If the world is going to reduce greenhouse gas (GHG) emissions to net-zero levels by 2050, a lot of things need to go right, with the success of the International Energy Agency’s (IEA) long-term plan balancing on three different pillars. First, there are emissions reductions from improvements to fossil fuels and processes, such as power generation and industrial production. Next, there are advancements in bioenergy, a category that includes biofuels like ethanol, sustainable aviation fuel (SAF), and renewable diesel (RD). And then there’s direct air capture (DAC) — a minor factor so far, but one with the potential for significant growth, especially given the billions in U.S. funding already set aside for it. In today’s RBN blog, we look at U.S. plans to develop four regional DAC hubs, how those proposals will be evaluated, and the likely timeline for their development.

Creation of a strategy to achieve net-zero GHG emissions has been an important goal of the Biden administration, with long-term decarbonization efforts at the heart of its two most significant legislative achievements to date. The first of those bills to pass, 2021’s Infrastructure Investment and Jobs Act (IIJA), better known as the Bipartisan Infrastructure Law, set aside $3.5 billion for the creation of the DAC hubs we will explore in greater detail today. It also included $65 billion in funding for clean energy transmission and the power grid, and $7.5 billion to build a nationwide network of electric vehicle (EV) chargers (see our One Shining Moment series for more on EVs), along with a host of other clean-energy priorities. Further, the IIJA provided the Department of Energy (DOE) with $8 billion to support the development of several regional hydrogen hubs — an initiative similar to the DAC hubs which are the focus of today’s blog — that we’ve detailed in a series of blogs and a Drill Down Report. (For the latest on how that process is playing out, see The Contenders.)

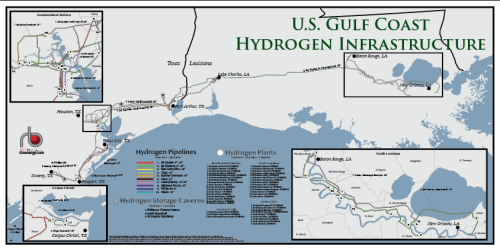

RBN’s U.S. Gulf Coast Hydrogen Infrastructure Map lays out the pipelines and merchant hydrogen plants that make up the gulf coast market, providing an unprecedented snapshot of the region’s hydrogen infrastructure network.

The more recent of those two game-changing bills is 2022’s Inflation Reduction Act (IRA), which includes major revisions to the federal 45Q tax credit for carbon capture and sequestration (CCS), a topic we’ve written about extensively in our Way Down in the Hole series. Under the IRA, the credits jumped to $85/metric ton (MT) for CCS and $60/MT for carbon capture use and sequestration (CCUS) for enhanced oil recovery (EOR). Under the previous law, those credits were scheduled to top out at $50/MT and $35/MT, respectively, in 2026. To claim the higher credits, prevailing-wage (typically union scale) and apprenticeship requirements need to be met during construction and for each year of the 12-year credit period. (The “base credits” if those criteria are not met are 80% lower, at $17/MT for CCS and $12/MT for CCUS, which essentially makes all carbon-capture projects uneconomic.) DAC gets the biggest boost from the IRA, with credits rising to $180/MT for CCS and $130/MT for CCUS, although the base credits would also be much lower, at $36/MT for CCS and $26/MT for CCUS.

About the song

“Stuck in the Middle With You” was written by Gerry Rafferty and Joe Egan and appears as the second song on Stealers Wheel’s debut album, Stealers Wheel. Released as the third single from the album in April 1973, the song went to #6 on the Billboard Hot 100 Singles chart and has sold over 1 million copies. The song became famous again when used in a notorious scene in Quentin Tarantino’s 1992 debut film, Reservoir Dogs. Personnel on the record were: Gerry Rafferty (lead vocal, guitar), Joe Egan (backing vocals, keyboards), Paul Palnick (lead guitar), Iain Campbell and Tony Williams (bass), Rod Coombes (drums) and Luther Grosvenor (lap steel guitar).

The album Stealers Wheel was recorded at Abbey Road Studios in London and was produced by Jerry Leiber and Mike Stoller. Released in October 1972, it went to #50 on the Billboard Top 200 Albums chart. It has been certified gold by the Recording Industry Association of America.

Stealers Wheel was a British folk-rock band originally formed in Paisley, Scotland, by former schoolmates Gerry Rafferty and Joe Egan in 1972. Eleven members passed through its ranks until the band broke up in 1975. It re-formed in 2008, but only briefly. They released three studio albums, three compilation albums and five singles. Gerry Rafferty went on to a successful career as a solo artist, releasing 10 studio albums and the hit single “Baker Street.” Joe Egan made two solo studio albums and currently runs a music publishing company in Scotland.