Brutal arctic cold may have chilled broad swaths of the U.S. last month, but the scorching pace of upstream M&A activity continued to be red hot, with nearly $20 billion in deals announced in January after a record-setting 2023. Last year’s transaction value totaled an astounding $192 billion, a mark 79% higher than the previous 10-year high and more than the previous three years combined. Why the surge? A wide range of factors influenced corporate decisions to grow through acquisitions rather than organic investment, including commodity prices, equity values, debt levels, operating costs, and production trends. In today’s RBN blog, we’ll analyze M&A trends through several statistical lenses and provide some insights into 2024 activity.

Build your energy market expertise at the 20th School of Energy: Foundations.

Learn from RBN experts, participate in hands-on Excel modeling, connect with industry peers, and gain a stronger understanding of today's interconnected energy markets.

September 9-10 | Houston, TX

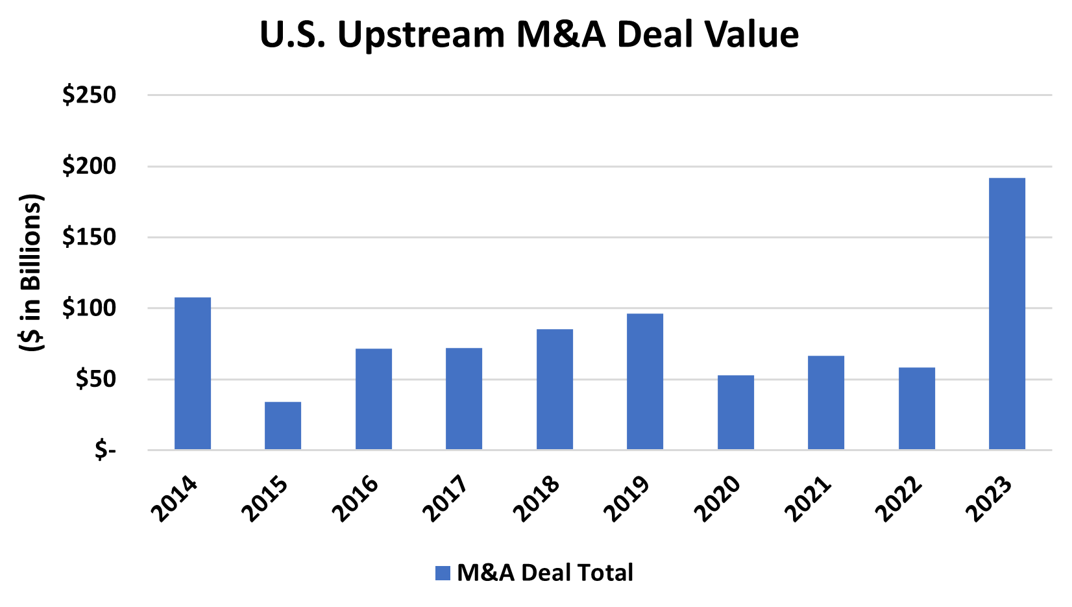

Figure 1 below, which illustrates the total value of upstream M&A transactions over the past 10 years, shows what a standout year 2023 was. And last year closed on a high note: The $144 billion in transaction value in Q4 alone surpassed the previous annual high of $107 billion in 2014. Q4 M&A activity was dominated by three major industry mergers, including ExxonMobil’s $59.5 billion purchase of Pioneer Natural Resources, Chevron’s $53 billion takeover of Hess Corp., and Occidental Petroleum’s $12 billion acquisition of privately owned CrownRock. One other data point: Upstream M&A last year was overwhelmingly tilted toward crude oil, with $186 billion in deals targeting oil-focused companies compared with just $6 billion in gas-focused transactions. And — no surprise here — the Permian Basin dominated the regional distribution of the deals, with $103 billion in 2023 acquisitions, with a record average deal size of almost $4 billion.

Figure 1. U.S. Upstream M&A Annual Deal Value. Source: Enverus

About the song

“Keep on Dancing” was written by Allen A. Jones, Andrew Love, and Richard Shann. It appears as the first song on side one of The Gentrys’ debut album, Keep on Dancing. Songwriter Andrew Love became half of the popular session horn duo, Memphis Horns, and Allen A. Jones became a well-known producer at American Recording Studio in Memphis, producing records by Albert King, The Bar-Kays, and others. “Keep on Dancing” was originally released as a single by the R&B band, The Avanti's, in 1963. The Bay City Rollers released a version as their debut single in 1971 — it went to #7 in the U.K. pop single charts. The Gentrys released their single in June 1965 and it went to #4 on the Billboard Hot 100 Singles chart. The Gentrys’ single is unique in that it is one short song with a fade and reintroduction starting the song again to stretch its length to an AM-radio-friendly time of 2:18. Personnel on the record were: Larry Raspberry (lead vocal, guitar), Jimmy Hart, Bruce Bowles (backing vocals), Bobby Fisher (keyboards), Pat Neal (bass), and Larry Wall (drums).

The album, Keep on Dancing, was recorded in Memphis in early 1965 at American Recording Studio, with Chip Moman producing. Composed of cover tunes, including the hit song, “Keep on Dancing,” the album was released on MGM Records in July 1965.

The Gentrys were an American rock band formed in Memphis at Treadwell High School where all the members were attending school together. Best known for their 1965 hit single, "Keep on Dancing," the group appeared on Shindig!, Hullabaloo, and Where the Action Is. They toured as the opening act for The Beach Boys, Sonny and Cher, as well as various Dick Clark package tours. The band broke up in 1967, reformed in 1969, and broke up again in 1973. They released three studio albums and three singles. Original band member Larry Raspberry went on to release an album with Alamo in 1971, and two LPs with Larry Raspberry and the Highsteppers in the mid-1970s. The band is still active. Founding member Jimmy Hart later found fame in professional wrestling as a manager named “The Mouth of the South.”