There’s been a surge in E&P interest in the Utica Shale’s volatile oil window the past couple of years, and EOG Resources has been particularly optimistic about its potential for producing large volumes of condensate, the lightest of superlight crude oils. A few days ago, EOG — known for growing its business organically, not via M&A — announced one of the largest acquisitions of the year so far: the planned purchase of Encino Acquisition Partners (EAP), the Utica’s #1 condensate producer by far, for $5.6 billion, including the assumption of EAP’s debt. As we discuss in today’s RBN blog, the deal will give EOG its third “foundational” focus area (the others are the Eagle Ford and the Permian's Delaware Basin) and supports the view that the Utica really is an up-and-comer.

Build your energy market expertise at the 20th School of Energy: Foundations.

Learn from RBN experts, participate in hands-on Excel modeling, connect with industry peers, and gain a stronger understanding of today's interconnected energy markets.

September 9-10 | Houston, TX

In our three-part Hit the Lights blog series a few months ago, we took an in-depth look at condensate production growth across a swath of eastern Ohio, as well as the leading E&Ps in the play and the pipelines and other infrastructure on which they depend. In Part 1, we said that while the broader “wet Marcellus/Utica” is famous for producing vast quantities of natural gas and NGLs, a handful of dogged, innovative E&Ps have concentrated primarily on producing fast-rising amounts of superlight crude — better described as condensate (condy or conde for short) — in the Utica Shale’s volatile oil window, focusing primarily on Ohio’s Carroll, Columbiana, Guernsey, Harrison and Noble counties. Most of the condensate has an API gravity of 55 to 59 degrees, but an increasing share is “heavy condensate” with an API closer to 50.

We noted that after ups and downs through the 2010s, Ohio’s crude oil production — almost all of it condy — is up nearly 3X from July 2022, when it averaged only 48 Mb/d; the state produced 136 Mb/d in March, according to the most recent data available from the Energy Information Administration (EIA). Admittedly that’s only a small fraction of what the Permian is churning out (about 6.5 MMb/d lately, according to RBN’s weekly Crude Oil Permian report) and barely one-tenth of Bakken production. But EOG has said the eastern Ohio wells it’s drilled over the past couple of years have IP30 (initial production over 30 days) rates that compare favorably with the best wells in the Permian: 1,425 b/d to 3,250 boe/d, with crude oil/condensate’s share of the Utica wells’ production ranging as high as 70% on a boe/d (barrels of oil equivalent per day) basis.

In Part 2, we discussed the six largest condensate producers in eastern Ohio, starting with #1 EAP and followed by #2 Ascent Resources, #3 EOG, #4 Infinity Natural Resources (which launched a well-received initial public offering, or IPO, in January), #5 Expand Energy (the recently merged Chesapeake Energy and Southwestern Energy) and #6 GulfPort Resources. Part 3 focused on the uses for condensate produced in eastern Ohio and other parts of the Marcellus/Utica and how the condy is transported from wellsites to refineries and other end users.

Long story short (see Part 3 for details), Utica condensate is in demand — it can either be run as a feedstock at refineries, condensate splitters or petchem plants, blended into heavier crude or (in a pinch) used as diluent. As for infrastructure, a couple of things are worth pointing out. First, a good bit of the condensate emerging from eastern Ohio wells needs to have its light ends (propane/butanes) removed; some producers do this themselves at the well pad with heater treaters and some turn to centralized condensate stabilizer sites in Ohio (like MPLX’s at Cadiz, Williams Companies’ at Scio and Ergon Inc.’s at Marietta). Second, there are no condy gathering pipelines in the Utica — the volumes are too small (at least so far) to justify investments in them. Instead, condensate is stored at or near the wellhead in tank batteries, then loaded onto tanker trucks and driven either to the end user (typically a refinery or condensate splitter) or, more frequently, to the next mode of transport (a rail terminal, a marine terminal or a pipeline intake point). Part 3 discusses these takeaway options in depth.

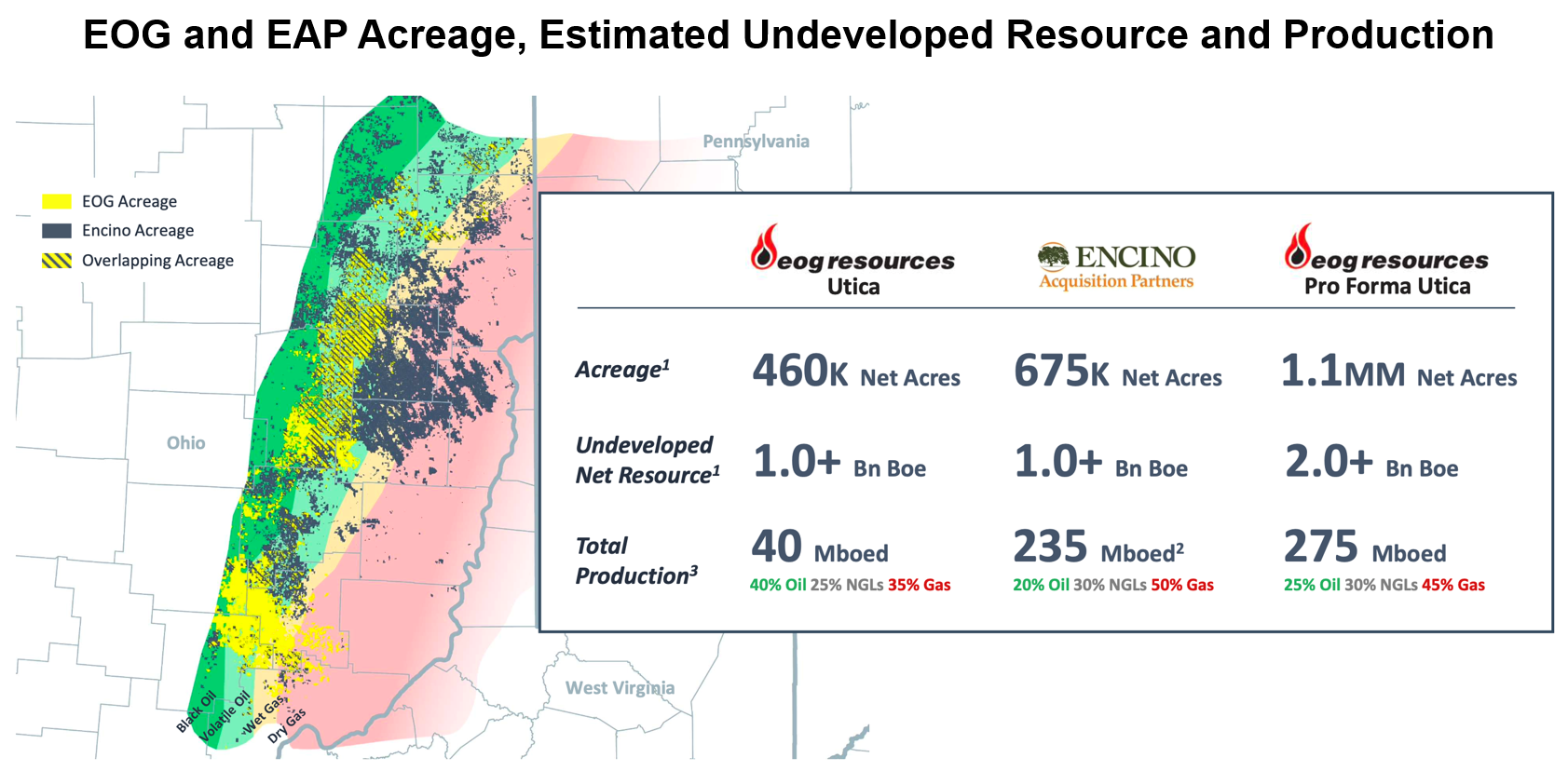

Figure 1. EOG and EAP Acreage, Estimated Undeveloped Resource and Production. Source: EOG

About the song

“Jump” was written by Michael Anthony, David Lee Roth, Eddie Van Halen and Alex Van Halen. It appears as the second song on side one of Van Halen’s sixth studio album, 1984. It was a unique direction for Van Halen in that the song was driven by a keyboard riff rather than a guitar. With its refrain of “Might as well jump!”, the song addresses survival, life and love in just over four minutes. Roth dedicated the song to his full-contact karate instructor, Benny “The Jet” Urquidez. Roth’s karate skills are on full display in the music video for “Jump.” Released as a single in December 1983, it went to #1 on the Billboard Hot 100 Singles chart and has been certified Gold by the Recording Industry Association of America (RIAA). It has been used in countless television shows, motion pictures and at sporting events. It remains the most successful single of Van Halen’s career. Personnel on the record were: David Lee Roth (lead vocals), Eddie Van Halen (lead guitar, synthesizer, backing vocals), Michael Anthony (bass, backing vocals) and Alex Van Halen (drums).

1984 was recorded between June and October 1983 at 5150 Studios in Studio City, CA. Produced by Ted Templeman, it was released in January 1984 and went to #2 on the Billboard 200 Albums chart. It has been certified Diamond (10 million sales) by the RIAA. Four charting singles were released from the LP.

Van Halen was an American rock band formed in Pasadena, CA, in 1973 by Eddie Van Halen, Alex Van Halen, David Lee Roth and Michael Anthony. They released 12 studio albums, two live albums, four compilation albums and 56 singles, and have sold more than 80 million records worldwide. They band won an American Music Award, a Grammy Award, four MTV Video Music Awards, and was inducted into the Rock and Roll Hall of Fame in 2007. Eight members passed through Val Halen during its decades-long run. David Lee Roth initially left the band after its 1984 Tour and was replaced by ex-Montrose singer Sammy Hagar. It could be argued that Montrose’s debut album, overseen by Van Halen producer Ted Templeman, was the blueprint for Van Halen’s debut LP. After Hager left the band in 1996, Extreme vocalist Gary Cherone took over vocal duties for one album and a tour before the band took a hiatus from 1999 to 2003. Hager briefly returned to the band for a tour in 2004. Longtime bassist and founding member Michael Anthony was dismissed from the band and replaced by Eddie Van Halen’s son, Wolfgang, in 2006, and David Lee Roth rejoined the band. Eddie Van Halen’s death in October 2020 in Los Angeles at 65 signaled an end to the band he helped start.