The illusion of a smooth energy transition was swept away in 2021, with the drive toward decarbonization running headlong into the reality of energy markets. It is now clear that the transition and its effects are permeating all aspects of supply and demand, from the chaos in European natural gas, to producer capital restraint in the oil patch, to the rising impact of renewable fuels and, of course, the escalating roadblocks to pipeline construction. Gone are the days when traditional energy markets operated independently of the energy transition. Today the markets for crude oil, natural gas, and NGLs are inextricably tied to renewables, decarbonization, and sustainability. It’s simply impossible to understand energy market behavior without having a solid grasp of how these factors are tied together. That is what School of Energy Spring 2022 is all about! In today’s RBN blog — a blatant advertorial — we’ll highlight how our upcoming conference integrates existing market dynamics with prospects for the energy transition.

First, a brief synopsis of School of Energy Spring 2022. It is scheduled for May 17-18, in-person (finally!!) at The Houstonian in Houston. We’ve reorganized the curriculum one more time, this time assessing the most important developments that energy markets must deal with in the real world of today, in the context of a lower-carbon future that is bringing radical changes in how energy commodities are produced, transported and used. As always, we’ll start with the basics of what makes energy markets tick, work through hands-on models of energy fundamentals, and review RBN’s forecasts for what lies ahead. Then we’ll get into what we believe are the most important hydrocarbon-related issues in the energy transition. That includes carbon dioxide (CO2) sequestration, hydrogen, and renewable fuels. For more about School of Energy Spring 2022, click here to read more about the themes we’ll be covering.

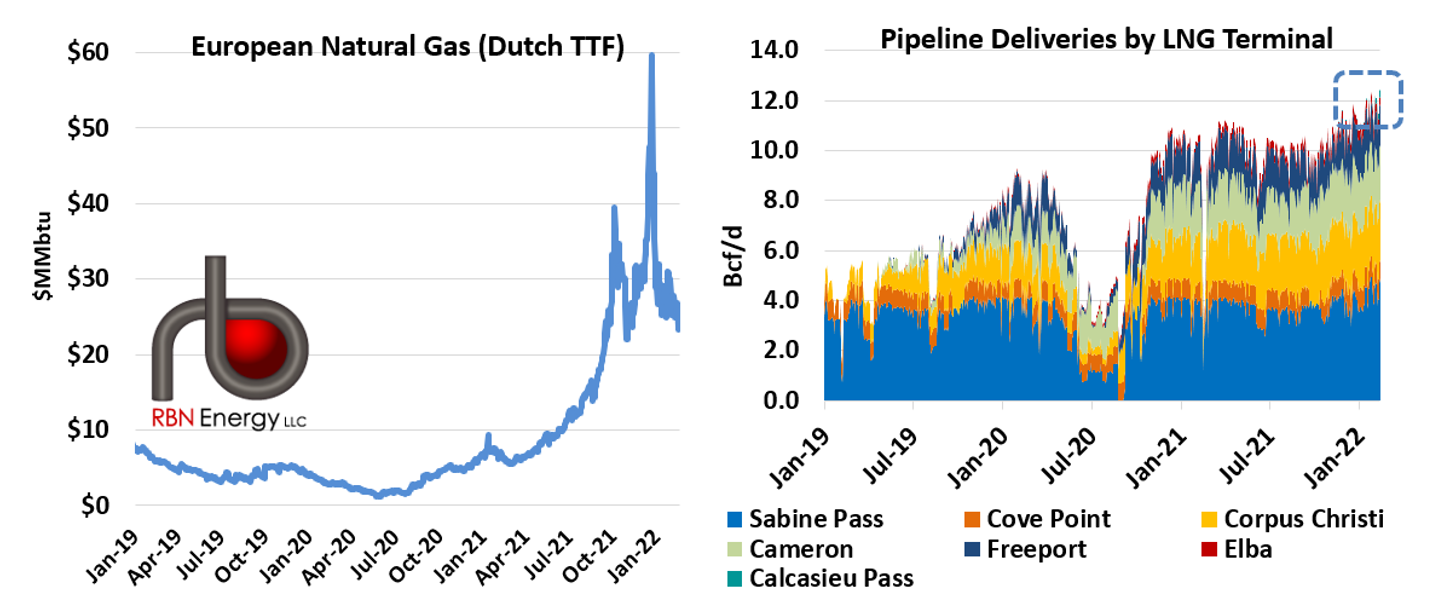

We’ll begin this spring’s School of Energy with a look at a few of the most evident symptoms of the energy transition trauma, first considering the highest-profile disruption — the European natural gas market in the winter of 2021-22. As shown in the left graph in Figure 1, the chaos in that market has been off the scale for the past year, with prices blasting up to $60/MMbtu in December 2021 before falling back to a “meager” $25-30/MMbtu lately — still over 6X the price of Henry Hub gas. Of course, there are many reasons for the surge, including shortfalls in Russian imports and low inventories entering this winter’s heating season. But some of the key drivers have been related to the energy transition, such as declining domestic natural gas production due to lack of investment in existing fields [in part due to European Union (EU) environmental regulations] and carbon pricing rules that incented reliance on wind and solar generation. Unfortunately, these drivers converged, with Europe’s less-windy-than-usual summer of 2021 resulting in a greater reliance on natural gas (see It’s Too Late for more on the European Gas crisis).

Figure 1. European Natural Gas Price; U.S. LNG Feedgas. Sources: Bloomberg, Wood Mackenzie Genscape

Only by paying astronomical prices for imported LNG has the European market been able to avoid a catastrophic winter market meltdown. But the high prices will have dire consequences for European gas users and governments, and it has yet to be seen how these market events will ultimately impact energy transition policy. Suffice to say that the collision between decarbonization and energy markets is now front-and-center for all to see.

Note also that U.S. domestic gas markets have not been completely isolated from the European mayhem. U.S. LNG exports based on the cost of domestic gas are absurdly profitable when delivered into the European market and are limited only by U.S. LNG liquefaction and export capacity. However, as shown in the right graph in Figure 1, LNG export facilities are running at full throttle, with pipeline feedgas deliveries into LNG terminals averaging a record 11.8 Bcf/d over the past three weeks and some terminals running above design capacity just to produce a few extra lucrative cargoes (dashed blue box in Figure 1). Still more LNG export capacity will be coming online over the next few months. That increase in feedgas demand has already had an impact on U.S. natural gas prices and will continue to tighten balances for years to come.

U.S. Crude Oil Production

The impact of the energy transition on crude oil markets is just as consequential, though so far primarily on the supply side of the equation. Wall Street pressure on publicly traded E&P companies to constrain their expenditures in what is perceived as a sunsetting energy industry and instead return capital to shareholders through dividends and buybacks has dramatically altered the calculus of price and production growth.

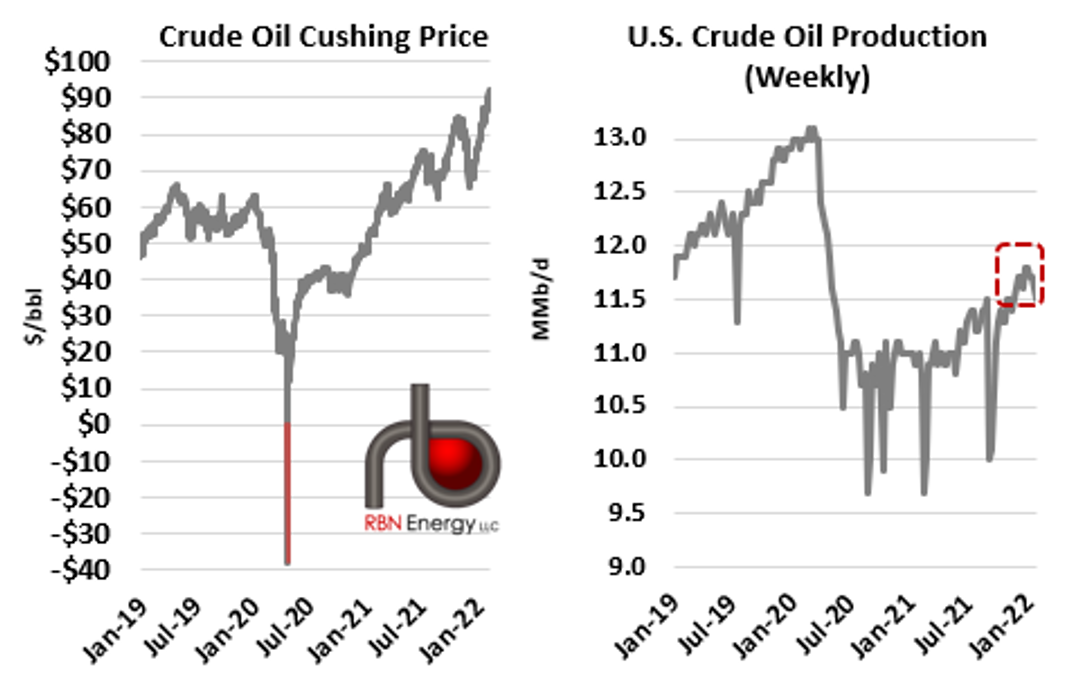

The current price of WTI is around the level it was at from 2012 to 2014, a period during which U.S. production grew by 50% — from 6 MMb/d to 9 MMb/d. After the crude price collapse of 2014-15, the industry’s growth resumed through 2019, and U.S. production grew again by another 2.5 MMb/d while the WTI price averaged only $54/bbl. Producers were able to survive and continue drilling even with prices essentially half of what they had been.

But the world has changed again. Now, after the COVID-related demand collapse of 2020, a whole range of factors — from OPEC+ discipline to the partial recovery in petroleum product demand — has driven the price of WTI back into the $80s-90s/bbl, as shown on the left graph in Figure 2, but as the right graph indicates, U.S. production growth continues to languish well below the pre-pandemic level. In fact, in EIA’s most recent numbers, production for the week ended January 28 was 11.5 MMb/d, exactly the same level as in August 2021, when the price of crude was “only” $68.50/bbl (dashed red box).

Figure 2. U.S Crude Oil Prices and Production. Sources: CME/NYMEX, EIA

The moral to this part of the story is that the looming energy transition has been a major contributor to a slowdown in U.S. crude oil production growth at a given price level. To the extent that this new relationship between price and production growth is sustained, there will be significant implications for price volatility and the absolute level of crude prices. The old oil-patch adage that “high prices are the cure for high prices” seems to have been repealed. What will that mean for market price differentials, infrastructure development opportunities, and crude oil exports?

School of Energy Content

European gas and U.S. crude markets are only two examples of a myriad of topics that we will explore at School of Energy. The title of today’s blog is our theme: What happens when the sledgehammer of the energy transition slams into traditional energy reality? How does the energy industry move toward decarbonization while at the same time making sure markets have enough energy to survive the transition?

If you are not familiar with RBN’s School of Energy, the conference is structured more like a classroom experience, where we work through current developments in some aspect of the market and then examine those developments in the context of Excel models that grapple with a wide range of issues, including production economics, production forecasting, frac and crack spreads, gas processing economics, ethane rejection, and all sorts of similar topics. These models are similar to what we’ve used in past Schools, except that they have all been updated. Likewise, the course content follows the same themes we write about each day in our blogs — namely, that the markets for crude oil, natural gas, NGLs, and renewables are tied together in ways that are shifting dramatically. And, of course, with our focus on the effects of energy transition efforts, we’ll spend plenty of time talking about the challenges and opportunities that arise as a result. School of Energy is designed to integrate your knowledge of these market factors with hands-on, practical instruction and training.

We’ll have the whole RBN crew at this year’s School of Energy, with 14 instructors taking part in the course work. Our faculty includes industry veterans and top-notch analysts who will dive deep into the analytics and models across crude, gas, and NGL markets.

Here’s how the School of Energy will work. You’ll download spreadsheet models and conference presentations the day of the conference. We will start promptly at 8 a.m. at The Houstonian in Houston, and there will be a one-hour lunch break and conference mixer at the end of Day 1. The curriculum will be organized by market sector, but we’ll weave together the impact that each sector has on the others. You can save 20% if you register for the Early Bird Rate.

For more information about the conference, click here. For group rates, contact [email protected].

About the song

“Sledgehammer” was written by Peter Gabriel and appears as the second song on side one of Peter Gabriel’s fifth studio album, So. Released as the first single from the album in April 1986, “Sledgehammer” went to #1 on the Billboard Hot 100 Singles chart. Buoyed by the constant rotation of the video for the song on MTV, it remained at #1 for four weeks and won a record-breaking nine MTV Video Music Awards. The unique video for “Sledgehammer,” directed by Stephen R. Johnson, utilized claymation, pixilation, and stop-motion animation. Personnel on the record were: Peter Gabriel (vocals, Fairlight CMI, Prophet, piano), Tony Levin (bass), Manu Katche (drums), David Rhodes, Daniel Lanois (guitars), Wayne Jackson (trumpet), Mark Rivera (sax), Don Mikkelsen (trombone), and P.P. Arnold, Coral Gordon, Dee Lewis (backing vocals).

So was recorded between February-December 1985 at Ashcombe House in Somerset, England, with Peter Gabriel and Daniel Lanois producing. Released in May 1986, the album went to #2 on the Billboard 200 Albums chart and has been certified 5x Platinum by the Recording Industry Association of America. Five singles were released from the LP, helping to transform Gabriel from a cult world music figure to a mainstream pop artist. It remains his best-selling album.

Peter Gabriel is an English singer, songwriter, musician, producer, and activist. He started his professional music career as the lead vocalist for the prog-rock band Genesis. He was with them from their formation in 1967 until his departure from the group in 1975. He has released six albums with Genesis, nine solo studio albums, four soundtrack albums, six live albums, six compilation albums, and 43 singles. He has won six Grammy Awards, three Brit Awards, two Ivor Novello Awards, and 13 MTV Video Music Awards. He continues to record and tour, and is currently at work on a new LP, tentatively titled I/O, which would be his first new album release since 2011.

Comments

It is concerning to see a lack of balance in discussion about climate alarmism. There is no science to prove that higher levels of CO2 in the atmosphere and higher average temperatures are harmful and that the world is in danger. The climate models that are claimed to be "science" are flawed and can't even back-cast weather. The earth's atomospehre is so complex that even the most powerful supercomputers are incapable of modeling our earth's climate. The earth is the Lord's and the fullness thereof. We couldn't burn up the world if we tried.

The push for "decarbonzation", a deceitful term (CO2 is not carbon), is being driven by governments, seeking more power and control, woke elite investor classes, and greedy corporations. Wind and solar energy are not dispatchable, are not "green", and they are not sustainable. They require millions of tons of plastics, cement, and rare earth minerals that are mined in many countries using child labor, slave labor, and poor environmental conditions. The vast majority of solar panels and wind turbines are manufactured in China using cheap coal fired energy. China builds a new coal fired power plant every week. China, India, Russia, and developing economies will not elimate emissions of CO2. China is using climate alarmism to weaken the West in their push to be the dominant world superpower for the 100th anniversary of the communist revolution. Decarbonization is hurting the middle class and the poor globally. This is class warefare. When will we wake up? Probabaly not until it is too late. The solution is Biblical stewardship of the resources we have been given and economic development which allows poorer countries to clean up their environments. Cornwall Aliiance is an excellent source of information on stewardship and the harm being done by climate alarmism.