Next year (2014) RBN Energy expects Utica natural gas processing plants to produce 43 Mb/d of natural gasoline – more than 3 times 2013 production. Local demand will only soak up 17 Mb/d – leaving 26Mb/d needing transport to markets outside the region. Midstream companies are building infrastructure to accomplish this – by pipeline, rail, truck or barge. Today we conclude our survey of Utica Condensate and natural gasoline takeaway.

This is Part 5 in our blog series covering midstream plans to capture and deliver condensate range materials to market from Utica shale production. In Part 1 we described the expected surge in condensate, natural gas liquids (NGLs) and to a lesser extent crude oil production from the Utica shale in the next year (2014) as a result of new infrastructure coming online. Then we examined condensate and crude supply infrastructure plans recently outlined by MPC/MPLX (Marathon) at a recent conference. (November 15, 2013). In Part 2 we looked at MPLX’s longer term Utica transportation strategy to provide third party shippers with options to move liquids outside the region. In Part 3 we reviewed infrastructure proposals from Unity Pipeline Company and Kinder Morgan to move condensate and natural gasoline to Western Canada from the Utica as a diluent for blending with heavy bitumen crude to enable the latter to flow in pipelines. In Part 4 we covered existing and planned Crosstex and UEO infrastructure projects to takeaway condensates and natural gasoline from the Utica. This time we start with a look at the Northeast US natural gasoline supply/demand balance and then cover Blue Racer and MarkWest NGL takeaway projects.

But before we get to those topics let’s first touch on an update to Kinder Morgan Utica takeaway plans that we covered in Part 3. Recall that Kinder is building a gas processing plant at Tuscawaras, OH and has proposed building a 200 Mb/d pipeline from that plant to the Gulf Coast with JV partners Mark West and EMG. This week (December 16, 2013) Kinder announced a separate pipeline proposal to transport NGLs from fractionation facilities in Harrison County, OH (eg the UEO Scio plant we covered in Part 4 and the MarkWest EMG Hopedale plants that we cover in this blog). The Utica to Ontario Pipeline Access (UTOPIA) proposal – a joint venture with Nova Chemicals - would transport at least 50 Mb/d of NGL products to an intersection with Kinder’s Cochin pipeline at Riga, MI. From Riga, NGLs would be shipped East to Ontario. It is not clear whether this pipeline could ship natural gasoline West on Cochin to Western Canada – but that would seem to be an obvious option.

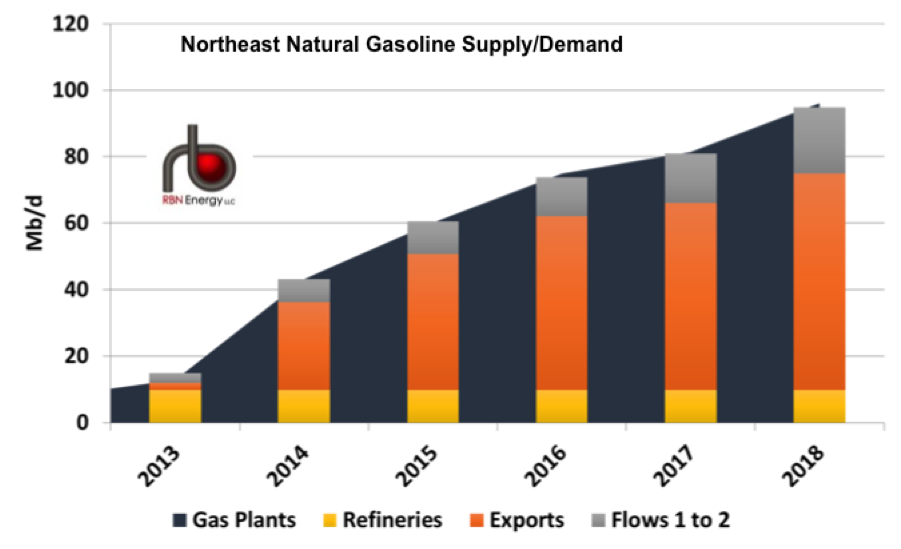

We start today’s analysis by providing perspective on the Northeast US natural gasoline supply/demand picture by sharing RBN Energy’s latest balance numbers. The chart below shows estimated current and future natural gasoline plant output from fractionation in the Northeast region. We classify the Northeast as the Department of Energy Petroleum Administration for Defense District (PADD) 1 plus the Ohio Utica – meaning production from the Marcellus and Utica basins. As you can see, the plant supply (blue shading) increases rapidly in 2014 – up by nearly 300 percent from 13 Mb/d in 2013 to 43 Mb/d. Supply then continues to increase – more than doubling again by 2018 to 96 Mb/d.

Source: RBN Energy

Demand for these growing supplies will come from local refineries (yellow bars on the chart – a static 10 Mb/d) and movements from the Northeast to the Midwest (PADD 1 to PADD 2 gray bars on the chart - 7 Mb/d in 2014 increasing to 20 Mb/d in 2018). The balance of supplies will have to be exported outside the region to find a market (orange bars on the chart). These exports will amount to 26 Mb/d in 2014 expanding by 250 percent to 65 Mb/d in 2018. Exports will either go to Canada as diluent as we described in Part 3 or they will be moved to other regions of the US most likely as a component of “Y”-grade (mixed NGLs) Our focus in this series is on takeaway capacity out of the Northeast for these supplies.