline for ethanol blending decreases. You can get a pretty good idea of how the ethanol blend wall is falling from the chart below. The blue line is the implied ethanol blend wall based on 10 percent of the apparent demand for gasoline. [We explained how apparent demand is calculated in “No Apparent Demand – US Gasoline Thirst Evaporates”.] The red trend line on the chart shows the ethanol blend wall falling from just under 1 MMb/d at the start of 2011 to about 900 Mb/d today (March 2013). So far this year (March 2013) the ethanol blend wall value has averaged 895 Mb/d. Given that the RFS volume target for 2013 is 900 Mb/d that means refiners will not be able to blend enough ethanol into gasoline this year to meet the mandate target. The market can’t absorb as much ethanol as the refiners are required to add.

Source: EIA Data from Morningstar

Next year in 2014, the target goes up to 14.4 billion gallons or 940 Mb/d meaning that refiners will definitely struggle to blend adequate ethanol volumes into gasoline based on the E10 blend wall. This eventuality was never envisaged under the RFS legislation but until the law is changed, refiners are on the hook to meet the ethanol mandate targets regardless of the ethanol blend wall. Failure to comply with the ethanol mandate targets leaves refiners liable for hefty fines.

Getting out of Jail Free? The RIN Escape Plan

That is where RINS come in – because the RFS legislation left a loophole open that allows refiners to use RIN credits to avoid paying fines for missing their target ethanol volumes. Hence all the fuss about RINS and their sudden increase in value this month. We explained in detail how RINS work back in August 2012 (see The RIN and Stimpy Show – Crushing Pain and Mandate Madness).

Under the RFS legislation, refiners have to meet an annual target called a renewable volume obligation (RVO). This number is calculated ahead of time based on a percentage of expected gasoline sales that will be replaced by ethanol. Last year (2012) that percentage number was around 9 percent but in 2013 it is expected to increase. The EPA will set the 2013 volume targets later this month (March 2013).

The mandates require refiners adding ethanol to their gasoline to document these renewable fuel transactions within 5 days to the EPA moderated transaction system (EMTS). That system generates 38 digit RIN “credit” numbers that can then be applied towards a refiner’s renewable volume obligation (RVO). A refiner can use more ethanol in one year than their RVO (for example if ethanol prices are lower than gasoline, a refiner has an incentive to increase ethanol up to the 10 percent maximum no matter what their RVO). At the end of the mandate year, refiners can retain up to 20 percent of any additional RINS they acquire by exceeding their RVO as credits against the following year. Additional current year RINS can also be sold to other refiners who failed to meet their RVO because they didn’t blend enough ethanol. By using purchased RINS, these non-compliant refiners can avoid paying fines for not meeting their RVO. This mechanism creates a RIN trading scheme that is designed to incentivize increased compliance by establishing a secondary market for RIN credits.

Not Enough RINS?

RIN credits therefore provide a potential solution – at least this year and maybe next to beat the ethanol blend wall. Credits accumulated in 2012 because more ethanol was blended than the RFS mandate can be used in 2013 and through February 2014. The market has realized that once the blend wall is hit, those credits will start drying up. That has created the sudden heavy demand for 2013 RIN credits that saw their price increase so dramatically this month.

Refiners across the US are finding themselves hitting the blend wall and anxiously shopping for RINS to avoid paying fines for missing their RVO target. That anxiety is fuelling a roaring trade in RIN credits that now threatens to cost refiners as much as $1 for every gallon of ethanol they cannot blend into gasoline – through no fault of their own. At the same time the American Petroleum Industry (API) and the American Fuel & Petrochemical Manufacturers (AFPM - previously called the National Petroleum Refiners Association, or NPRA) are up in arms trying to get the EPA to either lower the blend wall by reducing the target ethanol volumes or by issuing waivers to refiners that cannot meet the targets. The ethanol lobby – led by the Renewable Fuels Association (RFA) take the other side of the argument just as passionately – saying that oil companies should have invested in infrastructure to facilitate E15 blends that would add another 5 percent to the blend wall. Since oil companies no longer own most retail gasoline outlets (they sold them to independents years ago) they have no reason to make that investment. In fact, refiners are better off simply not supplying the US gasoline market but rather increasing exports that the RFS mandates do not apply to.

For 2013 at least, the question remains -- are there enough RIN credits available in the market from 2012 to meet the ethanol targets this year? A lot of this analysis is hypothetical because we don’t know the exact number of credits or the shortfall of ethanol after we hit the blend wall. Recent scholarly research on the topic by the University of Illinois Department of Agriculture and Consumer Economics (published here) suggests the stock of RIN credits at the start of 2013 was 2.6 billion gallons (170 Mb/d), which will be depleted to 1.2 billion gallons (78 Mb/d) by the end of the year. The stock of RINS goes down because no new credits will be created for 2014 if ethanol targets are not met in 2013 and because refiners will have to use RIN credits once we hit the blend wall. The University of Illinois research further suggests that by the end of 2014 RIN credit stocks will go into negative territory by about 0.6 Billion gallons (40 Mb/d). At that point the RIN escape plan runs out of credits and refiners will be paying hefty fines for not meeting the ethanol mandates.

All this leaves refiners seeing red big time at the prospect of playing an expensive game of musical chairs to get enough RIN credits to meet their obligations this year and next or paying fines if they cannot comply with the mandates because of the blend wall. So far the EPA is showing no sign of giving way on the issue by lowering the targets or issuing waivers. Refiners are waging a vocal public relations campaign pointing out that the costs will end up being passed on to consumers. Meanwhile in the US energy market where natural gas price basis has collapsed and crude prices are flat or discounted, previously dormant RIN trading is attracting speculators like bees to a honey pot. The resultant chaos would once again make Ren and Stimpy proud.

Ren & Stimpy premiered on August 11, 1991, and ran for 53 episodes

Comments

Hi Sandy,

As this is my first comment on this blog, I would like to start by saying that I am an extremely avid reader of the daily energy posts and give tremendous credit to them for my increased knowledge of this very broad subject. Thank you for this.

In this blog and previous ones on this topic, you have indicated that at the end of the mandate year, refiners can retain 20% of excess RINs and apply them towards next year's obligations. It is my understanding that instead, refiners are permitted to apply excess RINs from the previous year towards 20% of the CURRENT year's mandate. There is a pretty significant difference between the two from the balances i have projected and hence wanted to point it out. Curious on your thoughts. Thank You.

Very useful article. Thank you.

Wouldn't this open the door to selling E85 at a huge discount? We know the government will not scale back the racket, especially when they have already built in a system of trading to deal with the illogical nature of the illogical mandate.